Oil & Iran War Context Weekly (W13)

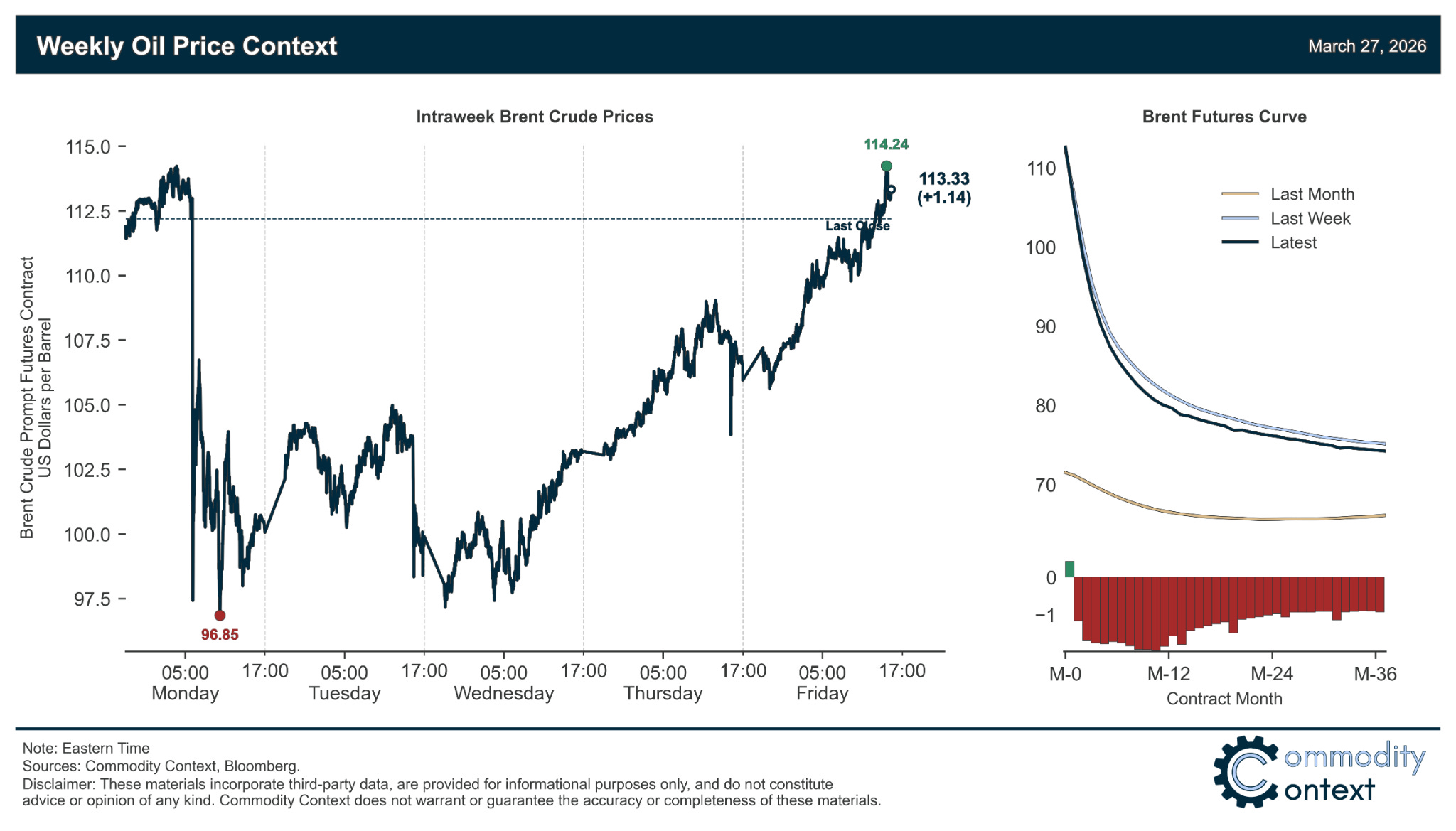

Crude prices rose modestly on the week after recovering from a Trump jawbone-driven rout on Monday given no real resolution to the Hormuz stoppage, and term structure keeps getting tighter.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices rose modestly, ending the week just more than $1/bbl higher than last Friday’s close, but that small w/w change masked considerable volatility over the course of the week, with crude collapsing more than $15/bbl on Monday following a de-escalatory post from President Trump, before prices continued to grind their way higher again on the lack of any firm progress on reopening the Strait of Hormuz.

Timespreads strengthened further, with prompt Brent backwardation rising to >$7/bbl from $4/bbl and Brent DFL spreads—the closest to the physical spot market—rose to all-time highs of >$10/bbl; WTI also saw prompt backwardation more than double to more than $5/bbl from $2/bbl and Dubai remains the major benchmark futures contract with the steepest backwardation at >$10/bbl.

Inventories data, paradoxically, came in relatively bearish given builds across the US, ARA Europe, and Singapore, despite exploding backwardation across both crude and refined products curves; part of this can be attributed to the fact that physical scarcity is still taking time to arrive in the most visible markets and another part can be explained by an initial boost in stocks driven by precautionary demand that manifests are physical hoarding (also seen in 2022).

Refined Products remain dominated by convulsions in the middle distillates market, with US diesel crack spreads (vs. Brent) >$70/bbl, which, while down slightly from the $90/bbl high on Wednesday, is more than double where the year started; jet fuel remains the tightest of the middle distillate products, with Asia the epicenter of that tightness.

Market Positioning data confirmed a modest reduction in net speculative positioning in major crude contracts, which dovetails nicely with roughly flat prices; however, while speculative crude positions remain extremely high, both price gains in crude and crack spread improvements for diesel have notably outpaced any hot money inflows and, for diesel and gasoil specifically, refining margins have continued to soar despite pullbacks in spec positioning in middle distillate contracts.

As Well As presidential jawboning has kept crude prices in check but verbal efficacy is waning; colossal volume of shut-in Gulf production will take months to restart; and Ukraine intensifies attacks on Russian oil and gas infrastructure to ensure the Kremlin doesn’t profit off the Iran War.