Oil & Iran War Context Weekly (W19)

Crude prices pull back, once again, on hopes of a diplomatic resolution to the Hormuz stoppage despite a resurgence of violence to levels not seen since the announcement of the ceasefire last month.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

On the latest episode of the Oil Ground Up podcast, I was joined by Eric Nuttall, a partner and senior portfolio manager with Ninepoint Partners LP, where he manages the Ninepoint Energy Fund and Ninepoint Energy Income Fund; our discussion focused on the unprecedented Hormuz energy crisis, how the largest energy shock in history is affecting the value of North American oil and gas producing companies, and what “the day after Hormuz” looks like for the global oil market.

For additional context, check out my appearances on CBC’s Power and Politics (video), the Arc Energy Ideas Podcast (audio), the Majority Report (video), and TopTV (video).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

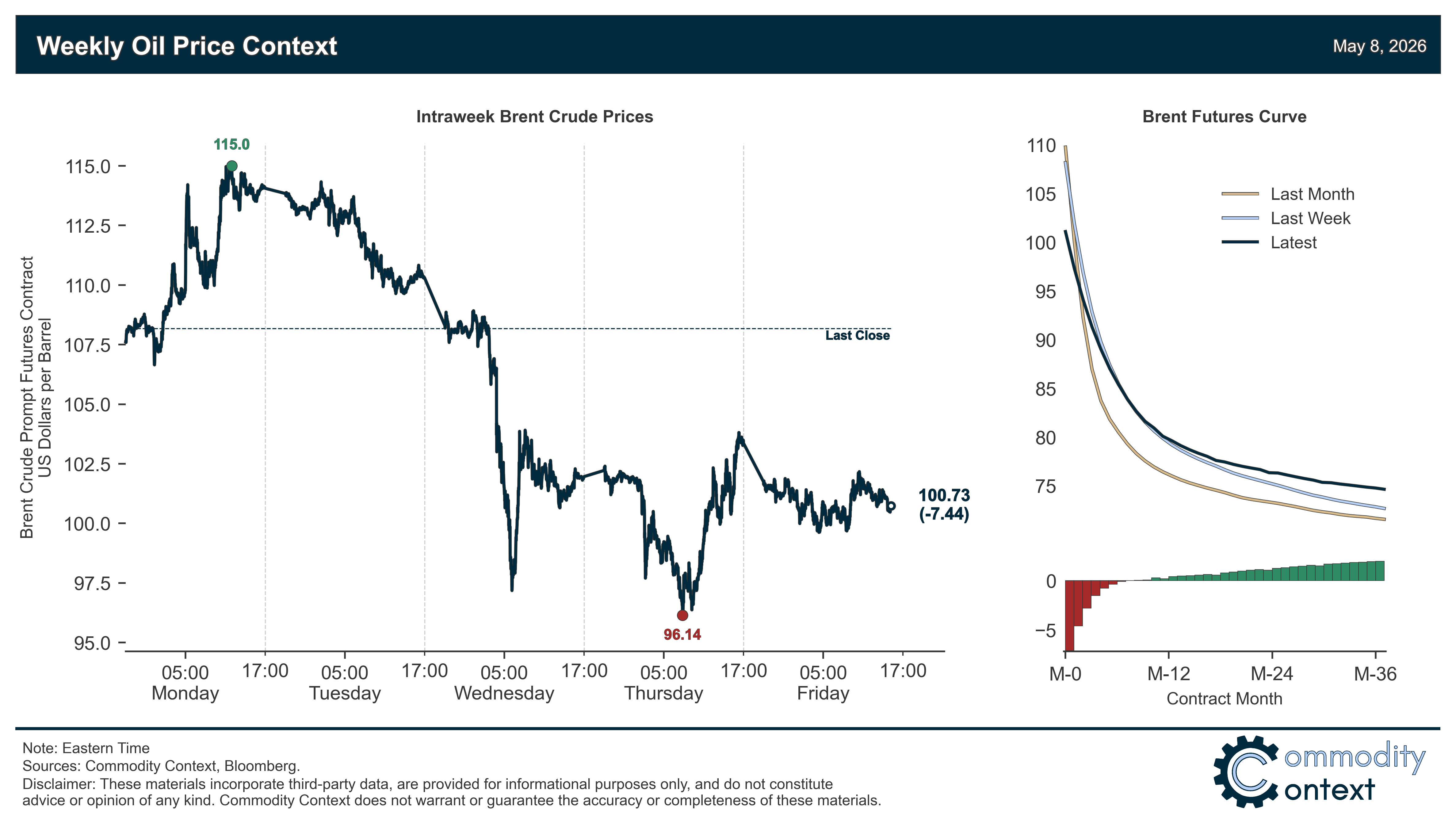

Flat Prices are down ~$7.50/bbl with Brent ending the session around $100.50/bbl; prices shot up on the back of escalating regional violence early in the week but pulled back sharply on Wednesday on yet more news of a potential peace agreement before bouncing around the $100/bbl mark.

Timespreads rolled over alongside flat pricing in a pattern that we’ve come to know: structure tightens into futures contract expiration and loosens through early month trading as the market holds out for some kind of resolution to the Hormuz crisis.

Inventories data revealed a resumption of draws across all major hubs—and last week’s delayed Singaporean inventory data confirmed back-to-back, large declines; US high-frequency data—now amongst the most important in the oil market—shows stocks continuing to decline at a rapid rate, although half the pace this week vs. last.

Refined Products markets continue to richly price middle distillates, like diesel and jet fuel, but relative laggard gasoline is closing the gap; in the US, refining margins for the dominant road fuel are now roughly double the seasonal norm amidst plunging stocks and the need to attract gasoline cargoes to the East Coast.

Market Positioning data confirmed that speculators were modest net sellers of crude futures and options contracts, but that pricing shifts continue to vastly exceed what can be explained by hot money moves and indicates that physical market participants are still driving the bus through the crisis.

As Well As Hormuz transits far from free, US blockade enforcement picks up, a very violent week in the Strait, negotiating the pace and staging of negotiations, and Iran’s new shipping process.