Oil & Iran War Context Weekly (W16)

Crude prices cratered and term structure flattened on Friday following Iran’s declaration that Hormuz is “open” despite the fact that little traffic has actually managed to cross the Strait today.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

In the latest episode of the Oil Ground Up podcast, I spoke with Adi Imsirovic, a long-time oil trader who now lectures at the University of Oxford and has written many books on the history of oil trading, the mechanics of the Brent crude complex, and the theory of price discovery. Our discussion focused on the connection between the physical and financial (i.e., paper) oil markets and what record-breaking backwardation means for the oil market.

This week, I spoke with MacroVoices (podcast, 48:00-forward), Facts vs Feelings (video), Competent Man (video), MacroHive (podcast), and Wall Street Journal (print).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

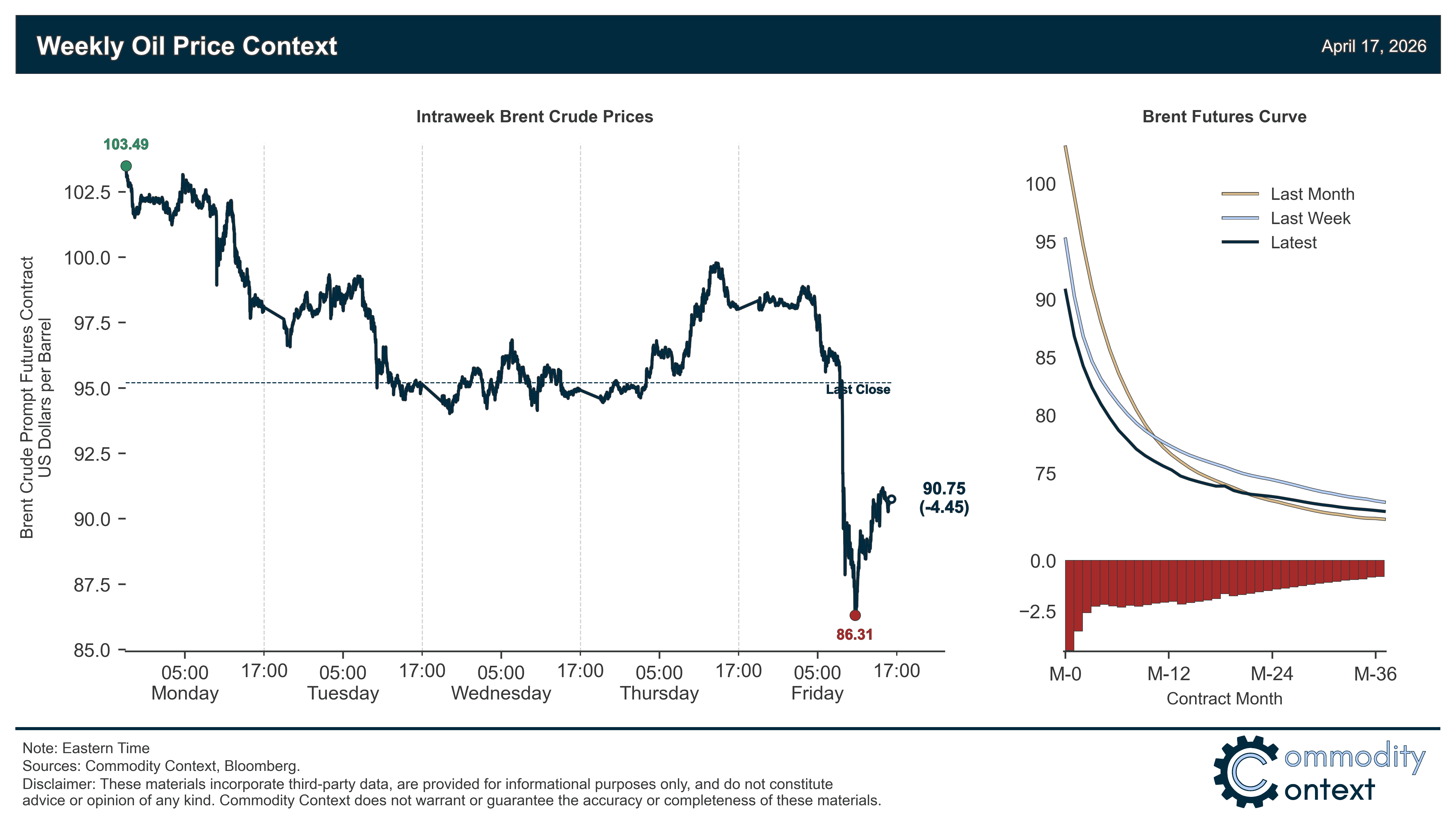

Flat Prices fell by ~$5/bbl for Brent to finish just above $90/bbl following a violent, near $10/bbl rout in crude prices that followed an Iranian announcement that the Strait of Hormuz was “completely open” (many caveats, discussed below).

Timespreads pulled back sharply alongside flat pricing as prompt timespreads of all major benchmarks fell back to their least backwardated level since early March; however, Brent prompt spreads and DFL spreads are still at ~$4/bbl and these are well above any other “normal” period (prompt timespreads are typically measured in cents!).

Inventories data were mixed given a large counterseasonal US draw, a modest decline in European stocks, and a large inflow into Singaporean storage tanks; US crude stocks fell on the week for the first time in nearly two months as a large armada of tankers heads for the US Gulf Coast.

Refined Products markets saw diesel crack spreads plunge alongside crude back to just more than $52/bbl in NYH vs. Brent; gasoline refining margins have continued to march higher, finishing at >$35/bbl vs. a seasonal norm nearer $20/bbl.

Market Positioning data confirmed that speculators were net sellers of crude contracts, but that as of Tuesday their net position remained very elevated relative to the trend of the past year; while those positions have likely come in notably following today’s sharp selloff, they surely remain elevated and, should de-escalation continue, will begin to contribute more meaningfully to selling pressure.

As Well As Today’s “complete opening” doesn’t really change anything, yet; The US blockade that began on Monday; Still considerable work to arrive at any durable end to the conflict; Still down nearly 1bn barrels in the most optimistic view of the supply outlook; and The split between “physical” and “paper” barrels (spoiler: it’s all backwardation!).