Tough Tariff Talk

Winners, losers, and how 25% US tariffs on Canadian and Mexican oil imports would reroute the flow of barrels across North America

This week has yielded a flurry of media and client inquiries regarding president-elect Trump’s threats of 25% tariffs against imports of Canadian and Mexican goods, including oil, and I wanted to put the current state of my evolving thinking on this novel market risk in one place for readers.

If you’re already subscribed and/or appreciate the free summary, sharing my research and hitting the LIKE button is one of the best ways to support my ongoing work.

While it remains unlikely that the incoming Trump administration will ultimately tariff Canadian crude exports, Trump has now specifically threatened to impose a 25% tariff on all imports from both Canada and Mexico, including oil.

For the US, a 25% tariff on oil import tariffs would inevitably increase consumer pump prices and weaken US refining margins.

For Canada, the threat of tariffs has exposed an acute vulnerability to US price pressure given a lack of export optionality; the degree of pain, however, will largely depend on whether other crude imports are also subject to a tariff. (Mexico is comparatively more insulated)

The threat of tariffs on oil imports runs directly counter to many of Trump’s other pledges, including to reduce US pump prices; but, likely much more importantly for him, it increases leverage in the forthcoming and broader trade renegotiations.

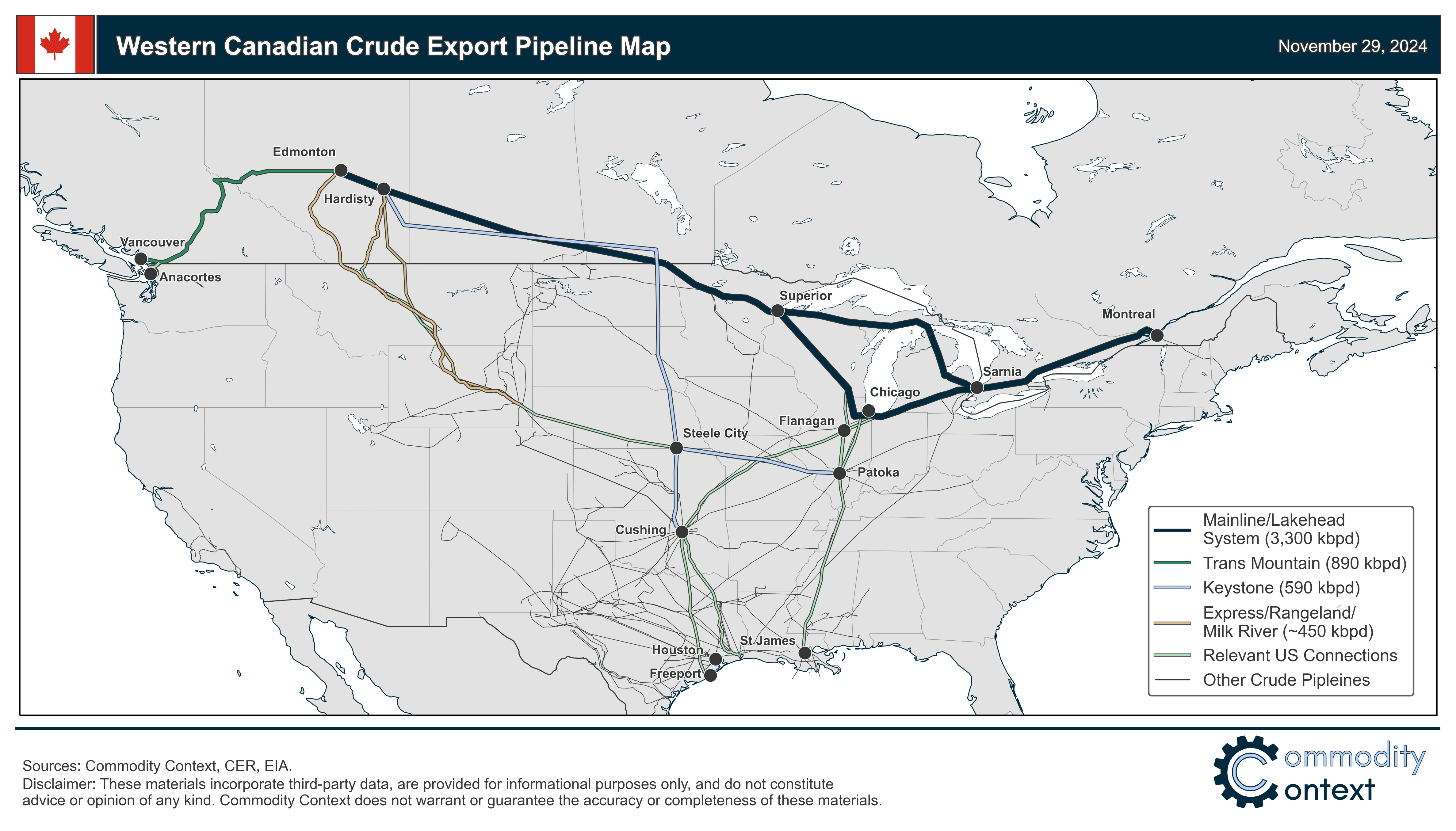

Earlier this month, the possibility that US oil imports could be implicated as part of president-elect Trump’s proposed 10-20% universal tariffs existed but felt deeply unlikely. Ask any analyst and they’d tell you that the probability was vanishingly slim. It seemed even more farfetched that Canadian barrels, specifically, would be included in any Trump tariffs: Canada is a long-time ally and USMCA partner, currently supplies more than half of total US imports, those imports are a type of crude that US drillers can’t supply, and, from an infrastructure perspective, remains the only real source of supply for large swaths of the US (i.e., the Midwest).

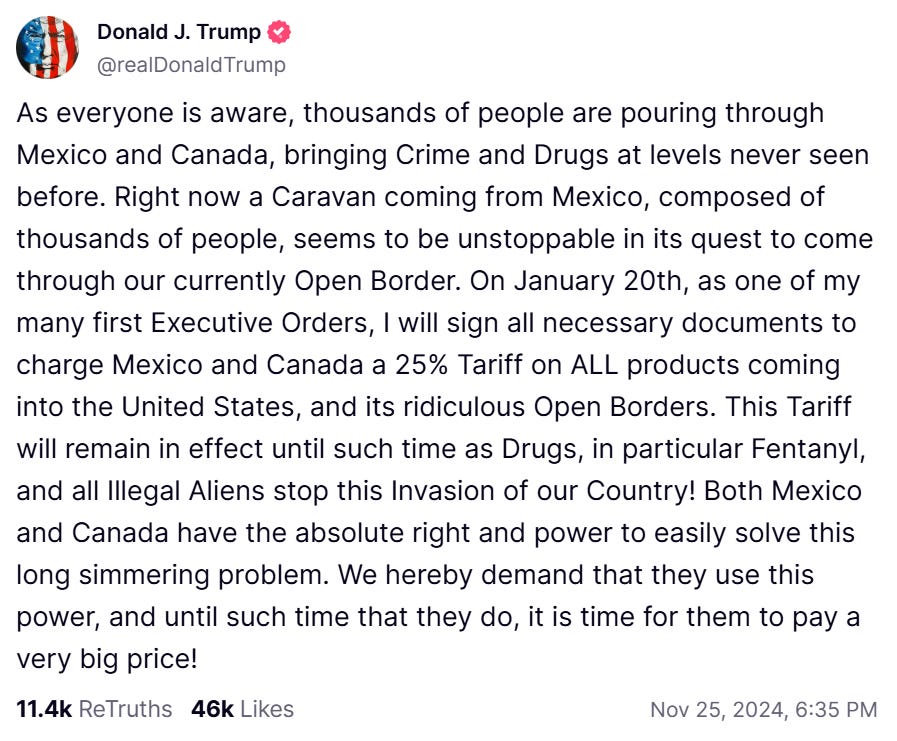

But now, Trump has specifically threatened to impose a 25% tariff on all imports from both Canada and Mexico, an announcement the former and incoming president made on Truth Social this past Monday. Even more concerning, sources with knowledge of Trump’s plans confirmed to Reuters that oil would not be excluded from the tariffs. This confirmation prompted a flurry of protests and warnings from oil and gas industry groups en masse, including the American Fuel and Petrochemical Manufacturers Group, representing US refiners, and the American Petroleum Institute, representing the broader US petroleum industry.

Source: Truth Social

The Canadian and US oil industries have evolved together and are structurally dependent on one another, a relationship I recently explored in depth in Stronger, Together—when I thought, while incredibly unlikely, the scale of the risk warranted detailed analysis to better understand the potential impact. Following on from that research, I co-published a public policy paper with the Canadian Global Affairs Institute (CGAI) —The Co-Evolution of the Canada-U.S. Oil Industry and Possible Implications of Donald Trump’s Re-election—that specifically discussed the risks of US tariffs on Canadian crude exports.

While I continue to believe that the base case scenario does not see tariffs imposed on Canadian barrels, the probability is clearly rising and it’s now worthwhile to take an even closer look: the potential winners, the potential losers, and just how barrels might be rerouted—not just across North America, but globally.