Sanguine Strait Stoppage

Making sense of relatively low crude prices through nearly two months of the largest oil supply shock in history

If you’re already subscribed and/or like the free summary bullets, hitting the LIKE button is one of the best ways to support my research.

Despite broad expectations that crude prices would rocket higher, the market reaction remains shockingly sanguine—with prompt Brent futures prices, somehow, spending most of April below $100/bbl—in the face of the currently-dire geopolitical context.

The best explanation for the juxtaposition between headline shock and pricing is a combination of the (lack of) realized inventory declines as well as Presidential jawboning and the April 7th ceasefire.

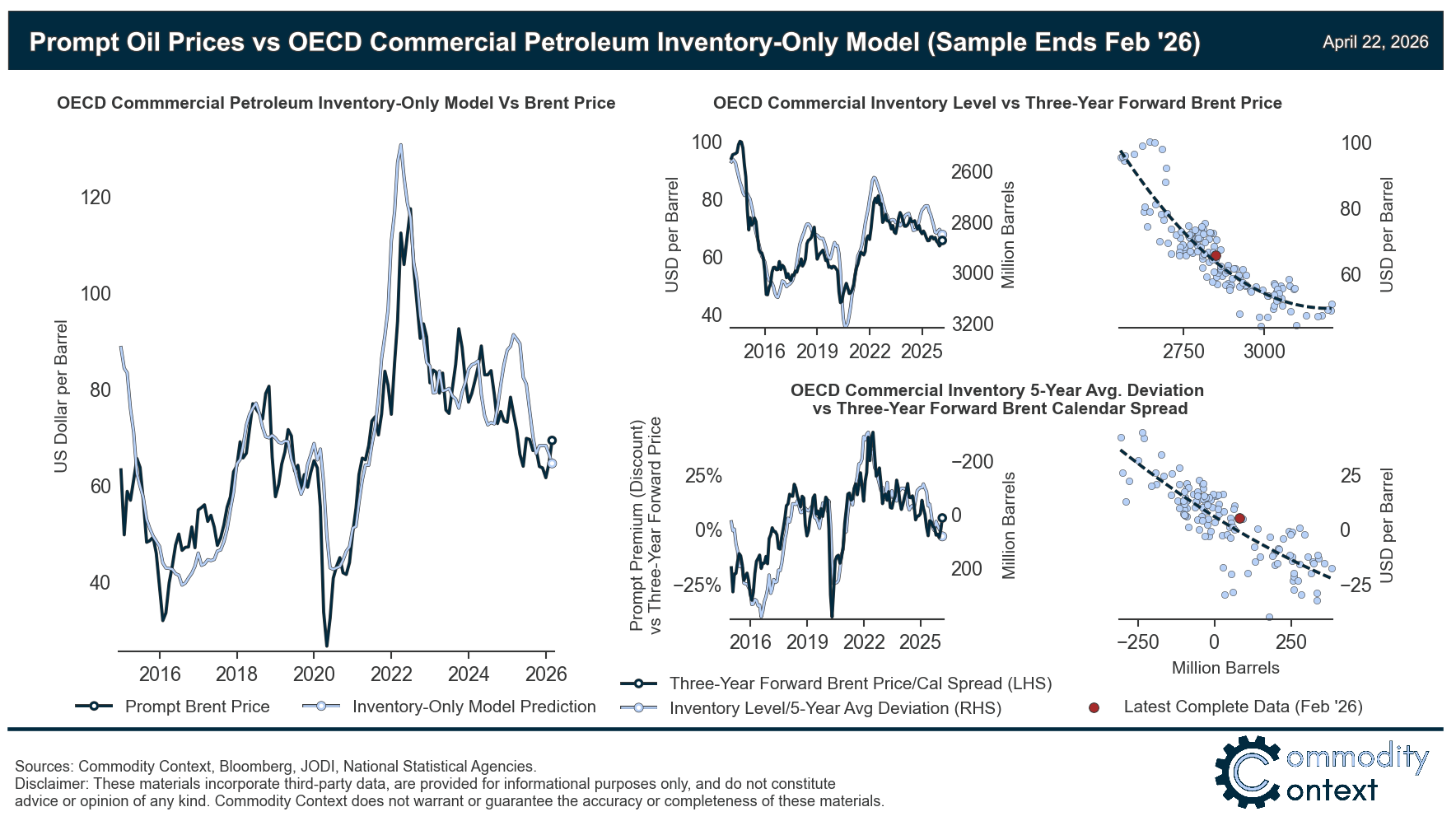

The impact to date of the Hormuz closure is most visible in term structure; while (still) elevated commercial inventories have provided a healthy buffer against upwards pressure on the curve, record backwardation in both physical and financial prices is placing a premium on prompt deliverable barrels as a signal to rapidly draw down those stocks.

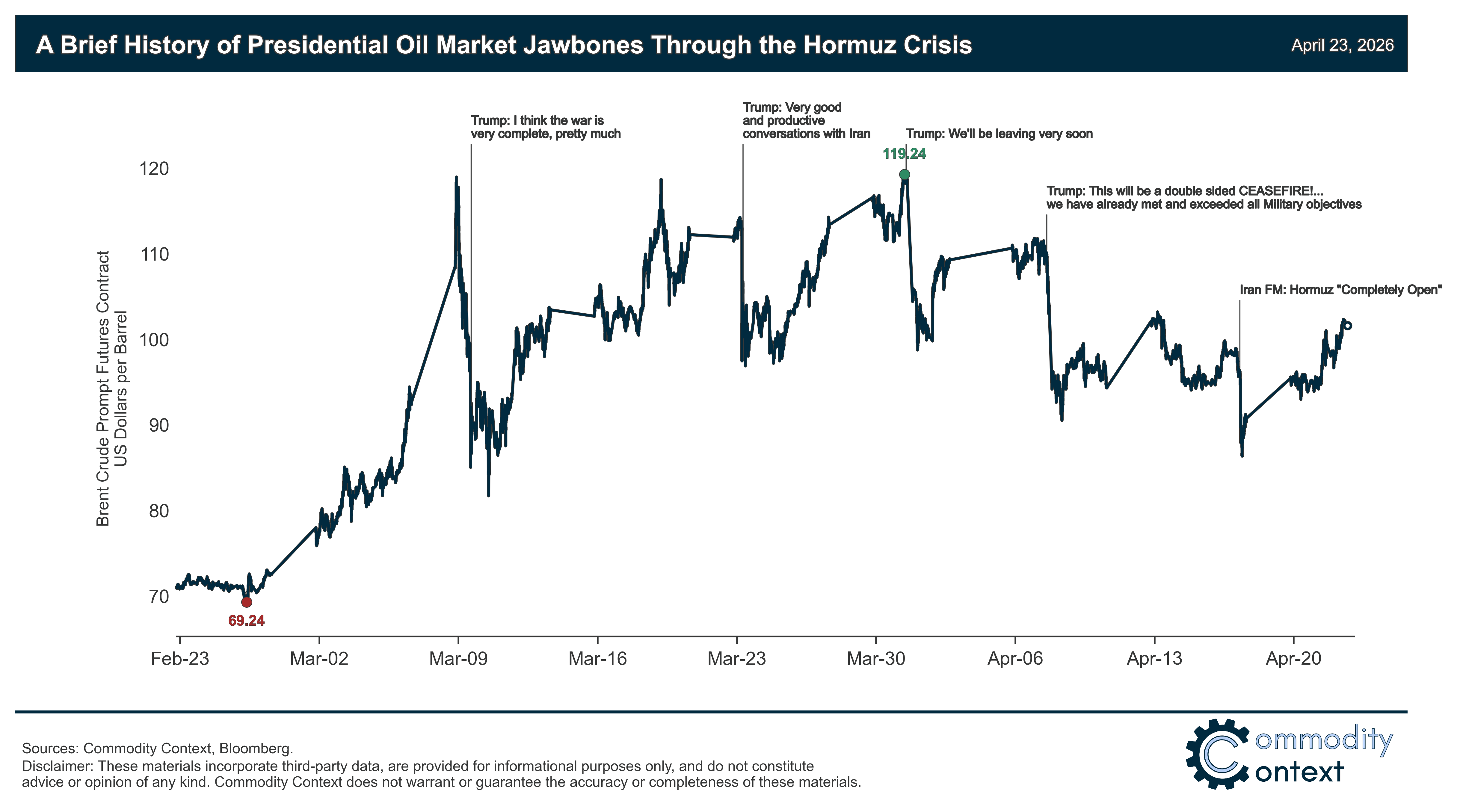

Frequent and strongly-worded verbal interventions by the White House have unnerved futures market participants; short-term downside is acute when another Trump post can, and will, sink the intraday price of crude by $10-15/bbl.

The largest pullback in prices occurred after the ceasefire announcement on April 7th; there is no doubt that the ceasefire has reduced, for now, the threat of extreme escalation, including more catastrophic damage to regional production infrastructure, but it has also thus far failed to end the conflict or reopen the Strait.

If the Strait of Hormuz remains closed for another two months, commercial inventories will be rapidly drawn down and historical relationships suggest we could see prompt Brent prices approach $200/bbl by the end of June.

The Strait of Hormuz has been closed for over seven weeks, shutting in a staggering 13 MMbpd of non-reroutable Gulf liquids production. The upstream shut-in has already accumulated more than a half billion barrels in unproduced output, en route to roughly a full billion barrels given lagged restart times even if the Strait was to fully reopen next week. Yet, the market reaction is shockingly sanguine in the currently dire geopolitical context. Despite many calls—including from yours truly—that crude prices would head sharply higher, prompt Brent futures have, somehow, remained below $100/bbl for most of April.

Perhaps, this juxtaposition—between headline shock and pricing—cuts to the heart of something that I’ve long argued: oil futures aren’t especially good at manifesting the market’s collective forward view. Under the glare of this lens, I, and many other oil analysts, may have violated my own cardinal rule: expecting the market to anticipate the inevitable supply losses stemming from the closure of the Strait. Through the lens of realized and visible inventory draws, there’s a reasonable argument that the initial price spike was a fear-induced overreaction to the Hormuz shock: not in scale, per se, but in timing.

Therefore, the best explanation for the pullback in crude pricing through April is the combination of (lack of) realized inventory declines as well as Presidential jawboning and the April 7th ceasefire. The world has stocks—both commercial and emergency—to buffer a temporary shock and, so, we’ve seen much of the pricing pressure manifest in the very front of the futures curve and into the physical market. Meanwhile, the White House’s desperate attempts to jawbone and talk down market reactions have distorted market sentiment. Most recently, the ceasefire materially shaved off some of the worst tail risks, including more direct attacks on regional production infrastructure, though has thus far failed to meaningfully reopen the Strait.

Nearsighted Curve