Venezuela’s Temporary Turnaround

While an important diplomatic inflection, recent sanctions easing lifts only the latest weight from around the neck of Venezuela's oil industry long hobbled by chronic underinvestment & mismanagement.

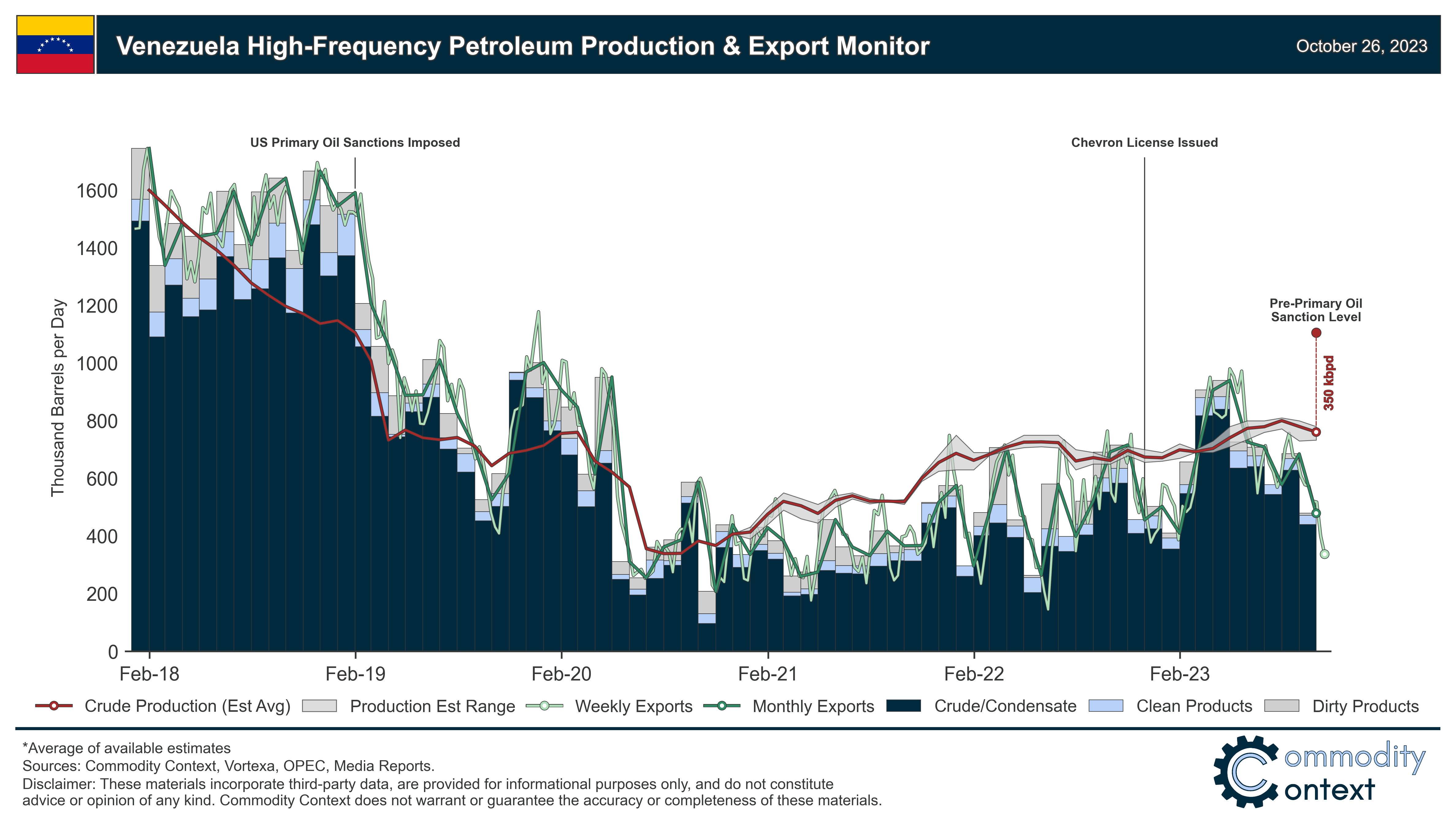

Given the lack of much transparent Venezuelan oil trade data, this pieces makes heavy use of tanker tracking data courtesy of Vortexa [affiliate link connects you directly to a Vortexa representative].

If you’re already subscribed and/or appreciate the free summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Oil-targeted US sanctions have been temporarily eased by the Biden Administration in exchange for electoral concessions from Venezuela’s Maduro government; both the efficacy of these negotiations and the long-term trajectory of US sanctions remain to be seen as we approach next year’s scheduled presidential elections.

The conditional sanctions relief is set to drive modest production and export increases (200-300 kbpd over the coming year) back to just shy of production levels seen before primary sanctions were imposed in early 2019, though chronic underinvestment and mismanagement in Venezuela’s oil and gas sector will cap any material upside until significant volumes of investment capital can be attracted back.

Any notable near-term impact will be in regional crude grade differentials where, net-net, a freer Venezuelan oil trade is negative for the relative value of heavy crudes in the Western hemisphere; Canadian crude differentials around the US Gulf Coast, for example, could be further hit after already falling from their July high-water mark.

After years of oil-targeted US sanctions, the Biden administration has announced an agreement with the Venezuelan government that includes a temporary easing of oil sector restrictions in exchange for a number of concessions related to next year’s Venezuelan presidential election.

Venezuela boasts the world's largest proven oil reserves and yet its industry is a basketcase—and I say that charitably. Decades of underinvestment, corruption, and mismanagement have rendered the country’s productive capacity a mere shadow of its former self. The combination of the collapse in production and the imposition of US sanctions in 2019 has driven petroleum exports to as low as 200 kbpd for a stretch into mid-2021, from 1.5 MMbpd as recently as 2018. Even as production recovered, modestly, from those COVID-depths, sanctions have remained a heavy weight around the neck of Venezuela’s industry—complicating and immensely reducing the pool of available customers, financing, and supply chain sourcing.

Given the dilapidated state of Venezuela’s remaining oil infrastructure, near-term production upside from this policy shift is likely capped at around 200-300 kbpd above September output; but, this diplomatic overture represents a potential turning point in what had been ever-tighter sanctions against the Venezuelan economy and—in the off chance that momentum is maintained—could unlock considerable heavy oil resources for future development.