Chinese Demand Destruction or Strategic Supply?

Despite a ~40% collapse in Chinese crude imports, data point to massive Chinese market support in the form of heavy SPR releases (both crude and refined products) rather than true demand destruction.

If you’re already subscribed and/or like the free summary bullets, hitting the LIKE button is one of the best ways to support my research.

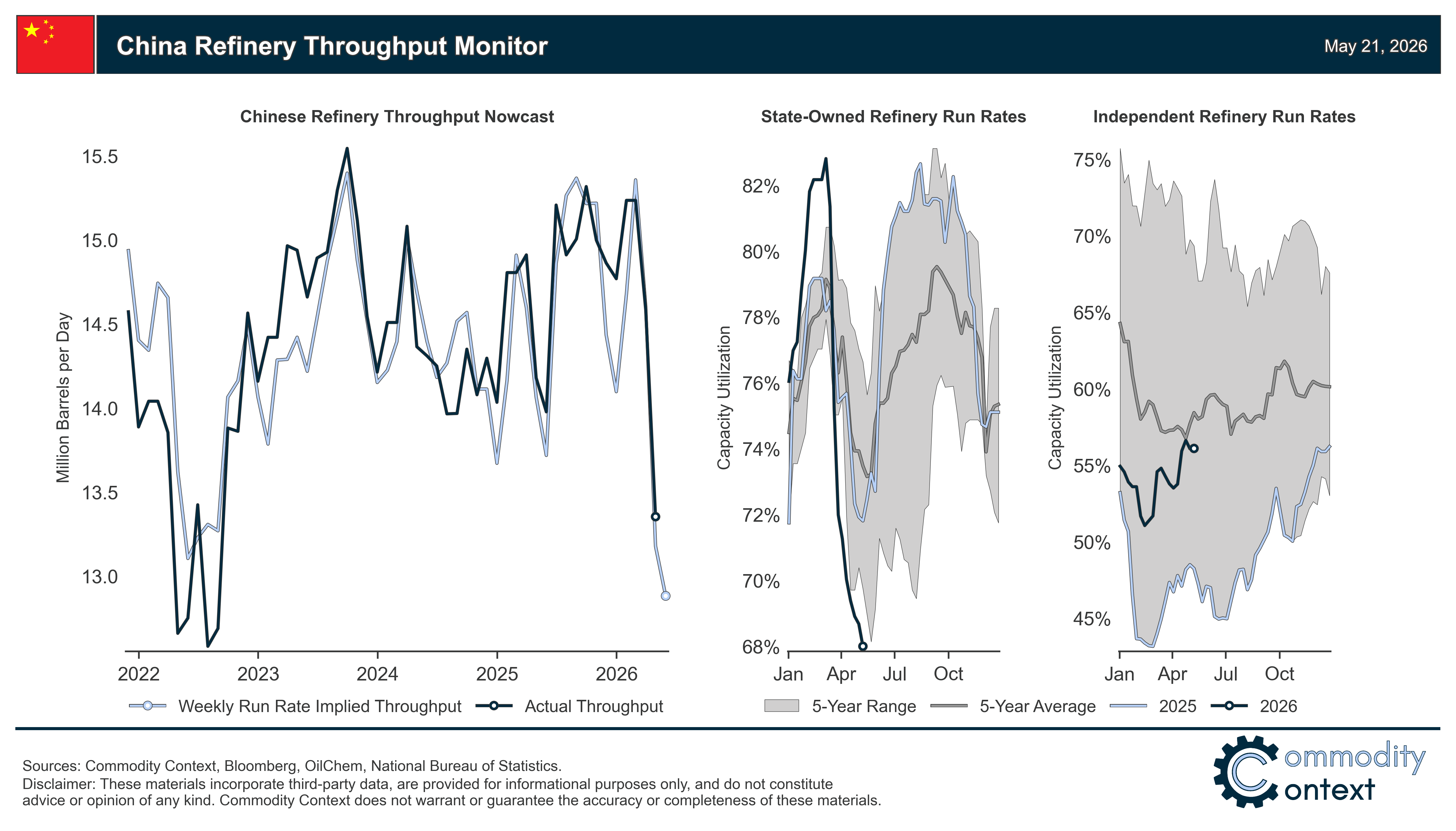

Our normal indicators of China’s petroleum demand have collapsed, from a more than 40% reduction in crude imports to the steepest contraction in domestic Chinese refining activity since COVID-zero in 2022.

However, mobility indicators remain robust and show minimal signs of true demand destruction, with flights, truck traffic, and road congestion all sitting at healthy levels.

The pullback in imports far outpaces the pullback in refining runs, which, in turn, outpaces any evidence of a retrenchment in end-user activity; in addition, visible inventory data has remained flat-to-higher.

This incongruence of flows indicates a high likelihood that the Chinese government is injecting a substantial volume of strategic petroleum stocks—both crude and finished products—into the market, providing critical supply relief to Hormuz-starved Asia and buying additional time before the scarcity panic really bites.

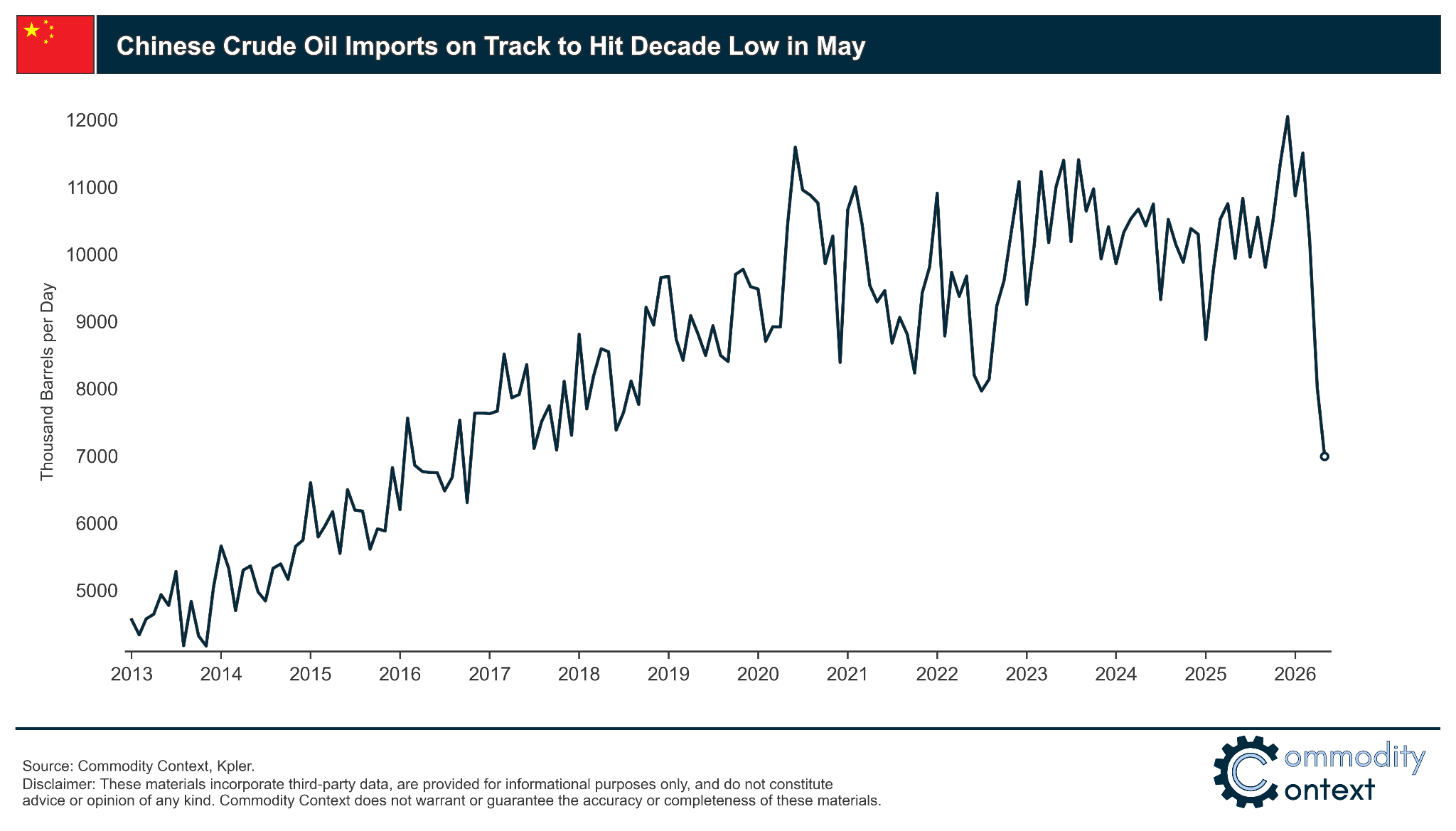

The financial consequences of the closure of the Strait of Hormuz are accumulating slower than initially expected (read: Sanguine Strait Stoppage). One argument is that material demand destruction is already visible in one of the world’s most important markets: China. As the largest and most variable demand centre in Asia, China is very much “ground zero” for how the Hormuz Crisis is playing out. Indeed, we have already seen a measurable, 40% decrease in Chinese crude imports from 11.5 MMbpd in February to a May month-to-date average of less than 7 MMbpd.

Digging in, there is a confusing assortment of volatile trade and refining data to parse. Chinese crude imports have fallen faster than refinery run rates, which have fallen faster than visible mobility data. Together, this indicates that China is likely drawing statistically invisible inventories of both crude and refined products to sustain demand. In other words, this is not true demand destruction but, rather, temporary supply relief in the same vein as the US and Japanese SPR releases, keeping the market looser than it otherwise would be right now.

This highlights a more structural and analytically discomforting reality: despite unprecedented visibility into global oil inventories and seaborne trade (thanks to the proliferation of alternative data vendors), large portions of China’s oil industry remain troublingly opaque. Today, this represents the largest blind spot to the market’s collective statistical model of the oil industry. And, more urgently, this leaves the market guessing as to when China’s aggressive SPR support will be exhausted or otherwise withdrawn, which would prompt a renewed surge in upward pricing pressure.

Let’s review the Chinese data that we do have—from imports through refining and on to end consumer behaviour—to get a better sense of whether this looks more like true demand destruction or mere temporary supply relief.

Import Implosion