Refiners’ Unbalanced Barrel

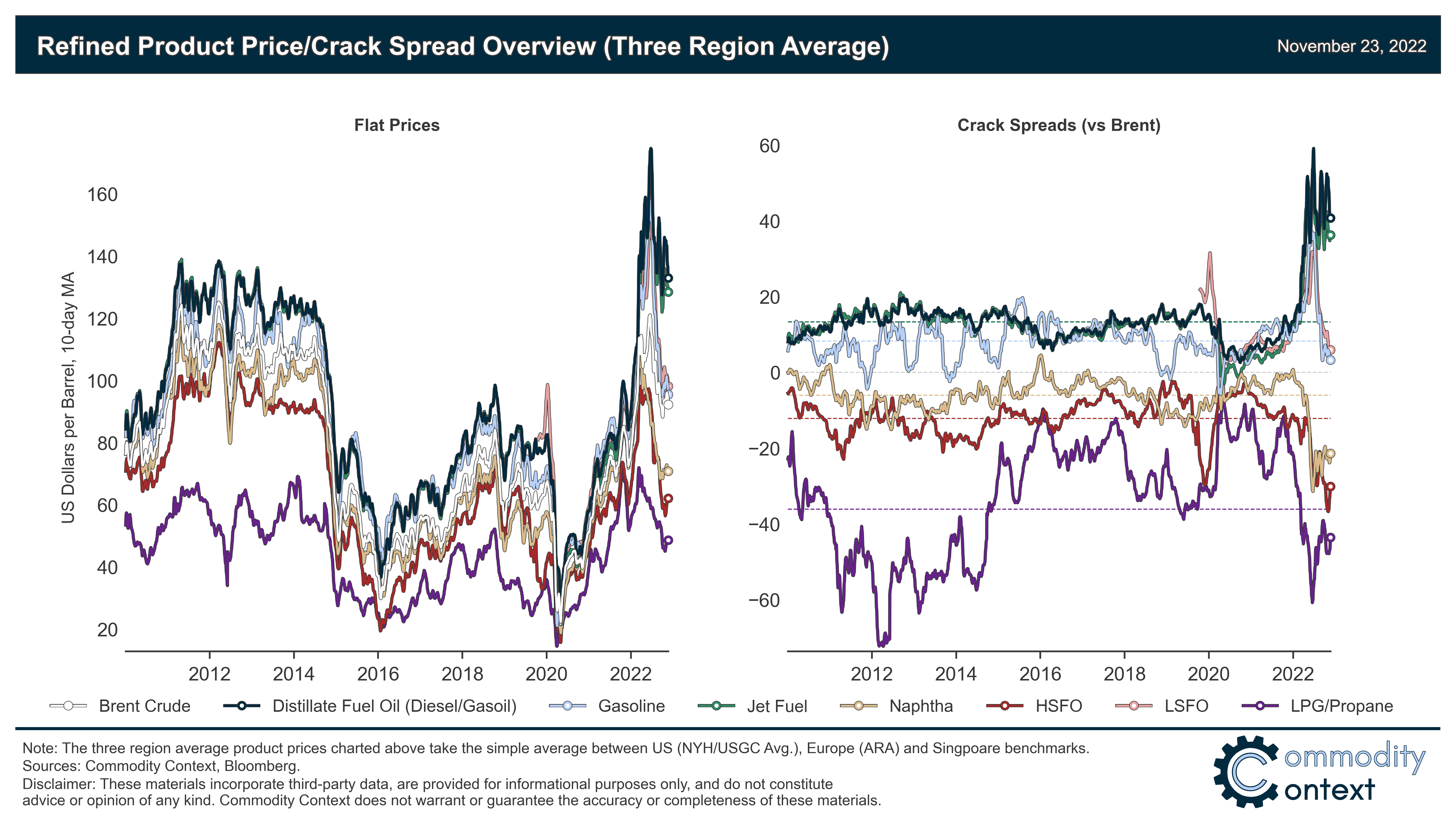

While middle distillates refining margins remain near all-time highs, all other major refined products are far weaker—with product cracks below year-ago and long-run average levels.

Over the coming months I will begin digging deeper into the downstream (i.e., refined product) side of the global petroleum market, beginning with this overview of relative product prices on a global basis before bringing it back to North American refining balances (to tie into the North American Oil Data Deck series), product-by-product deep-dives, and special cases like the particularly acute tightness in the US Northeast and the likely impact of embargoes against Russian refined products beginning in February.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

We currently face one of the starkest refinery capacity crises in modern history, driven by pandemic-shuttered refineries and the delayed startup of planned capacity additions, reduced Chinese exports on the back of longer-term environmental goals, and logistical chaos related to Russian product flow disruptions—the last of which will only be inflamed by the upcoming embargoes and price caps.

Total visible middle distillate (diesel, gasoil, jet fuel) inventories sit at 13% (100 MMbbl) below the trailing 5-year average and well outside the 5-year range, confirming the crisis-level tightness expressed in crack spreads; it’s hard to see how refining output, especially for diesel, can meaningfully meet demand in the near-term.

However, not all petroleum products are facing extreme demand pressures given weak underlying petrochemical product demand, China’s COVID-zero lockdowns, and sky-high power/natural gas prices in Europe; and yet, those tight middle distillates markets around the world are pressing refinery utilization higher and, with it, the supply of gasoline, LPG, naphtha, fuel oil and others.

In the near-term, this contradictory dynamic seems destined to persist until either new refineries come online or, more likely, diesel demand eases—and the differentiated end-market dynamics will continue to play an outsized role in the demand for crude over the coming year.

I know you've noticed that there isn’t nearly enough diesel in the market today; conditions are so tight that the crack spreads for middle distillates (i.e., diesel, gasoil, and jet fuel) have set record upon record this year. But what you may not have noticed is the relative oversupply of virtually all over petroleum products. Unlike middle distillate crack spreads that are sitting at nearly three-fold their long-run (2010-present) average, the crack spreads of gasoline, naphtha, LPG, and high sulphur fuel oil are all below their historical norm.

It’s safe to say that differentiated end-market dynamics will play an outsized role in the demand for crude over the coming year. Even if you don’t care about the nitty gritty of end-fuel markets, these dynamics are critical for understanding refinery profitability and, thus, the overall demand for crude oil.