Oil & Iran War Context Weekly (W20)

Crude prices rise back toward $110 and term structure firms again as US-Iran talks stall out and Trump’s trip to China fails to yield any meaningful breakthrough.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

This week, I joined Jimmy Connors of Bloor Street Capital (video) and MacroVoices (podcast, 56:00 onward).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

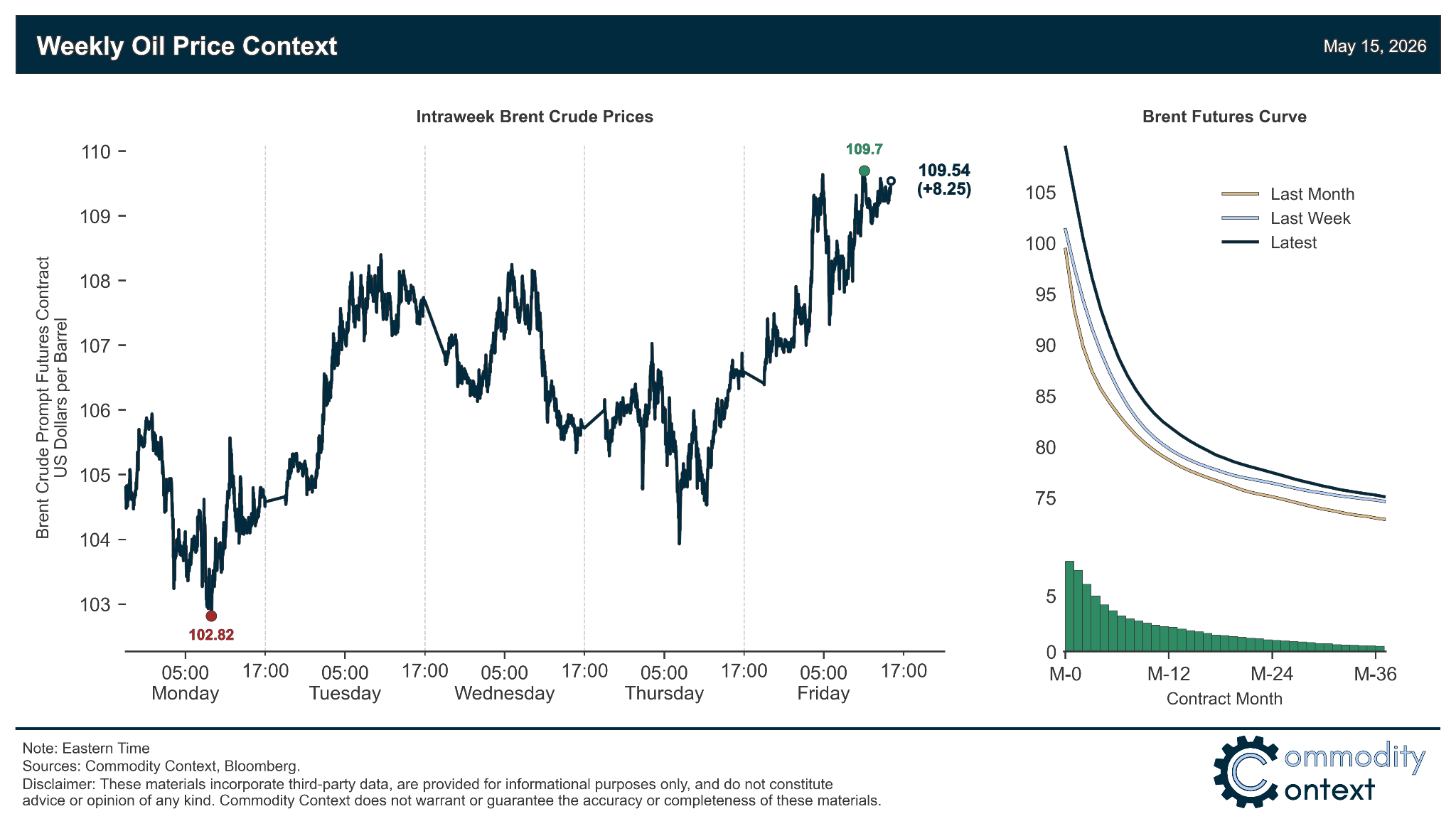

Summary

Flat Prices rose ~$8/bbl for Brent to finish just shy of $110/bbl as last week’s optimism that a deal might be reached began to fade amidst deadlocked US-Iran talks and no meaningful progress coming out of Trump’s trip to China this week.

Timespreads bottomed on Monday and then gradually grinded higher, repeating the well-trodden path of buyer wariness through the first half of the month before being forced to bid more aggressively ahead of contract expiry; the back of the curve, too, continues to rerate higher as global inventories are depleted.

Inventories data was mixed but still leaned bullish given another large US draw and ARA European stocks down to ever more precarious seasonal levels; Singaporean stocks notched a small build after three consecutive weekly draws.

Refined Products markets continue to indicate mounting tightness in US gasoline markets, with New York Harbor gasoline crack spreads rising to within striking range of the all-time high set through the energy crisis summer of 2022.

Market Positioning data confirmed the steepest week of proportional speculative selling of major crude contracts since the beginning of the war; however, while still elevated, hot money flows have had an increasingly inconsequential effect on the crude pricing complex compared to their typically outsized role in non-crisis markets.

As Well As Hopes disappointed that China summit would yield Hormuz breakthrough; US-Iran talks thoroughly stalled on nuclear bottleneck; the crucial difference between Hormuz crossings and real production relief; Iranian onshore inventories continue to rise amidst collapse in tanker loadings; US SPR release hits all-time high outflow rate; UAE to double pipeline reroute capacity around Strait of Hormuz; and Ottawa and Alberta advance West Coast pipeline plan.