China Sputtering

The world’s perennial fastest-growing source of petroleum consumption is seeing demand contract once again following last year’s historic recovery, weighing on global demand forecasts.

If you’re already subscribed and/or appreciate the free summary, hitting the LIKE button is one of the best ways to support my ongoing research.

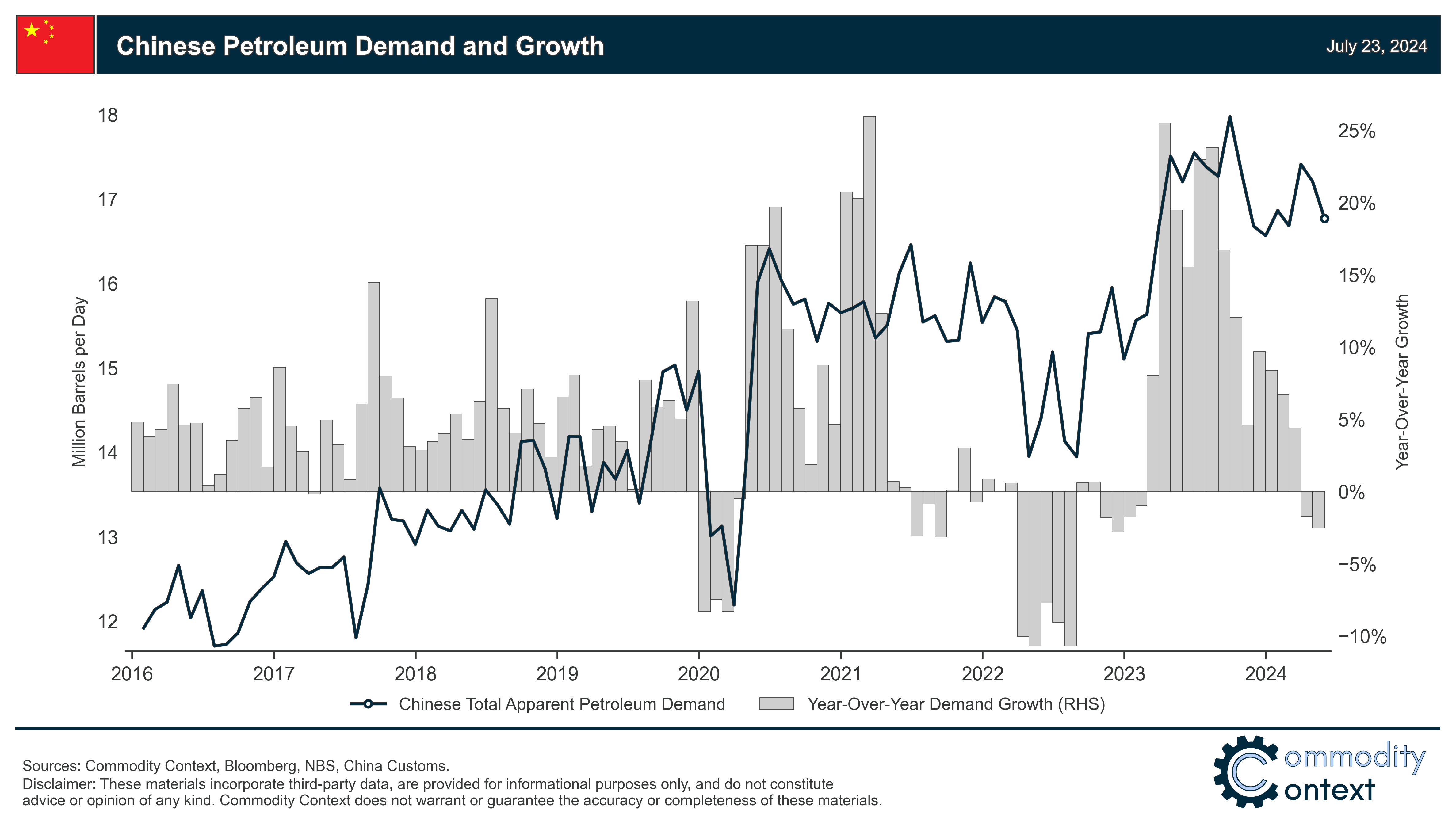

Apparent Chinese petroleum consumption is contracting, becoming a drag on global demand growth after last year’s unprecedented Chinese advance drove three-quarters of global gains.

Demand growth is slowing across all major petroleum products, but weakness is especially stark in industrial-linked fuels like diesel, which are suffering both from slower industrial activity as well as direct displacement by other fuels like LNG in the core heavy transportation sector.

A slower China is a big problem for global demand hopes this year, and Chinese consumption needs to reaccelerate in the second half of 2024 to hit consensus growth expectations, with the latest high frequency tracking data indicating that said reacceleration hasn’t yet materialized as of mid-July.

Chinese petroleum consumption growth has weakened materially through the first half of 2024. Apparent Chinese refined product demand actually contracted in both April and May compared to the same period last year, and higher frequency refining and tanker trade data indicates that consumption remained weak, and possibly fell even further, through June and into July.

Now, Chinese demand is by absolutely no measure low; last year’s unprecedentedly strong growth pushed overall Chinese consumption to extremely high levels. Even after easing back, Chinese consumers are still absorbing nearly 17 million barrels of petroleum products every day as of the latest data. But, base effects from last year’s historic growth boom make continued growth inherently difficult to sustain without some period of retrenchment (see China’s High Demand Bar). So, while there’s always a chance that demand recovers in the latter half of the year like we saw in 2023, we have yet to see evidence of this reacceleration and last year’s strong second-half growth creates an especially high hurdle to clear in 2024.

The challenge is that China’s incremental demand growth has slowed, reflecting worrisome headwinds from both flagging economic activity and alternative fuel penetration. That’s a big problem for global demand growth prospects this year and, by extension, OPEC+’s plans to ease a considerable volume of production cuts back into the market as outlined and modeled in OPEC’s Plan and Oil’s Next 18 Months. China is almost always the single largest source of global oil demand growth; so, it will be incredibly hard to reach, let alone surpass, the modest forecast of 1 MMbpd in global demand growth held by both the IEA and EIA—not to mention OPEC’s 2.25 MMbpd expectation—with China already flatlining mid-year.