Pipeline from Perdition

The start-up of the Trans Mountain Expansion (TMX) pipeline staves off yet another Western Canadian crude egress crisis and diversifies export optionality

If you’re already subscribed and/or appreciate the free summary, hitting the LIKE button is one of the best ways to support my ongoing research.

The start-up of the much-delayed and wildly over-budget Trans Mountain Expansion Project staves off yet another Western Canadian egress crisis and triples Western Canada’s access to global crude markets via tidewater.

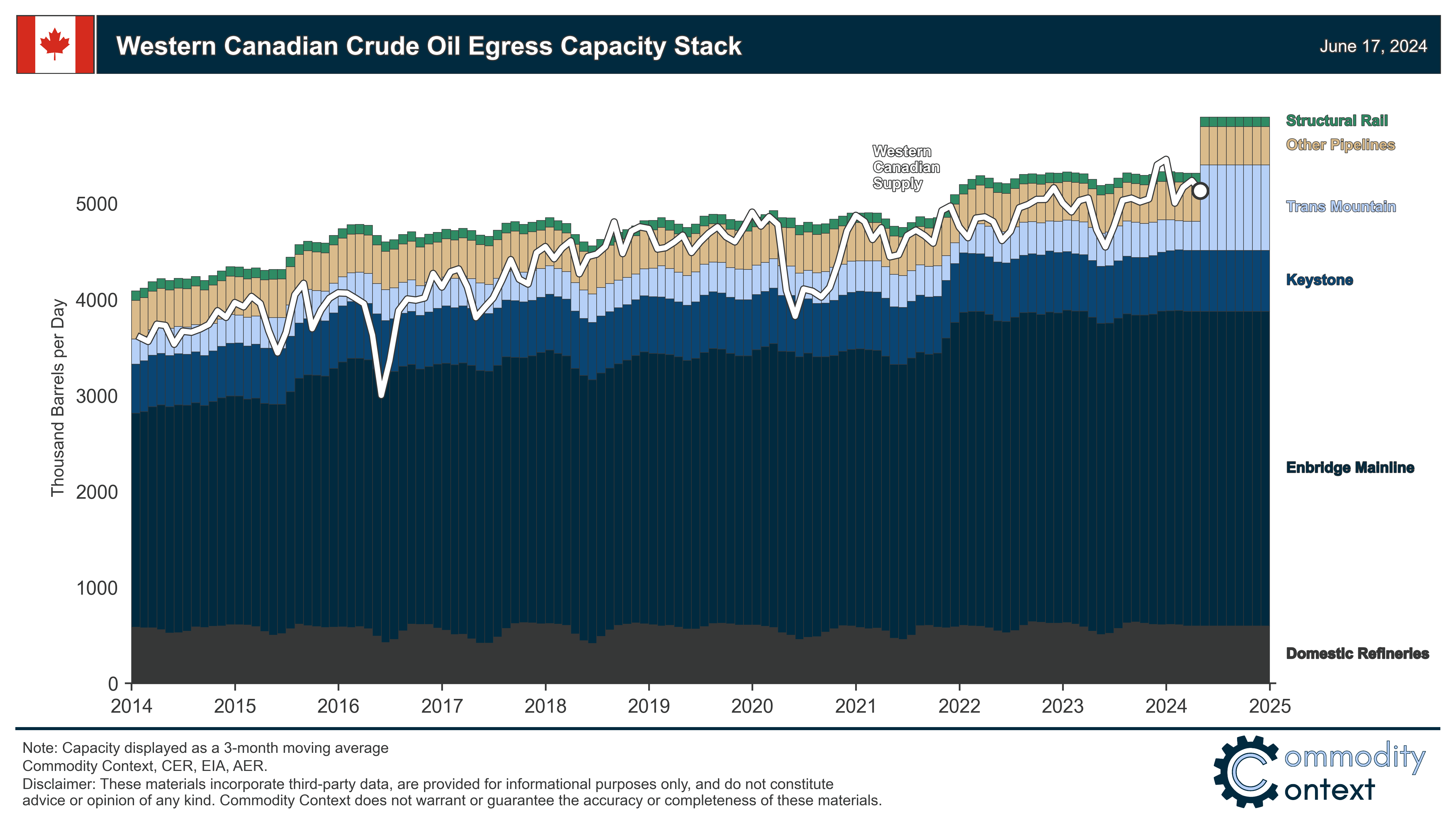

Western Canadian oil producers rely on just a handful of pipelines to get their crude to end-consumers—mostly, just three large pipelines: the Enbridge Mainline, newly-expanded Trans Mountain System, and Keystone.

Trans Mountain was, until very recently, the smallest of the core large pipelines, now upgraded to 890 kbpd from only around 300 kbpd, and is remarkable not only because of the novelty of new pipeline development after years of project drought but also because TMX holds great potential to diversify Canadian exports.

The start-up of the Trans Mountain Expansion pipeline (TMX) has staved off an other egress capacity crisis for Western Canadian oil producers, tripling Western Canada’s access to tidewater and, more broadly, kicking off the necessary process of rerouting some barrels west that were previously heading south of the border. Canada produces roughly three times more crude oil and equivalents than Canadian refineries can process domestically. Most of that is produced in the Western Canadian Sedimentary Basin (WCSB), the vast geologic region spreading from northeastern British Columbia, through Alberta, and into western Saskatchewan, which is blessed with some of the largest reserves of crude oil and natural gas in the world.

But, in a cruel twist of fate, this hydrocarbon bounty is located huge distances from end consumers in any direction, with the Rocky Mountains standing between Western Canadian producers and the tidewater that would grant them proper access to global crude oil markets. Canada is an anomaly in that almost all crude leaves the country by pipeline, rather than by tanker, and is purchased by just one importer—the US. For most other world-leading production regions, barrels are exported on tankers to be sold on the global seaborne market and sales are diversified across a wide array of seaborne importers that make decisions based on constantly-changing sets of economic incentives.

Unfortunately, Western Canadian pipeline capacity has frequently fallen short of the demand for takeaway as a result of steady WCSB production growth, with devastating consequences for the value of Canadian crude production. Even when it is sufficient, come rain or shine, good times or bad, Canadian barrels head south along a fixed set of pipelines to a consistent set of US regions, states, and even individual refineries, which creates its own set of risks. So, let’s take a moment to better appreciate how the newly minted TMX affects the outlook for Canadian crude prices and the directional balance of how Canadian crude gets to market—and which markets it gets to.

Vast, Concentrated, and Frequently Insufficient