Oil's Russia-Sized Hole—Part 1

Putin’s invasion of Ukraine was like a hammer to an already fragile oil market

The impact of the oil market’s Russia Shock is somewhere between big and truly massive—likely costing the market between 1-4 MMbpd in Russian supply—but remains difficult to estimate even a month into the crisis given the slow pace of contract turnover, still-shifting wartime realities (potential significant peace talk progress announced this morning!), and capricious self-sanctioning behaviour.

Even before Russia [re]crossed the Ukrainian border, the oil market was tight and there was a strong case that prices would need to rise above $100 per barrel to bring on additional sources of supply—and then came the second-largest oil exporter’s overnight transformation to a global pariah state.

Beyond the elephant in the room, there are various other market factors at play. For example, a pullback in demand stemming from China’s increasingly severe COVID lockdowns or the possible return of sanctioned Iranian barrels could soften the Russia Shock, while the reduction of Kazakh flows on the CPC pipeline may further strain supply pressures.

It has somehow already been more than a month since Russian president Vladimir Putin invaded Ukraine and shattered peace in Europe. Before Moscow blindsided the world, all three major oil forecasting agencies were anticipating that the market would loosen and at least a temporarily return to oversupply conditions through 2022. Russia’s overnight transformation from interconnected commodity powerhouse to global pariah state has thrown the already-tight oil market into historic disarray.

The scale of Russia’s role in the global oil market is hard to overstate. Russia is the second- or third-largest producer (neck and neck with Saudi Arabia) and second-largest exporter—and now, the single-biggest problem. The “Russia Shock” is too big, and frankly unknown, to cover in a single post today, so this is Part 1 of what I imagine will be a running series on the structure of Russia’s oil industry, its role in the global oil market, and where things look like they’re headed.

Tight market made tighter

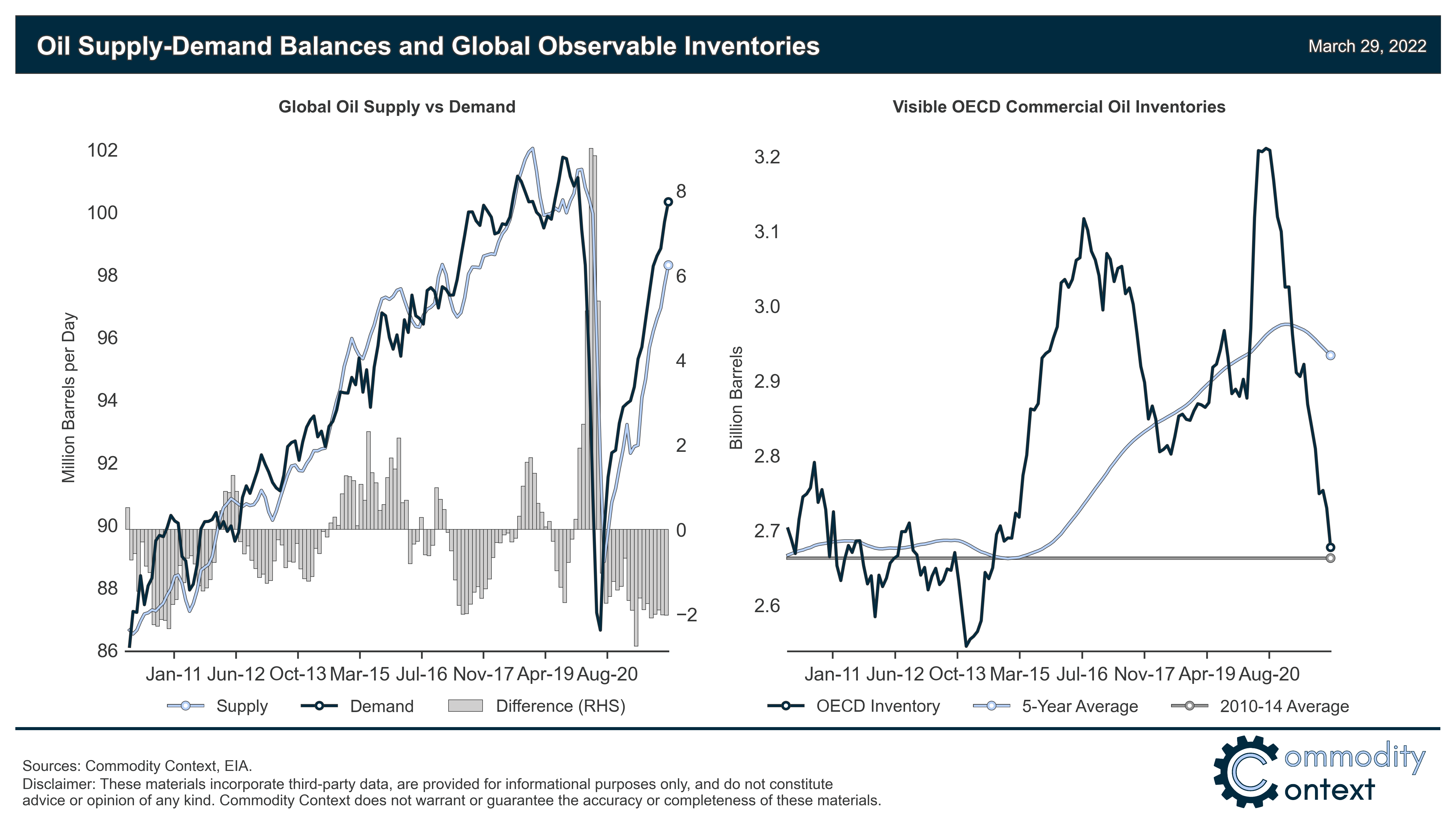

To set the stage, the global oil market was already extremely tight before Russia [re]crossed the Ukrainian border. Current estimates put the average undersupply in 2021 between 1.5-2 million barrels per day (MMbpd), already enough to bring global inventories—that were sitting at all-time highs on the back of early-COVID demand losses—back down to their lowest level since the high-price era of 2010-14 (chart above). Crude prices had risen from around $50 per barrel at the beginning of 2021 to more than $90 by early-2022.

In my last oil market update (before the invasion), I noted that we really needed a bunch of things to go right (shale, OPEC, Russia, etc.) to avoid those tight markets tightening even further and pressing prices well into the $100s per barrel. Instead, we’ve had one big thing go wrong, terribly, horribly wrong. Following the invasion, that steady price appreciation went completely berserk: Brent crude rocketed higher and reached nearly $140 per barrel before briefly falling back into the $90s, bouncing once again back above $120, and then falling again at the beginning of this week. Not the sign of a well-functioning market.

Russia used to export around 7 million barrels of oil and petroleum products per day—about 5MMbpd of crude and condensate and 2 MMbpd of refined petroleum products. Around 5 MMbpd of that total Russian flow (most of the refined products and about half the crude) typically went to Europe, with the balance mostly destined for Asian markets. Russia’s share of Europe’s distillate (i.e., diesel) market is also considerable, creating an even more acute product shortage within the broader crude market crisis. We know we’re going to lose some portion of that supply, but the shambolic nature of the Russia Shock is making it tricky to accurately capture.

Russia off the tracks

Needless to say, the Russia Shock is like a slow-moving train wreck. We can see that the Russian oil industry has very clearly come off the tracks, but it’s impossible at this stage to tell whether the market impact is simply bad (say, 1 MMbpd lost) or outright calamitous (3-4 MMbpd lost).

There are a lot of moving pieces in the Russia Shock. Some are easy to grasp: the United States, Canada, the UK, and Australia have all banned the import of Russian oil. Other pieces are far more squishy: some firms, especially those in the West, have effectively “self-sanctioned”, refusing to touch Russian barrels for fear of legal headaches or, as Shell quickly learned, fierce PR blowback. What we know for sure today is that the differentials borne by Russian crude blends—both Urals in the west and ESPO in the east—have exploded as buyers ratchet back on purchases (chart above)

Still, there are many more pieces that are truly unknown. How widespread is the self-sanctioning amongst Western firms, and how long does it continue? Can prices fall low enough to negate that self-sanctioning aversion? Would firms reestablish trade or partnerships even if the West brokered a deal with Moscow and removed sanctions? Will that self-sanctioning block all the crude going to western Europe, or just some of it? Of the blocked formerly westward-bound barrels, how many will or even can move toward less discerning—or at least more economically desperate amidst this ongoing energy price shock—markets in Asia?

Takes Time to Turn a Tanker

[Chart correction: a previous version of this chart showed the same compositional change but a larger headline decline in exports due to a conversion mistake on my part related to the fact that these shipments only reflect the first 27 days of March. Sincere apologies.]

In addition to the unknowns, the oil market also moves excruciatingly slow relative to the pace of news flow. Oil shipments are typically paid for weeks or more in advance, which means that many of the tankers still leaving Russian ports were bought and paid for before the first Russian shells began to fall on Ukrainian cities. We can expect that the true extent of the export losses will only become clearer over the coming weeks as the tankers leaving Russian ports begin to reflect purchases made after the invasion.

While the picture will continue to evolve over the coming weeks, total seaborne exports thus far in March have only fallen about than ~4%, according to TankerTrackers.com (huge thanks to Samir Madani for his help) but the much bigger story is in the composition of those exports. Western European seaborne purchases are down by more than a quarter, while Indian purchases grew multiple fold as buyers took advantage of extremely attractive pricing. We also saw a large increase in tankers leaving port without a known destination, which likely represents a combination of shy buyers, ship-to-ship transfer plans, or ships just setting sail in hopes of finding a buyer once at sea.

Other Market Balance Complications

And that’s just over the next 6 months. Beyond how this situation evolves in 2022, there’s the very serious question about the longer-term prospects for Russian production as its ostracism from the global community ossifies. Beyond the potentially long-lasting loss of its traditional export customers, Russia’s oil industry has also been severed from much of the global capital market and lost access to many of the key sources of oilfield expertise, from ties cut with former joint-ventures (Shell, Exxon, etc.) and equity stakes (BP) to the withdrawal of major oilfield services companies. It’s going to be immensely difficult, if not impossible, for Russian petroleum engineers to prevent a collapse in crude production, let alone grow output anytime soon.

All of the above considerations are specifically about Russian oil supply—this is without even beginning to factor for everything else going on in the 2022 oil market. The prospect of demand destruction stemming from China’s increasingly severe COVID lockdowns, the US shale patch’s short-circuiting economic response function, OPEC+ coming to the end of its COVID-era deal, the potential easing of sanctions on Iran and Venezuela, and Russia’s months-long throttling back of Kazakh oil exports on the CPC pipeline to repair “storm damage”: these will all have considerable, and still-yet-unknown, impacts to global oil balances, too.

Conclusion

The oil market has always been a difficult one to forecast; but right now, it’s more-or-less impossible. The variables currently at play are so large and uncertainty bands so wide that it’s hard to land on anything approaching a high probability base case. We’re squarely in the land of scenario analysis (which I plan to expand on in Part 2).

At this point, my best guestimate is that the range of possible outcomes will result in between 1-4 MMbpd of Russian supply losses—very big numbers given the current state of the market. Losses at the upper end of that range are unsustainable for long, and prices would need to rise until some combination of more US shale production and demand destruction balanced the market. Unfortunately, we don’t have a great sense today of either of those price thresholds given that shale hasn’t been especially responsive and the price that would prompt meaningful demand destruction is likely quite high, somewhere near or above the $150 per barrel mark.

There really is a strong economic incentive for these barrels to find a home at some price, thus lessening the ultimate supply loss. However, we could very well still see further tightening of the Russia sanctions regime—say, an official pan-European oil import ban or even US secondary sanctions like those imposed on Iran and Venezuela (that would directly bite Asian appetite for even vastly cheaper stranded Russian barrels). On the other hand, this morning’s headlines about progress toward Russia-Ukraine peace negotiations could signal that the worst of the Russia Show is now behind us—unfortunately, it’s still far too early to say.

Clicking the LIKE button is one of the best ways to support my research.

Great read. I'm new here but would like for you to touch on the reasons the future contracts are still showing a reduced price and why that is thanks for your help

Fantastic analysis of the incredibly complex and constantly evolving crude oil market.

I was reflecting this weekend that the reason I find crude oil spot prices (and more broadly strip pricing) so fascinating is because they involve countless considerations; some knowable inputs and some unknowable, some financial elements and some physical, a sprinkle of geopolitics and foreign policy.

As you summed up perfectly - "the oil market has always been a difficult one to forecast; but right now, it’s more-or-less impossible." Well said, Rory. Keep up the great work.