OPEC Supply Risk Smaller Than It May Appear

Overproduction—both officially acknowledged and not—front-runs much of the official return of OPEC+ supply, leaving us in a weaker position today than recognized but with less forward risk than feared

If you’re already subscribed and/or appreciate the free summary, hitting the LIKE button is one of the best ways to support my ongoing research.

OPEC+ production policy has retaken the wheel as the primary driver of the oil market following the rapid acceleration of planned production cut unwinding over the past couple of months and threats to return the entire 2.5 MMbpd tranche of withheld supply by November.

However, there are open questions and debate as to how much the producer group is actually producing and thus what share of the 2.5 MMbpd tranche of withheld supply was even missing from the market when the output hike liftoff began in April.

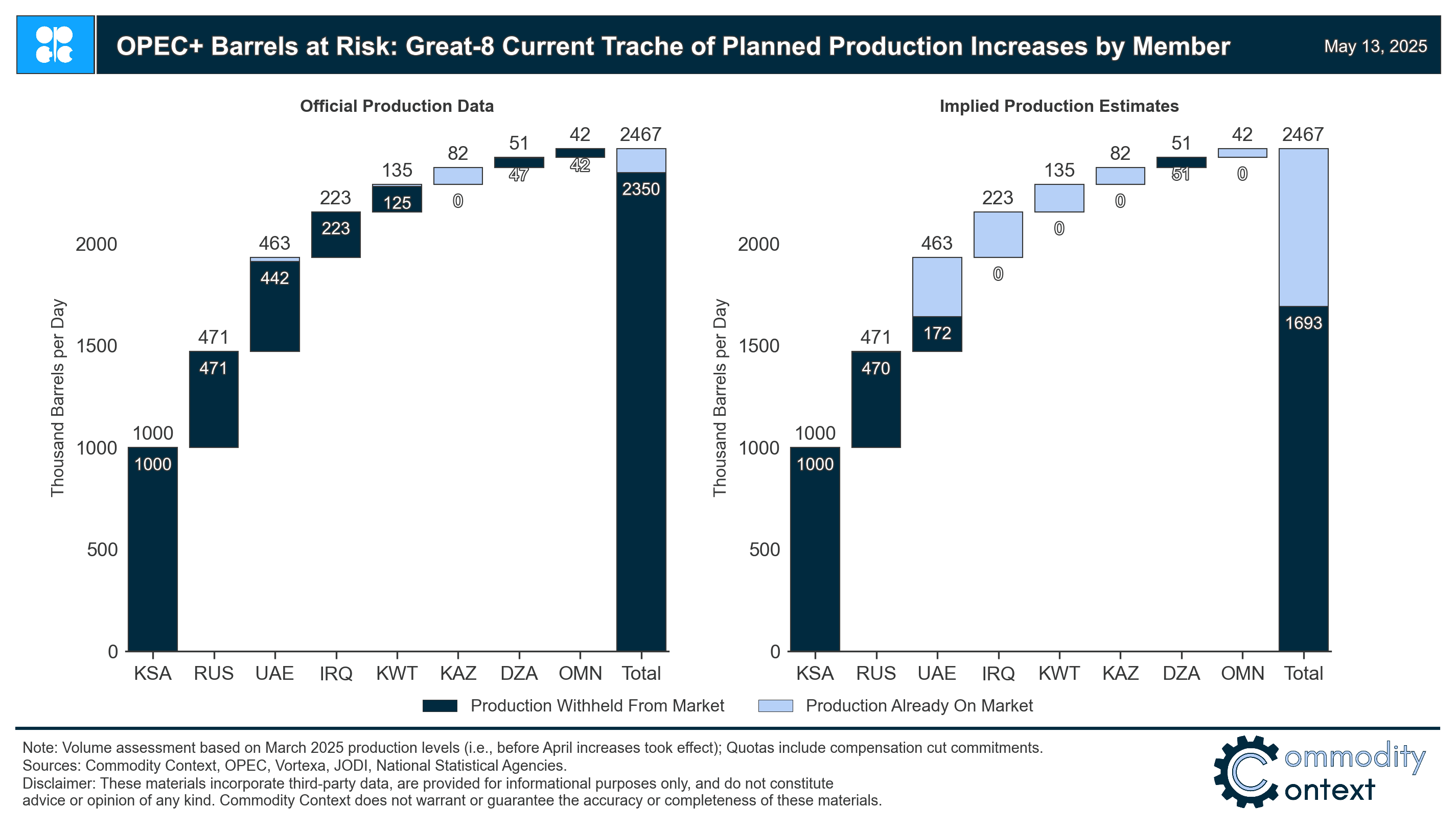

It is well-known, and even officially acknowledged by OPEC, that Kazakhstan’s portion of the planned return (82 kbpd) doesn’t really matter because those barrels—and then some—are already back on the market.

Extending this logic, implied production estimates (see data notes below) shave ~800 kbpd off the broadly anticipated OPEC+ supply risk, a net bullish development compared to current consensus outlook assumptions.

The bulk of the planned supply increases will therefore come from the likes of Saudi Arabia, Russia, and the UAE, though the true degree of near-term OPEC+ supply risk will be driven by realized individual production levels and may be further limited by functional capacity constraints in members like Russia.

OPEC+ has already pledged the return of nearly 1 MMbpd of previously withheld crude oil production between April and June and threatened to return the entire 2.5 MMbpd supply tranche to the market by the end of October. Following on from What’s Driving OPEC’s Dovish Shift?, OPEC began lifting production, after numerous delays, in April and has since tripled the pace of planned output hikes in both May and June. Instead of the previously planned 18 months, this entire slice of OPEC market support might be unwound in 7 months. That’s a lot of oil, very quickly.

If taken at face value, OPEC’s planned and threatened production increases would almost certainly not just push the market into oversupply but thoroughly swamp global balances and crush prices. But, what if we don’t take it at face value? Many analysts are questioning the degree to which official OPEC data accurately reflect realized OPEC+ member supply to the market. At the extreme, it has been argued that virtually all of OPEC’s production cut is already unwound and on the market.

Implied production estimates (see data notes below) shave ~800 kbpd off the broadly anticipated OPEC+ supply risk, a net bullish development compared to the current consensus outlook. This leaves upwards of 1.7 MMbpd of remaining supply—largely withheld by Saudi Arabia, Russia, and the UAE—and is, no doubt, still a substantial volume of crude. The return of these barrels to the market before the end of the year will be a tremendous weight around the neck of oil prices, regardless.

Let’s review the current and pledged production levels of the eight members of the so-called Great 8 subgroup of OPEC+ cutters to better quantify the OPEC+ supply risk.