China Oil Demand Doubts

Apparent Chinese oil consumption data is unrealistically high, likely driven by strategic stock building, and may present headwinds to global liquids demand as those builds normalize.

If you’re already subscribed and/or appreciate the free charts and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

There’s a fundamental incongruence between staggeringly strong apparent Chinese oil demand and all indications of lackluster broader economic conditions in China.

This isn’t to say that demand is weak; but, perhaps what we’re really seeing, at least in part, is a strategic stockpiling—and this creates the risk of a sudden pullback if said activity ends before real domestic demand has caught up.

There continues to be high hopes for China’s 2023 recovery from the ultra-depressed COVID-zero levels of 2022, and there remains a [less likely] chance that it’s actually current Chinese economic activity that is being underestimated.

Despite our best efforts, the opacity of Chinese data makes confirming current oil demand tremendously difficult and leaves plenty of room for honest disagreement, which only increases the likelihood of volatile price moves as the evidence shifts between narrative camps.

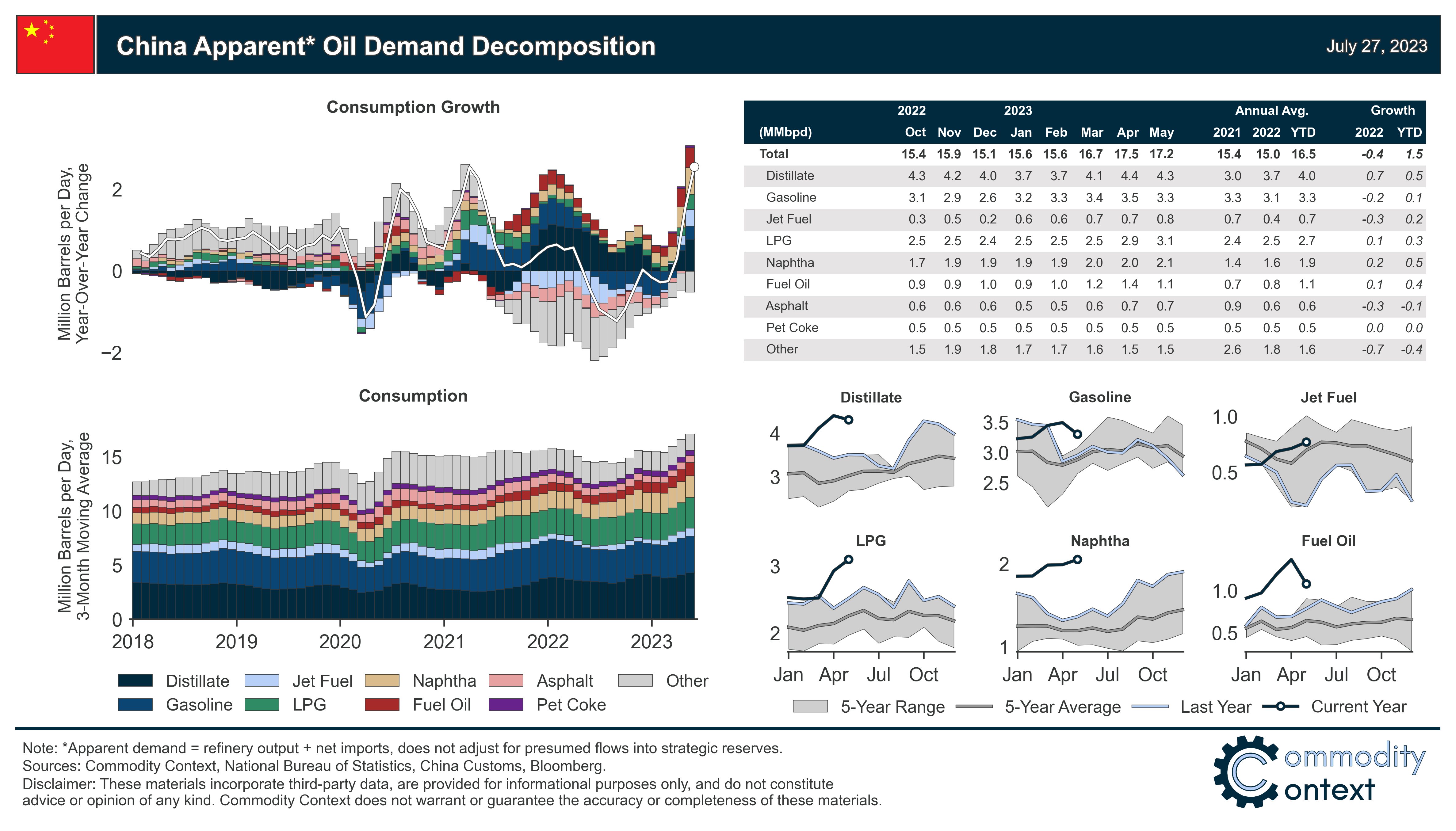

There’s something weird about Chinese oil demand data. “Chinese Oil Demand Doesn’t Make Sense,” reads a July 14th Wall Street Journal headline and I completely agree—in my view, this has been an issue for months, if not years, and, now, is seemingly getting worse. The crux of the problem is a fundamental incongruence between staggeringly strong apparent Chinese oil demand and all indications of lackluster broader economic conditions.

This is not simply a matter of pedantics; the question of Chinese oil demand is deeply consequential given the role of China as the world’s second-largest oil consumer and largest source, by-far, of incremental demand growth. Indeed, the apparent gangbusters petroleum product demand strength is a big part of why my global balance estimates have been tipping into steeper undersupply over the past couple of months (see my July Global Oil Data Deck).

The simplest explanation is that much of that recent Chinese apparent demand isn’t true consumption at all; but rather, Beijing-directed strategic inventory accumulation. If true, this would be a pretty dramatic accumulation, at least judging by recent apparent demand prints. April and May were the first two monthly prints above 17 MMbpd, which is an average of 3.2 MMbpd higher compared to the corresponding, albeit depressed COVID-zero, months last year.

Now, this isn’t to say that Chinese oil demand is terrible; but, it would be bizarre to see record-setting domestic consumption amidst a far more tepid overall Chinese economy. In contrast, the implications of a strategic stock-building thesis are reasonably bearish, relatively speaking: apparent demand could contract quickly in the face of higher prices or, worse, inventories could be released back to the market, switching in an instant from a demand-force to a supply-force.