Quick Context: Strategic Release

Quick Context: Strategic Release

Does the White House's SPR release bolster or threaten global energy security?

The Biden Admin announced plans for a sustained release of 1 million barrels of oil per day from the SPR over the next six months, by-far the largest such release in history.

There are the contours of effective policy contained in the White House’s announcement, but a more nuanced approach is required given that this is not necessarily the type of temporary supply loss that the SPR was initially designed to address

A combination of spot selling and future refilling (if committed today) could flatten the curve and enhance the price signal received by US shale and other non-OPEC producers, but it remains to be seen if the Biden Admin is planning or even positioned to pull it off.

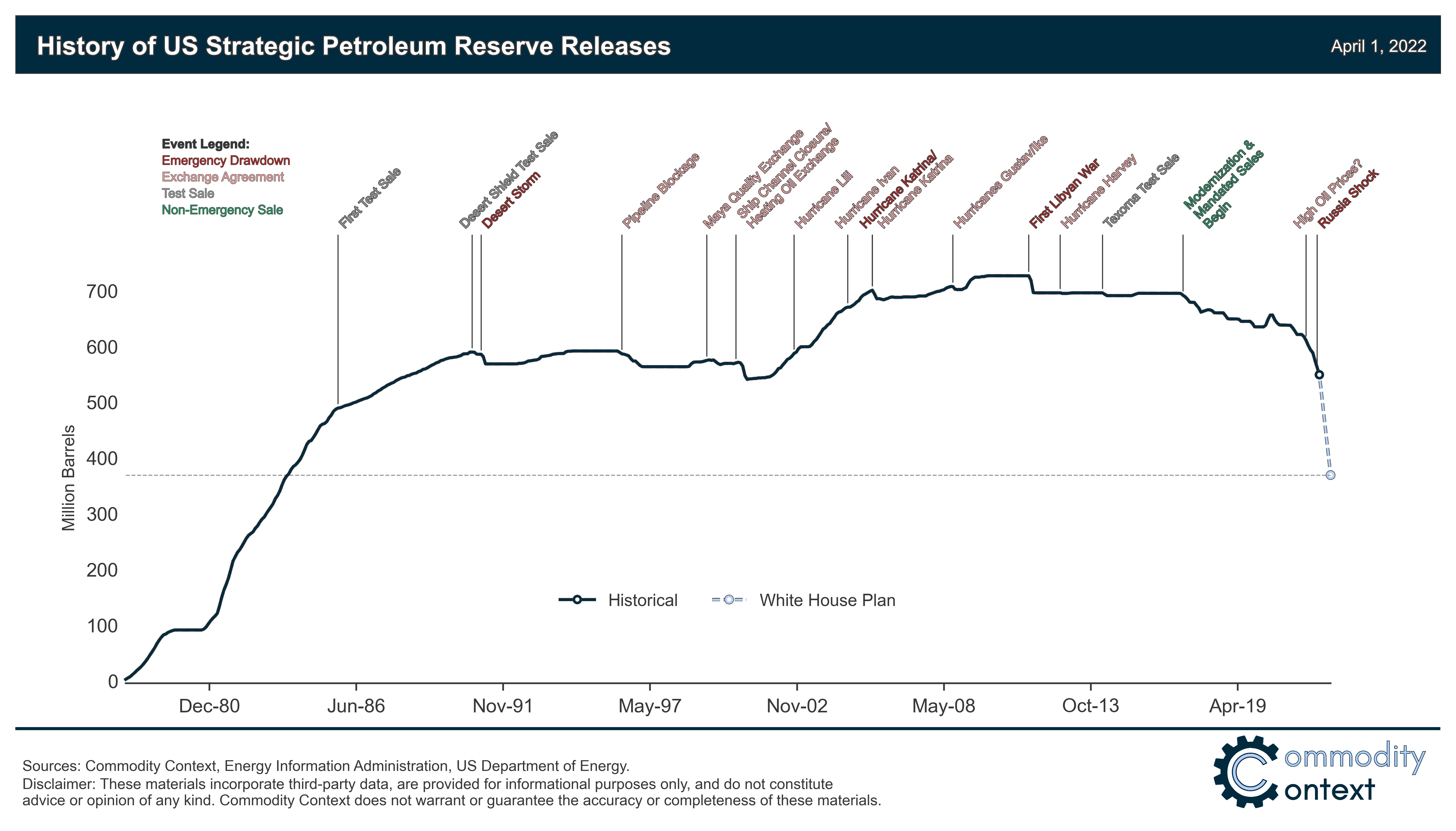

The Biden Administration has announced plans for the largest-ever release from the US Strategic Petroleum Reserve (SPR): 1 million barrels per day (MMbpd) sustained for up to 180 days for a maximum of, you guessed it, 180 million barrels. This release will be supported by smaller contributions from US allies, although those specific details are yet to be made clear. Regardless of any complementary actions, 180 million barrels from the SPR is a big release and would bring the SPR back to its lowest level since 1983 (see chart). In this case, the US SPR alone would become, at least temporarily, the 20th-largest oil supplier in the world, neck and neck with the United Kingdom.

While this is certainly a significant and historic effort, the big question is will it help—or hurt—the oil market’s increasingly precarious balancing act? In short, this is not the traditional purpose of the SPR—and a traditional, simple emergency sale approach applied here would be self-defeating. But there may be a more sophisticated way for the Biden Administration to deploy the SPR that facilitates both the reduction of current prices and the enhancement of effective producer price signals.

Beyond its Traditional Purpose

The traditional purpose of the SPR is to offset temporary supply losses, like a hurricane—not structural supply scarcity stemming from a historic invasion carried out by the world’s second-largest oil exporter. And it’s hard to think of this disruption as anything resembling a temporary supply loss.

If the Russia Shock is truly temporary, then the release will help offset the price pain caused by the anticipated short-term loss of Russian exports in addition to lessening the revenue upside received by Moscow, further pressuring the Kremlin. However, as I pointed out in my last piece (Oil’s Russia-Sized Hole—Part 1), even if peace is reestablished relatively quickly, the Russia Shock cannot just be written-off as a near-term loss of barrels. We could very well see a longer-term enfeebling of one of the world’s largest oil producers that results in a permanent and material loss of Russian production capacity.

The efficacy of a strategic release in the face of a persistent Russia Shock is even more unclear. At first glance, I’d say that the release of this much crude to offset a structural shock is self-defeating: it will blunt the price signal needed for US shale producers, and really all non-Russian producers, to begin investing in and bringing on new production capacity.

Can Biden Walk the Line and Refill the Tanks?

Here’s how price signals are supposed to work in commodity markets: higher prices lead to more supply, lower prices lead to less supply. For this reason, a simple SPR release would yield only short-term relief that would give way to longer-term pain and an even larger supply shortfall than if the White House has just left the SPR alone. This type of policy approach would threaten, rather than bolster, the energy security of the US (as I’ve discussed and warned against before) and its allies.

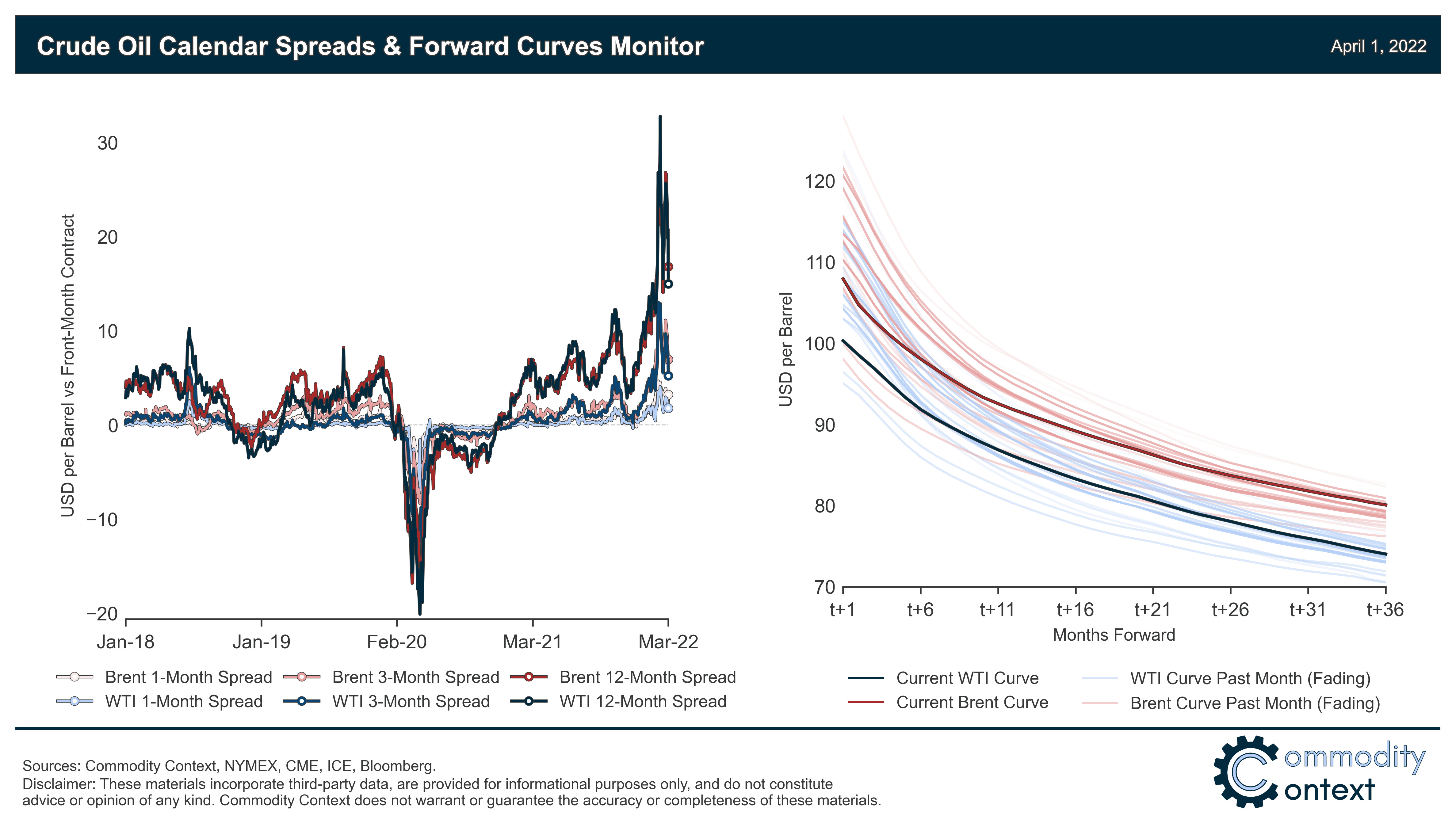

What becomes considerably more interesting is a scenario where the SPR releases crude today and simultaneously buys it back in the future. This is because there is a wrinkle in the price signaling theory that many in industry but few outside industry understand: the headline price today isn’t the only price that matters. On any given day, there is a price for oil delivered next month and every month over the coming years (see chart above), and all these prices matter for producer investment decisions. In fact, extreme backwardation (i.e., a spot price premium relative to future deliveries)—like we’re currently seeing—in the crude oil futures curve is often cited as a reason for a smaller than expected US shale investment response because of how producers typically hedge their production out that same curve.

You see, the SPR is uniquely positioned to act as a discretionary, policy-driven seller and buyer of crude. In this case, the release could be paired with an equivalent purchase of crude to refill the SPR further down the curve—say, in August 2023 where crude is currently trading at $85 per barrel, $15 lower than the current spot. This move would achieve a reduction in current prices while potentially enhancing the effective price signal to producers by lifting the curve further out, allowing for more attractive hedging. This idea of spot sales coupled with future purchases was included in a broader suite of policy proposals published a few weeks ago by Employ America. (Specifically, EA suggests the SPR use its “exchange authority” but the principle is the same; you can read more about legal details of the SPR’s oil acquisition procedure here.)

To wit, the official White House announcement did include a commitment to “use the revenue from the release to restock the Strategic Petroleum Reserve in future years. This will provide a signal of future demand and help encourage domestic production today…” which is great, if not a bit vague. The lack of a clear repurchase plan opens the White House to not unreasonable accusations, given the current energy crisis environment, that they risk selling SPR barrels today at $100 and buying them back later at a much higher price. The White House can counter said accusation by simply buying those barrels today, for future delivery, and completely avoid said risk.

A Few Other Asides

All scenarios—the good, the bad, and the ugly—assume that there are no technical or logistical issues that prevent the SPR from achieving a sustained 1 MMbpd drawdown rate, or any quality-related issues as have caused problems with SPR barrels in the past.

There are also logistical frictions (e.g., transportation, regrading, getting it back into storage, etc.) that will erode the simple arbitrage conveyed by the futures curve (i.e., it won’t be a simple $15 net per barrel). The backwardation is extreme enough, though, that those can likely be accommodated while still turning a theoretical positive return.

There’s also the issue that the SPR release—even if coupled with the buying of longer-dated futures to refill and buttress the back end of the curve—stimulates demand because consumers do care most about prices today. However, the Biden Admin is pretty explicit that its motivation is to lessen the burden on consumers, so I’ll give them a pass on that vector—and it’s still better than a gasoline tax cut.

Conclusion

There are the contours of effective policy contained in the White House’s announcement but, as always, the devil is in the details. On face value, a simple SPR release is not fit-for-purpose—it wrongly assumes there can be a quick resolution of the Russia Shock and ignores the potential for massively distorting price signals for other producers. Instead, I hope to see a more explicit plan to leverage the SPR’s buying power today to refill the SPR in the coming years and enhance the price signal to producers by pulling up the back of the crude futures curve. Absent such re-purchase efforts today, the SPR release risks falling into bad policy territory—an election-year pump-price pander distracting from the intensifying energy price crisis.

Follow me on Twitter where I’ll be tracking this process and yelling about maintaining price signals.

Clicking the LIKE button is one of the best ways to support my research.

First of all, thank you Rory! For what it's worth, my system doesn't yet signal long or short on spot oil but I'll just stick this SPR release in the "unintended consequences of central planners" bucket for now...there's a lot of things in that bucket!