Oil Context Weekly (W34)

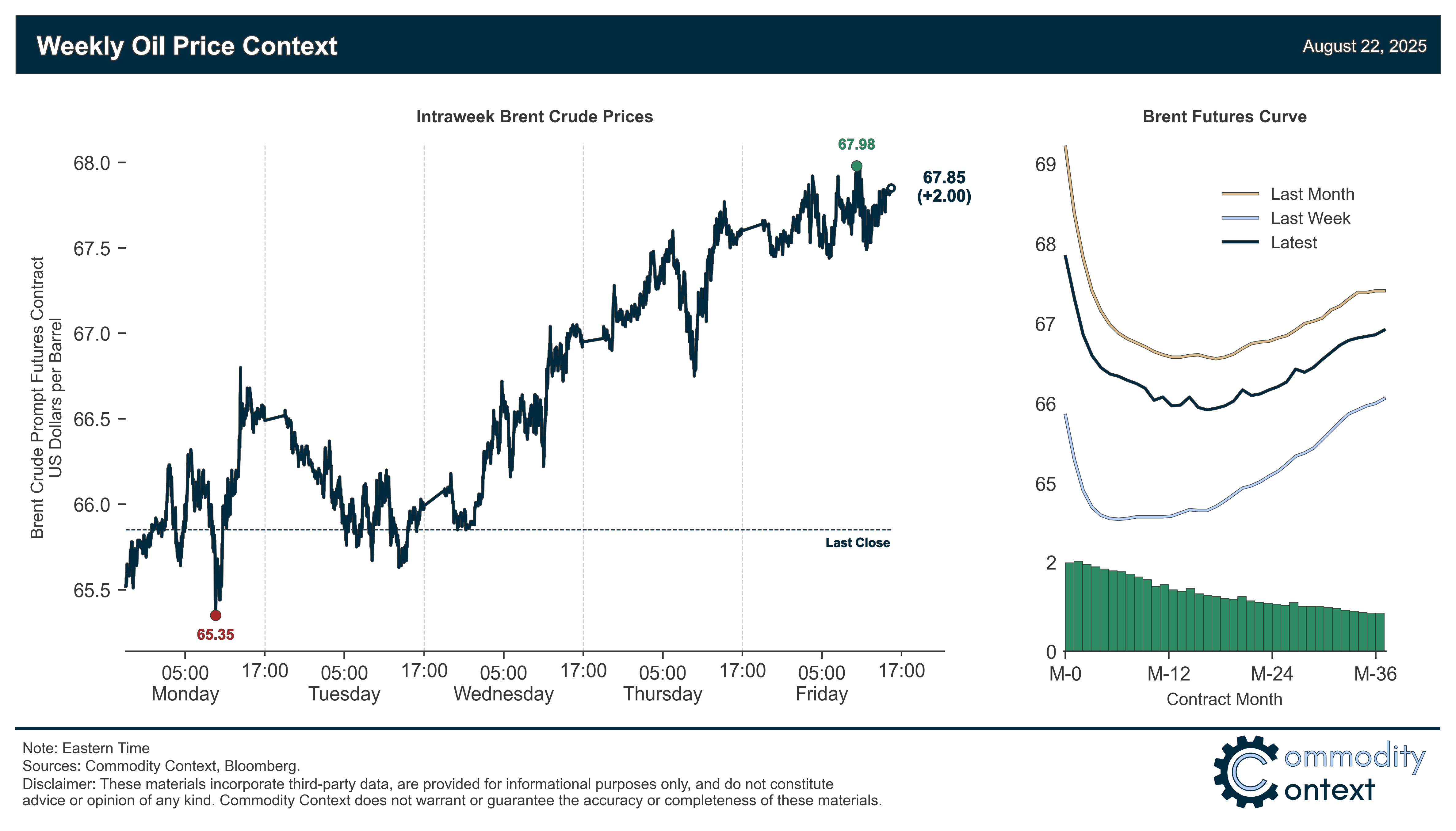

Crude prices gained through the latter half of the week amidst escalating attacks on Russian energy infrastructure and a paring back of some speculative bearishness across the belly of the crude curve

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Reminder: This report includes the first weekly update of the NEW Oil Market Positioning Data Deck (announced earlier this week here), which will provide subscribers with a comprehensive and contextualized view of shifts in petroleum market positioning immediately following the publication of the CFTC and ICE’s Commitments of Traders Reports.

Subscribers can find the link to that 40-page PDF file at the end of this weekly report, immediately following our regular market positioning commentary.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices rose $2/bbl amidst heightened geopolitical tensions—e.g., further attacks on Russian energy infrastructure—and as some overstretched bearish positioning, which had been weighing heavily through the belly of the crude curve, was likely trimmed across the latter half of the week.

Timespreads at the very front of the Brent and WTI curves remained weakly backwardated but we saw signs of improvement through the belly and back of the global benchmark curves; Dubai, meanwhile, is seeing a burst of comparative strength.

Inventories data was mixed between headline draws across the US and Singapore and a modest inflow in ARA Europe; however, the key story is rapidly recovering stocks of middle distillates across all three major geographic consuming hubs.

Refined Products strengthened this week, with gasoline gaining despite normal seasonal weakness on the back of the outage at BP’s refinery in Whiting, IN and diesel remaining firm despite inventory builds thanks to renewed concerns regarding Russian refinery capacity losses stemming from ramped-up Ukrainian attacks.

Market Positioning data revealed that speculators were once again net sellers of crude futures and options contracts, bringing their collective net position to the second lowest level as a share of open interest on record, behind only the rock-bottom September 2024 experience (read Positioned On The Floor for commentary at that time); by any measure speculative positioning in crude contracts is now exceptionally oversold, tilting reversion risk squarely to the upside—indeed, we likely saw the beginning of that covering rally play out through the latter half of the week.

As Well As Ukrainian attacks spread from refineries to crude and throttle Russian oil flow to Central Europe, and Brent sinks below Dubai pricing, opening Atlantic arb to Asia.