OPEC+ Data Deck (March 2026)

Where the producer group stood heading into the most severe supply crisis in its history, as well as early estimates regarding where the core of OPEC's Gulf production base currently stands today.

OPEC+ is currently experiencing the most severe supply crisis in the producer group’s history, which began just more than two weeks ago. As such, the February operational performance statistics explored in detail in the attached Data Deck below are no longer immediately relevant to the market, but I wanted to keep the normal pace of monthly data publications running because this report will be truly eye-popping next month when March numbers roll in.

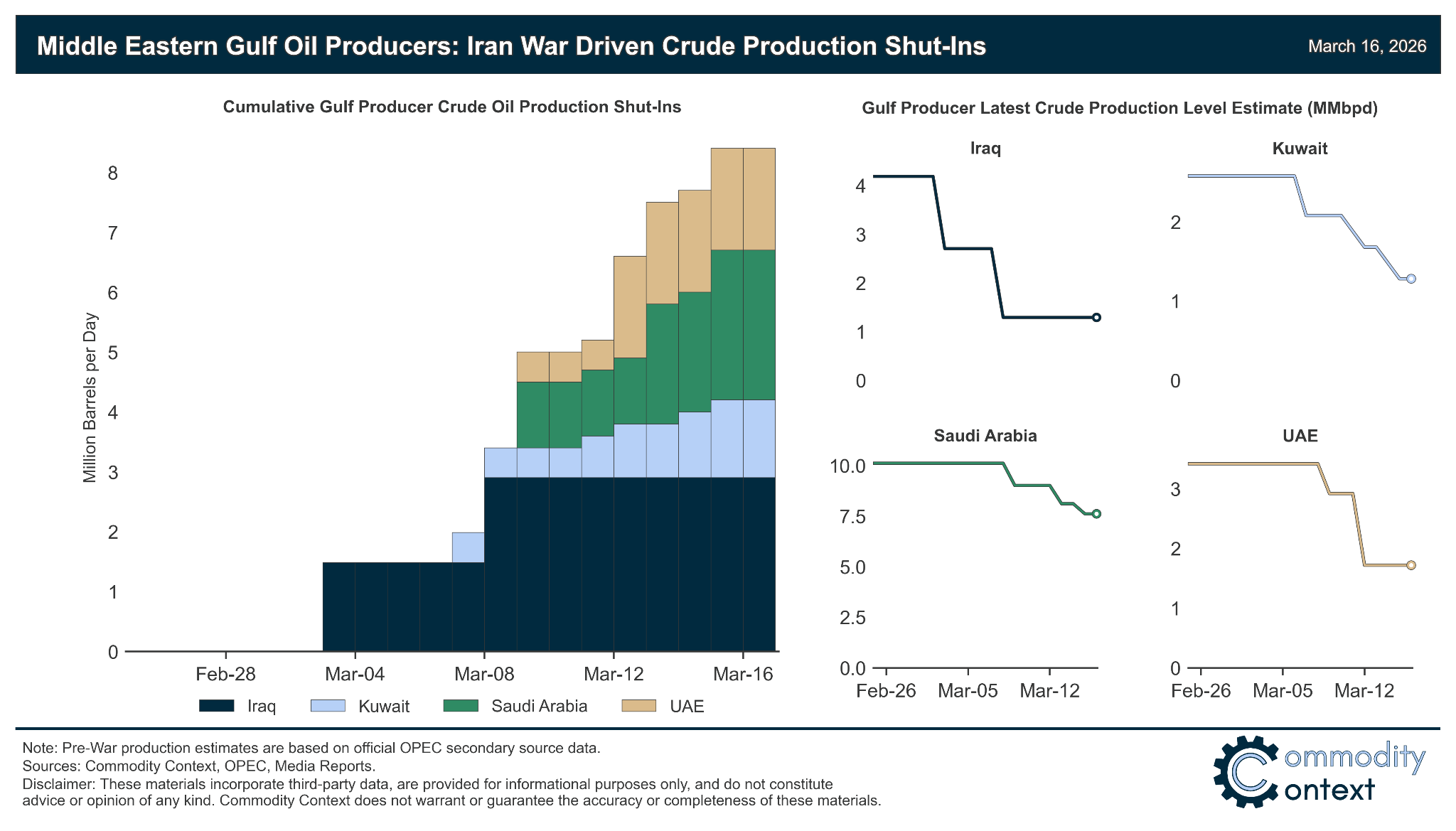

You will also find early running estimates of current Gulf producer crude output cuts and shut-ins below as a running tally of the damage already wrought by the Hormuz stoppage.

Below the paywall you will find the latest monthly edition of the Commodity Context OPEC+ Data Deck (50-page PDF), tracking groupwide and member-level official production estimates, quotas, compliance, exports, and official production data reconciliation vs output implied by visible movements.

If you’re already subscribed and/or like the free summary bullets, hitting the LIKE button is one of the best ways to support my research.

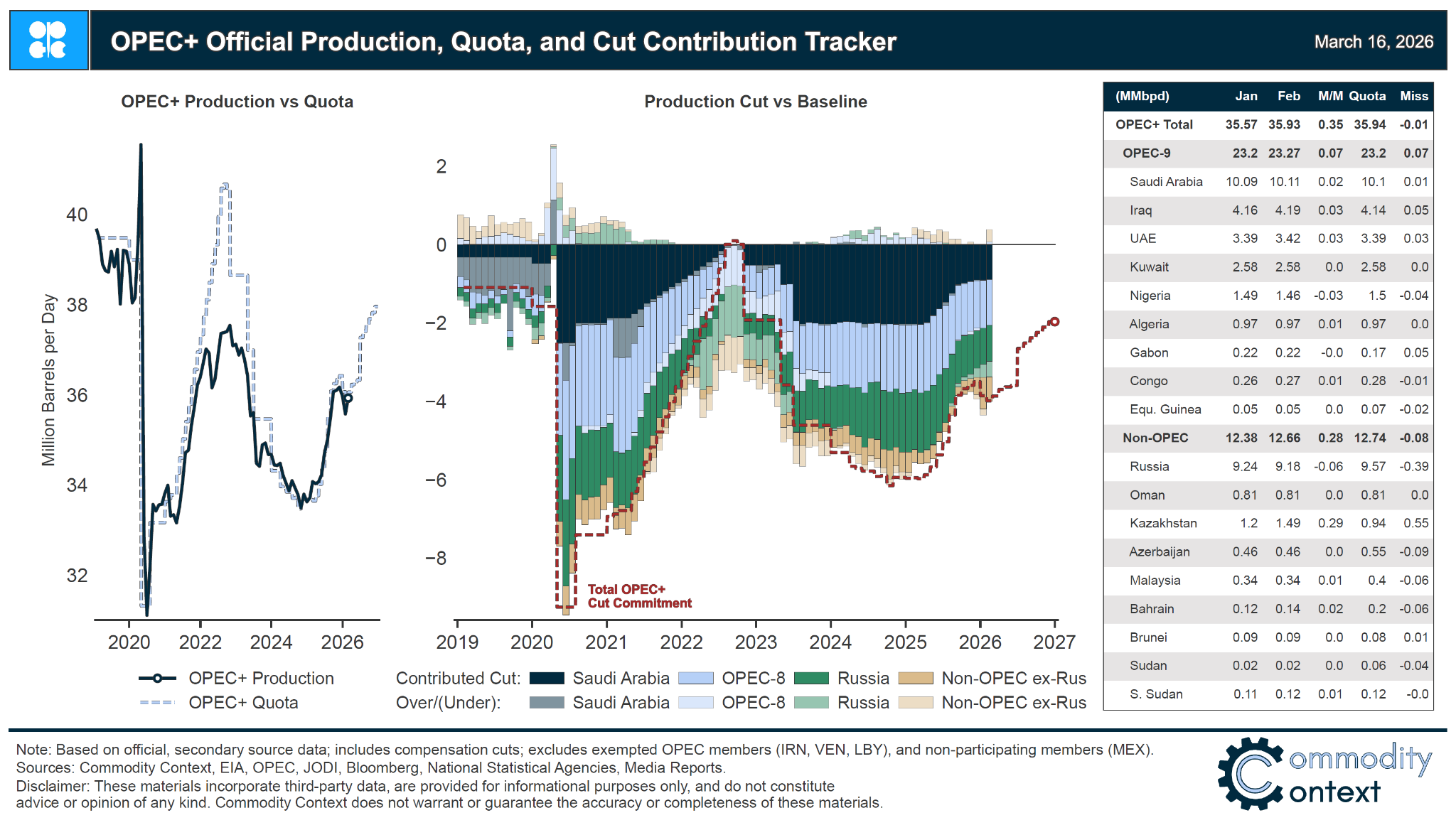

Quota-participating OPEC+ crude production rose +354 kbpd m/m to 35,928 kbpd in February, immediately before the onset of the Iran War, according to official OPEC+ secondary source aggregate statistics, mostly driven by the ongoing rebound in beleaguered Kazakh output.

Crude production shut-ins across the Gulf have risen to roughly 8.5 MMbpd as of latest count, based on ongoing industry reports. Iraqi production has been hit hardest, down more than two-thirds with most of the production in the Southern Basra fields currently offline. Kuwaiti and Emirati production is currently sitting around 50% of pre-war levels, contributing 1.3 and 1.7 MMbpd of confirmed shut-ins each, with all of the UAE’s offshore production now reportedly shut-in. Finally, Saudi Arabian production, which is most sheltered from the Hormuz stoppage thanks to the East-West pipeline offset, is believed to have reduced upstream production by 20-25%.

[Full PDF Deck and additional analysis below paywall]