Toward a New Demand Normal

Global petroleum product consumption has bounced back from last year’s beleaguered, sloth-like pace but we’re absolutely not yet out of the woods.

If you’re already subscribed and/or appreciate the free summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Oil demand growth now sets the general pace of the oil industry and that pace has been slowing; forecasts now expect global demand to advance through 2025 and 2026 at an uninspiring rate compared to the steady growth pre-COVID.

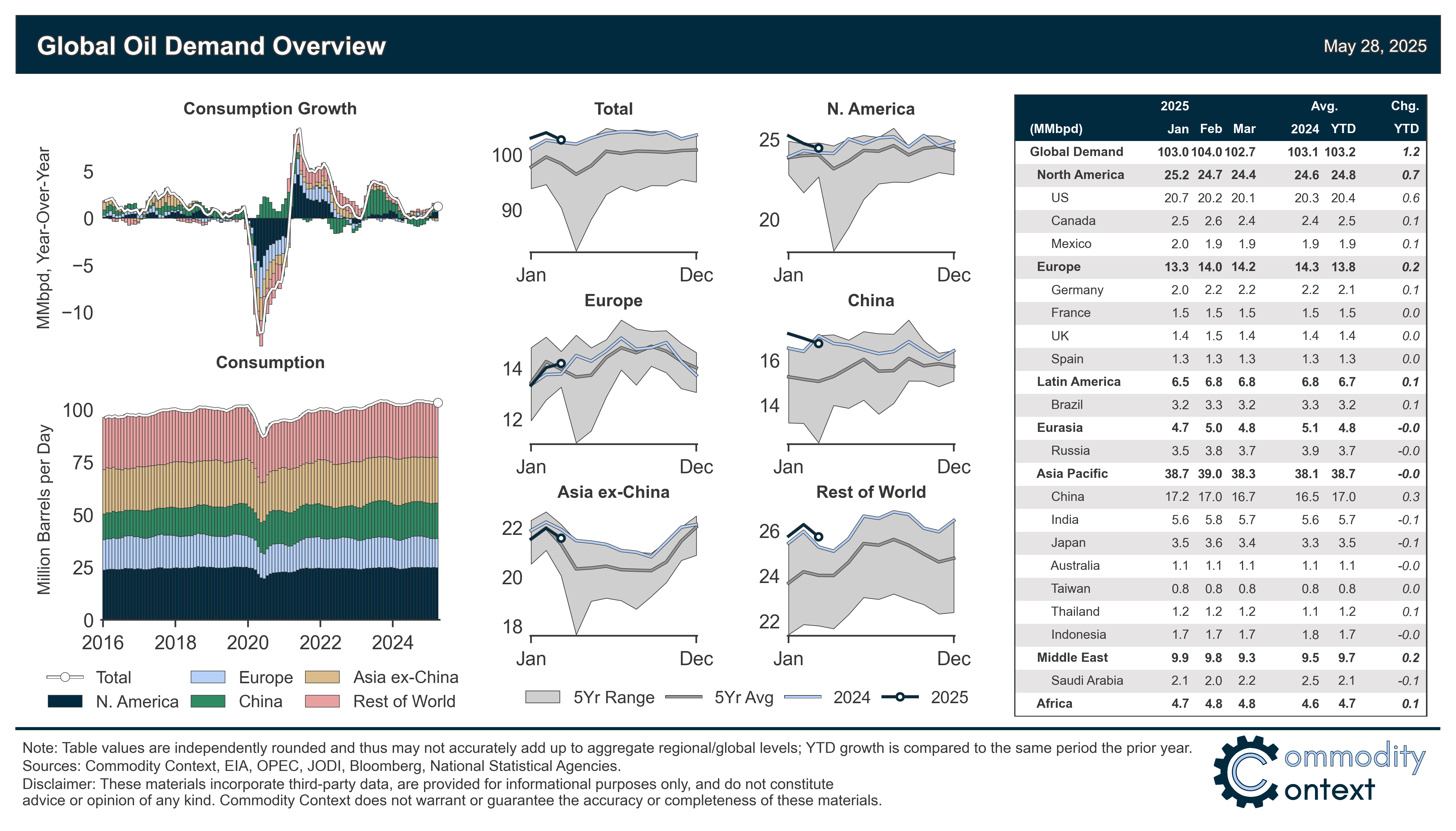

Q1/2025 data indicates a strong start to the year but there are reasons to believe this demand growth trajectory may be a mirage: weak 2024 base effects made outperformance easier and, going forward, trade policy uncertainties pile atop a deeply unfamiliar fundamental foundation.

After a volatile few years, it’s anybody’s guess as to where Chinese demand growth is headed (especially in the face of Trump’s tariffs): early signs of promise have faded again through March and April as demand for gasoline and diesel, in particular, remains weakest.

Ex-China demand growth rests on the shoulders of other emerging markets across developing Asia and Africa; however, the recovery in headline liquids demand in Q1/2025 was notably driven by advanced economies like the United States and Europe.

The drag of US trade policy volatility will only become more visible through the coming months; so, this summer will really prove the mettle of the current marginal petroleum consumer.

Demand has become the de facto speed limit that governs the global oil market. Once upon a time, supply was the primary constraint: produce a barrel and someone somewhere would use it. But times have changed and production technologies have grown immensely more potent; the term “Peak Oil” almost universally refers to oil demand and not, as it meant for decades, the high-water mark for global oil output after which scarcity would grow ever-more constrictive. Yet still, there are ever-proliferating headline-grabbing supply-side storylines to follow, which typically move quicker and are more politically intriguing—from OPEC policy to sanctions. Meanwhile, demand provides the slower-moving, structural backbone against which the market clears.

And that de facto demand growth speed limit has been slow over the past year. Indeed, it appears that China could be shifting towards being a net drag on global oil demand growth from its normal position of primary driver: 2024 was only the second year—alongside COVID-zero 2022—in more than two decades that annual average Chinese consumption declined. While mid-2024 expectations were for a natural bounceback in 2025 (a la 2023), China’s demand growth recovery remains wobbly, ex-China demand growth is far from encouraging, and, to top it all off, President Trump has thrown global trade into a tizzy following the introduction of his “Liberation Day” tariffs. All three major global oil market forecasting agencies—the International Energy Agency (IEA), U.S. Energy Information Administration (EIA), and Organization of the Petroleum Exporting Countries (OPEC)—have now slashed global demand growth forecasts for this year and next.

So, let’s take a closer look at global oil demand growth.