Oil Context Weekly (W20)

Crude prices posted their first weekly gain in more than a month on easing US debt ceiling concerns and despite key calendar spreads that continue to highlight lackluster spot market conditions.

Happy Friday,

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

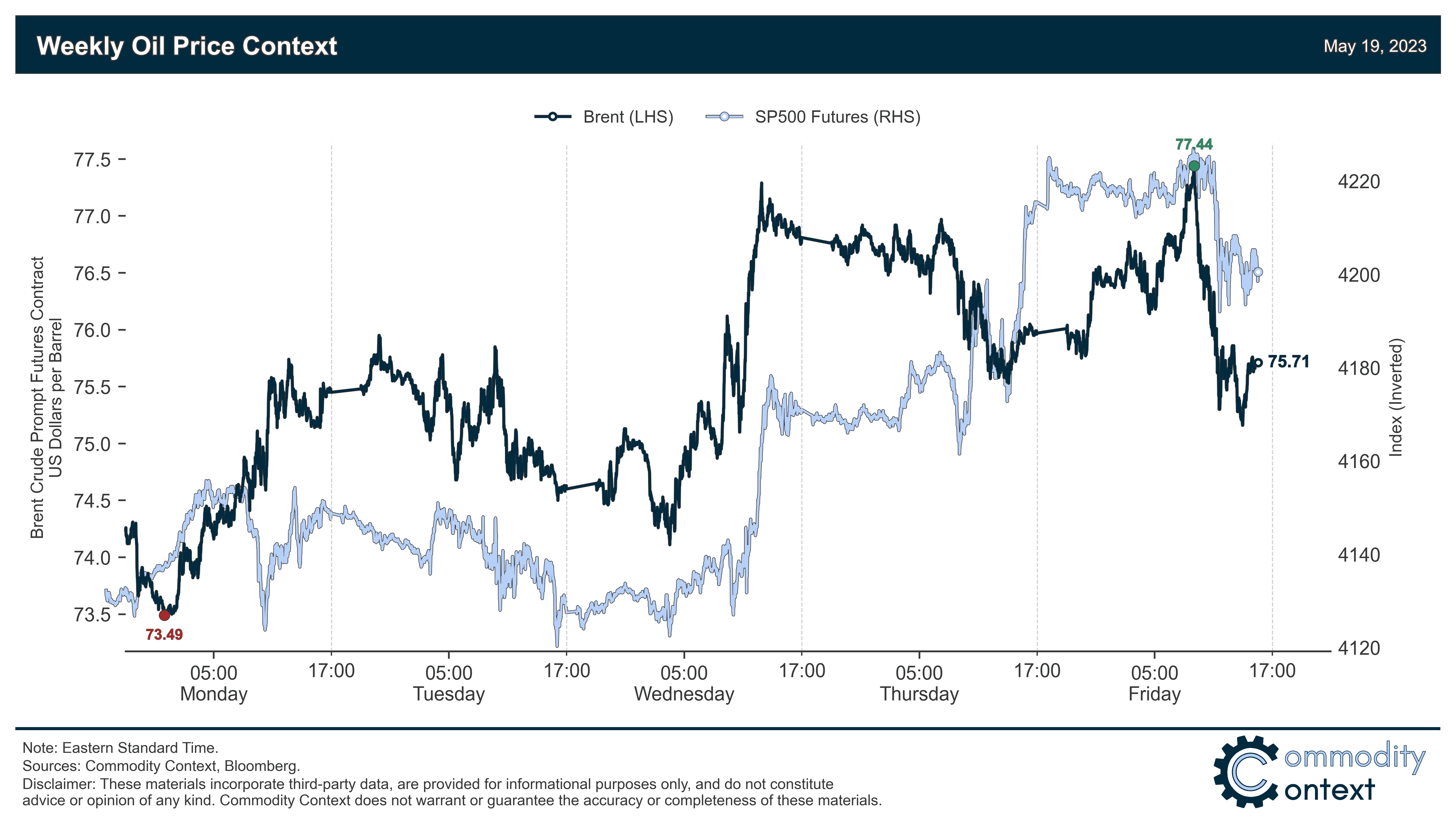

Flat Prices rose by $1.50/bbl to reach ~$76/bbl to mark the first weekly oil gain in more than a month, benefiting from renewed optimism re: the US debt ceiling standoff.

Calendar Spreads remain split; bellwether spreads, like Dec23/Dec24, are locked at the hip with flat prices and ended the week up, while prompt spreads weakened steadily through most of the week before finding a floor on Friday.

Inventories data were mixed but learned bearish as modest draws across Singapore (-0.9 MMbbl) and ARA Europe (-0.6 MMbbl) were swamped by a sizable build in commercial petroleum stocks in the US (+7.6 MMbbl), which was driven by the the largest increase in crude inventories in 3 months.

Refined Products strengthened this week with diesel cracks gaining ~$2/bbl and gasoline cracks gaining ~$6/bbl; year-to-date, we’ve seen diesel generally fall back to earth (from it’s absurd crisis-era heights), but the value of most other fuels including gasoline, high-sulphur fuel oil, LPG, and naphtha have all since recovered materially, unwinding much of the core imbalance that I discussed a few week’s ago in Refiners’ Unbalanced Barrel.

Positioning data confirmed the fourth consecutive week of speculative selling pressure in major crude contracts and the net position as a share of total open interest is within a hair of the mid-March low, tipping position normalization risk squarely to the upside.

SPR Solicitation Correction: In my hot take on the SPR refill solicitation, I raised a specific concern regarding what I thought to be a maximum price clause; I have since learned that the clause governs maximum contract value, such that the quantity, rather than the price, would be adjusted in an event of a big price move (i.e., to keep the total contract value from exceeding the budgeted amount).