Iranian Maximum Pressure Redux

Trump’s stated goal of zeroing out Iranian oil exports is the oil market’s key bullish catalyst in 2025, but can it be done and what does it mean for both crude prices and OPEC+ policy?

If you’re already subscribed and/or appreciate the free summary, sharing my research and hitting the LIKE button is one of the best ways to support my ongoing work.

The Trump Administration has reimposed its “Maximum Pressure” campaign against Iran and publicly stated a goal of driving Iranian exports to zero—this is now the most anticipated bullish catalyst for the 2025 oil market.

While the Trump administration has the capacity to materially reduce Iranian oil exports, it will face an entirely different trade landscape compared to 2018; Trump will have to rely on China—rather than allied countries—with its history of opposing and skirting these sanctions.

Anticipated US policy action is expected to (temporarily) dent effective Iranian supply to the market by up to 1 MMbpd; but, absent further sanctions tightening and active maintenance of pressure, it’s likely that Iranian crude marketers, and Chinese importers, will find new workarounds.

Any Iranian supply loss needs to be considered in the context of OPEC+ champing at the bit to return withheld barrels to the market, which both blunts upside price risk and reframes the overarching narrative less as a bullish risk and more as a reduction of bearish OPEC+ deal collapse tail risk.

Earlier this month, President Trump signed a National Security Presidential Memorandum (NPSM) to restore the “Maximum Pressure” campaign against Iran. This is the first step in keeping to his pledge to take a hammer to the Iranian economy, with an explicitly-stated goal of “driving Iran’s oil exports to zero”. The decision to withdraw from the Joint Comprehensive Plan of Action or JCPOA (AKA Iranian nuclear deal) was one of Trump’s central foreign policy directives in his first term and what followed was a so-called “Maximum Pressure” campaign to bolster Washington’s leverage in renegotiating that deal. Trump vowed to clamp down on Iran once again if he were to return to the White House and this policy risk was easily the most cited bullish catalyst for the 2025 oil market following Trump’s reelection last November.

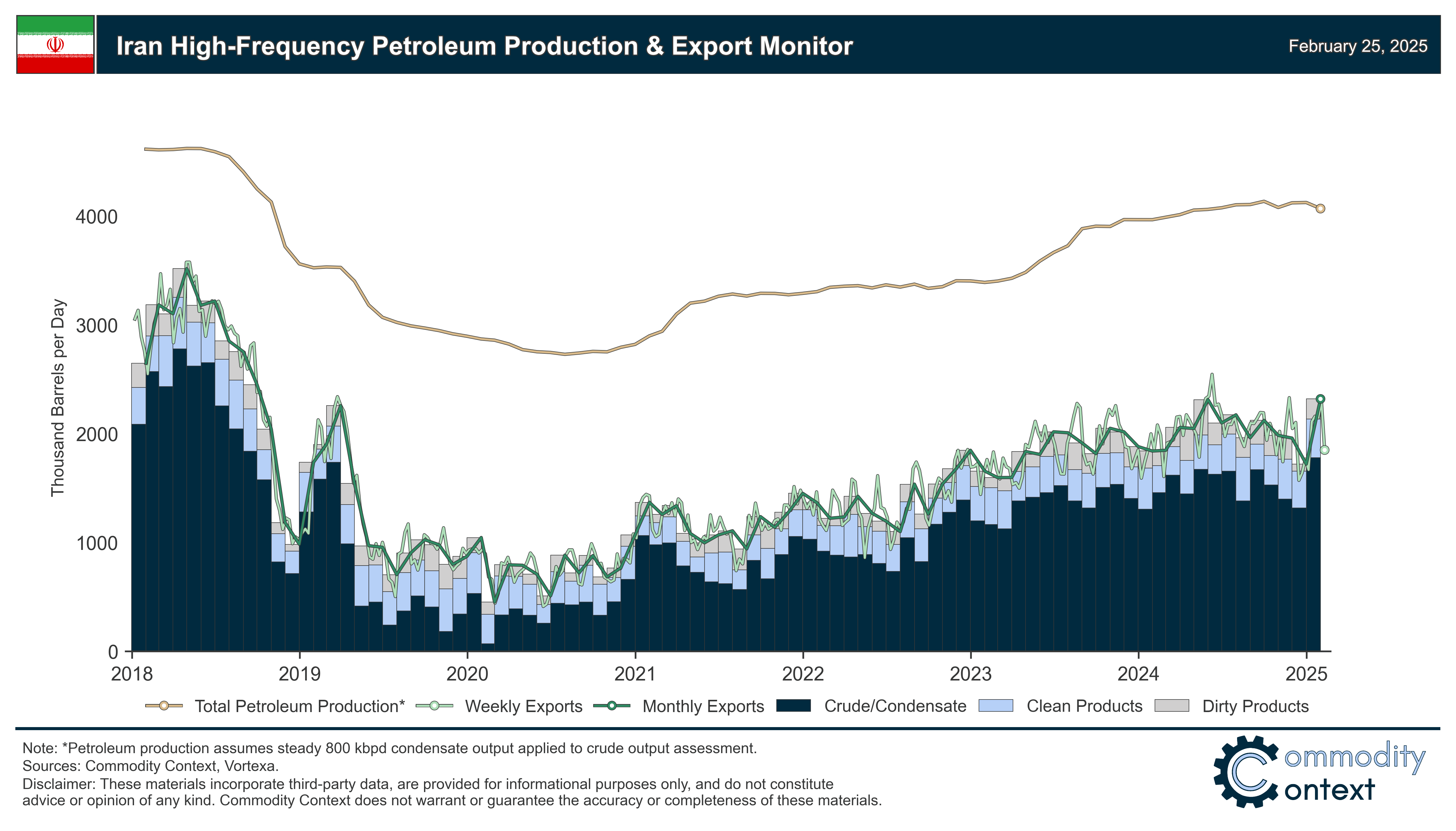

To briefly recap: Iranian oil exports (both crude and refined products) collapsed during Trump’s first term, falling from as much as 3.5 MMbpd in mid-2018 to less than 500 kbpd by early 2020 before climbing again when Biden entered the White House to average more than 2 MMbpd in late 2024. This rebound in Iranian exports was a bearish drag on crude prices that, alongside a final boom in US output, stymied OPEC+’s plans for a tighter oil market in 2023 and forced the producer group’s “temporary” support to evolve into something more structural (see Iran’s Sanctioned Production Renaissance).

Today, the oil market faces the prospect of material losses in Iranian supply, perhaps upwards of ~1 MMbpd, thanks to the US policy pivot back to Maximum Pressure. But, while the Trump administration has the capacity to materially reduce Iranian oil exports, it will face an entirely different trade landscape compared to 2018—including the fact that China is now the overwhelmingly dominant importer of Iranian crude. Moreover, OPEC+ is champing at the bit to return their own long-withheld barrels to the market. In other words, a loss of Iranian exports would put modest, temporary upward pressure on prices but upside will ultimately be capped by OPEC+’s desire to return withheld barrels to the market. Indeed, there’s a strong argument that the US effort to collapse Iranian exports isn’t a straightforward bullish risk at all, but, rather, by releasing pressure within OPEC+, it primarily reduces the probability of the ultimate bearish scenario for the oil market: the rapid and disorderly unwinding of the OPEC+ production deal.