Oil & Iran War Context Weekly (W18)

Crude prices climb amidst ongoing deadlocked diplomacy, the third month of the Iran War, breaching the billion lost barrel threshold, and the UAE announcing an abrupt departure from OPEC.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

On the latest episode of the Oil Ground Up Podcast, I spoke with Michelle Bockmann about the unprecedented disruption in global oil flows following the effective closure of the Strait of Hormuz, the tricks in tracking the shadowing passage of ships through the critical maritime chokepoint, and assessments of the efficacy of the US’ ongoing blockade.

For more free oil context, check out my appearances on The Great Simplification podcast (video), the Bankless Podcast (video), and Breaking Points (video), as well as my latest column in The Dispatch (print).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

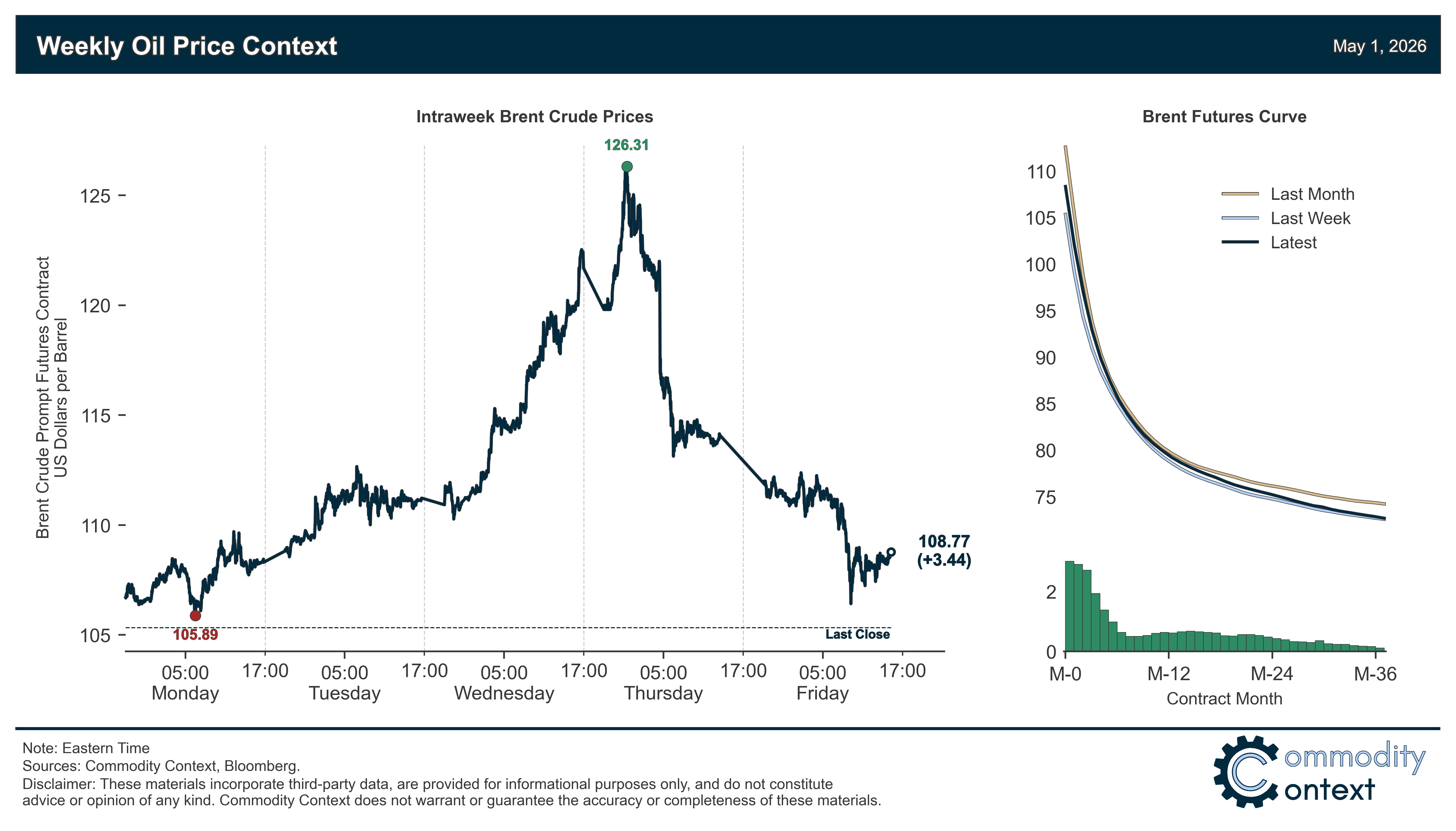

Flat Prices spiraled higher through the final day of Brent’s June contract expiry, hitting a crisis high of more than $126/bbl in early Asian trading before collapsing more than $12/bbl through the end of the day and settling around $114/bbl; prompt Brent crude prices rose $3/bbl on the week while the July Brent contract (now prompt) rose $9/bbl.

Timespreads were relatively flat albeit at crisis levels of backwardation, save a sharp spasm in Brent’s prompt timespread on the final day of the June construct’s trading; Brent prompt spreads, now trading July at prompt, sit above $6/bbl, WTI above $5/bbl, and Dubai around $4/bbl, with Brent DFLs still most steeply backwardated at ~$7.50/bbl.

Inventories data was mixed but dominated by a massive >-24 million barrel draw from US stockpiles, including -17 MMbbl of commercial stocks and -7.1 MMbbl of SPR crude; the US draw proved especially important for market sentiment, crystallizing the mounting global scarcity with highly visible and transparent data.

Refined Products markets continued to be driven by the rapid rise in gasoline prices, which outpaced crude again as gasoline crack spreads rose to their highest level since the energy crisis summer of 2022; diesel margins, meanwhile, remain acutely elevated (~$60/bbl) but traded flat-ish.

Market Positioning data confirmed that speculators were, once again, modest buyers of crude futures and options contracts, lifting their net position as a share of open interest to the highest of the Hormuz crisis; positioning-related risk remains squarely to the downside should these participants look to rapidly liquidate their length—likely amplified by a reaccumulation of currently depressed short interest; speculative positioning in gasoline contracts is on the high end but still lower late-2025 and an unlikely driver of the current RBOB rally.

As Well As Breaching the billion barrel threshold; the UAE’s abrupt departure from OPEC; Iran-US Diplomatic Digest; Trump weighs longer blockade to “explode” Iran’s oil industry; US SPR release rate rising above 1 MMbpd for the first time since 2022; Treasury clarifies that Iranian toll payments are sanctions violations; and Trump approves key permit for Bridge Pipeline Expansion to resurrect Keystone XL.