Oil & Iran War Context Weekly (W21)

Crude prices sink once more on renewed Iran War negotiation optimism, though major diplomatic hurdles remain and the oil market continues to hemorrhage supply.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

Hey Subscribers, I will be in New York City between June 9th and June 11th for the StoneX Natural Resources Summit and would love to meet up! Please complete this survey if you are interested.

On the latest episode of the Oil Ground Up podcast, I was joined by Edward Fishman, a senior fellow and director of the Maurice R. Greenberg Center for Geoeconomics at the Council on Foreign Relations, as well as the author of one of my favourite books I read last year, Chokepoints: American Power in the Age of Economic Warfare, which provides an incredible account of the development of the US economic statecraft toolkit, with Iran the original proving ground for much of that policy evolution; our conversation focused on sanctions policy backdrop and the kinetic conduct of the Iran War.

For more free oil context, check out my appearances in this CNN Hormuz crisis explainer (video) and on The Simardone Show (video).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

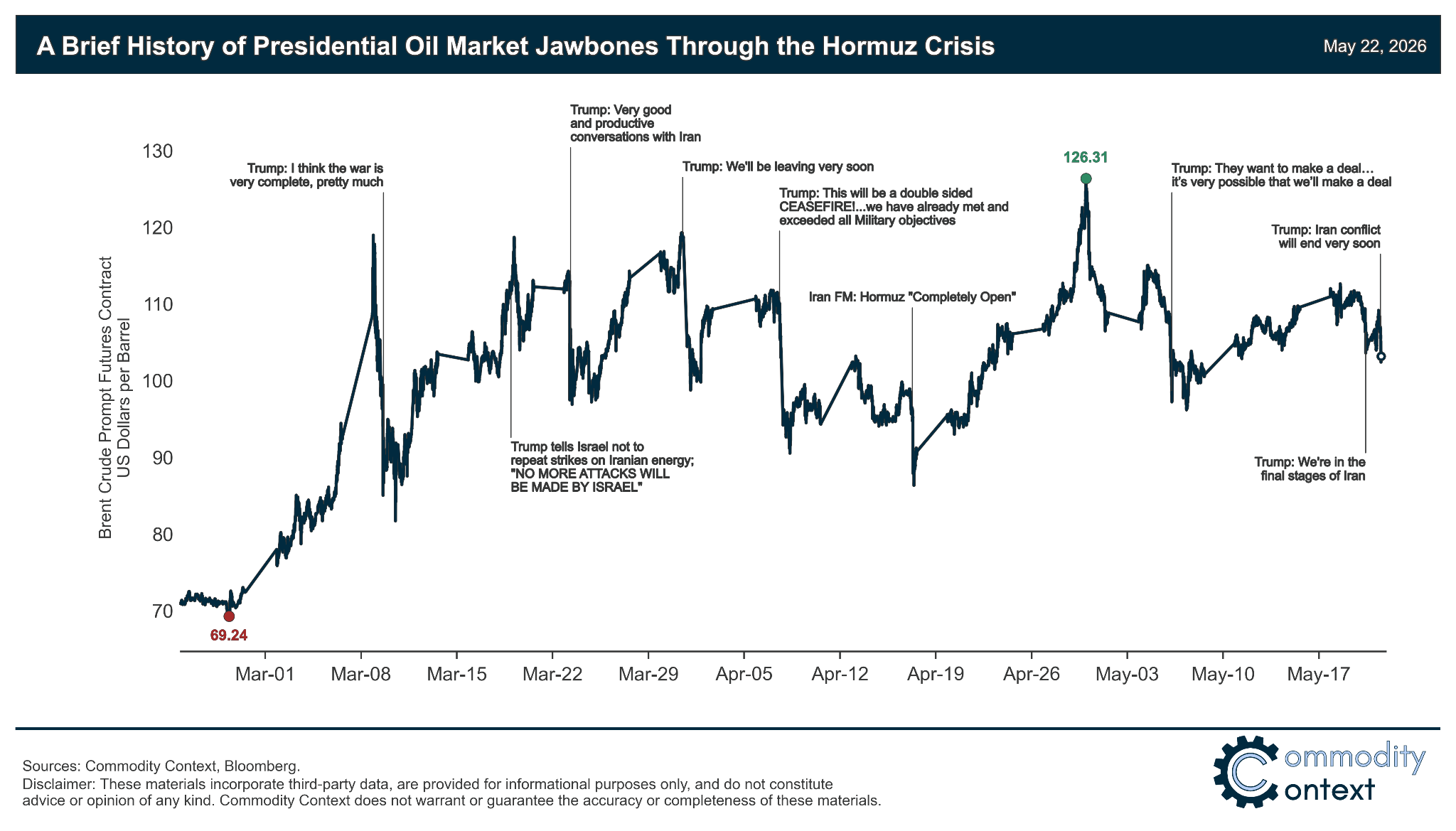

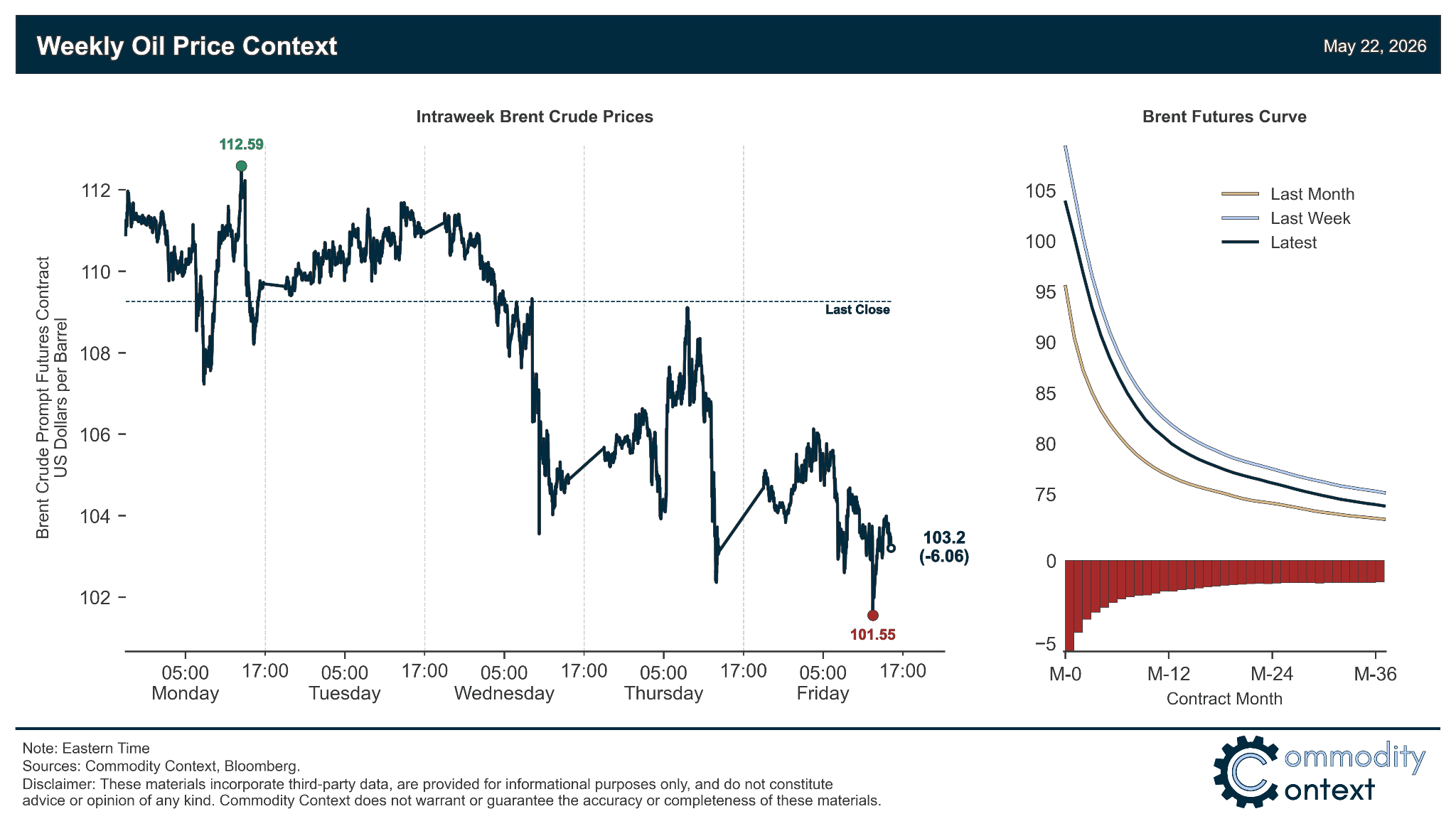

Flat Prices sank roughly $6/bbl on the back of another bout of Iranian negotiation optimism, driven lower by repeated statements by President Trump that “we’re in the final stages of Iran” and the “Iran conflict will end very soon”.

Timespreads followed the trajectory of flat prices lower as prompt Brent timespreads fell from ~$5/bbl to nearer $3/bbl, and all other major benchmarks following suit; this is a reversal of the prevailing trend through the crisis, in which term structure strengthens into month-end contract expiry.

Inventories data were mixed but leaned heavily bullish given the largest SPR-inclusive US crude oil stock draw on record (-17.8 MMbbl w/w) and US gasoline inventories continued to plunge further to the lowest, seasonally-adjusted level since 2014.

Refined Products markets saw diesel crack spreads continue to trade sideways around $60/bbl, below the early-April peak of ~$90/bbl but still nearly 3x the typical level; gasoline margins slipped back to around $40/bbl from the extremely heady nearly $50/bbl reached last week.

Market Positioning data revealed that speculative participants were modest net buyers of crude over the past week-through-Tuesday, though, as has been the trend over the past month, shifts in hot money flows have been small and have, generally, failed to move the needle on pricing relative to broader physical participant influence; that said, speculative positions remain high relative to the pre-war norm and, thus, represent a lingering downside risk to prices should we see a real breakthrough in negotiations.

As Well As another week defined by Iran War negotiation hopes and jawbone market interventions; still watching the bouncing diplomatic ball; handicapping the odds of a return to war; and Iran announces new Hormuz transit regime and regulatory body in the Persian Gulf Strait Authority (PGSA).

What Happened This Week