Oil Context Weekly (W36)

Worst week for oil since last October rattles industry nerves as prices fall to lowest level since late-2021, with crude falling in lockstep with broader risk assets & driven by outsized spec selling

Happy(ish) Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

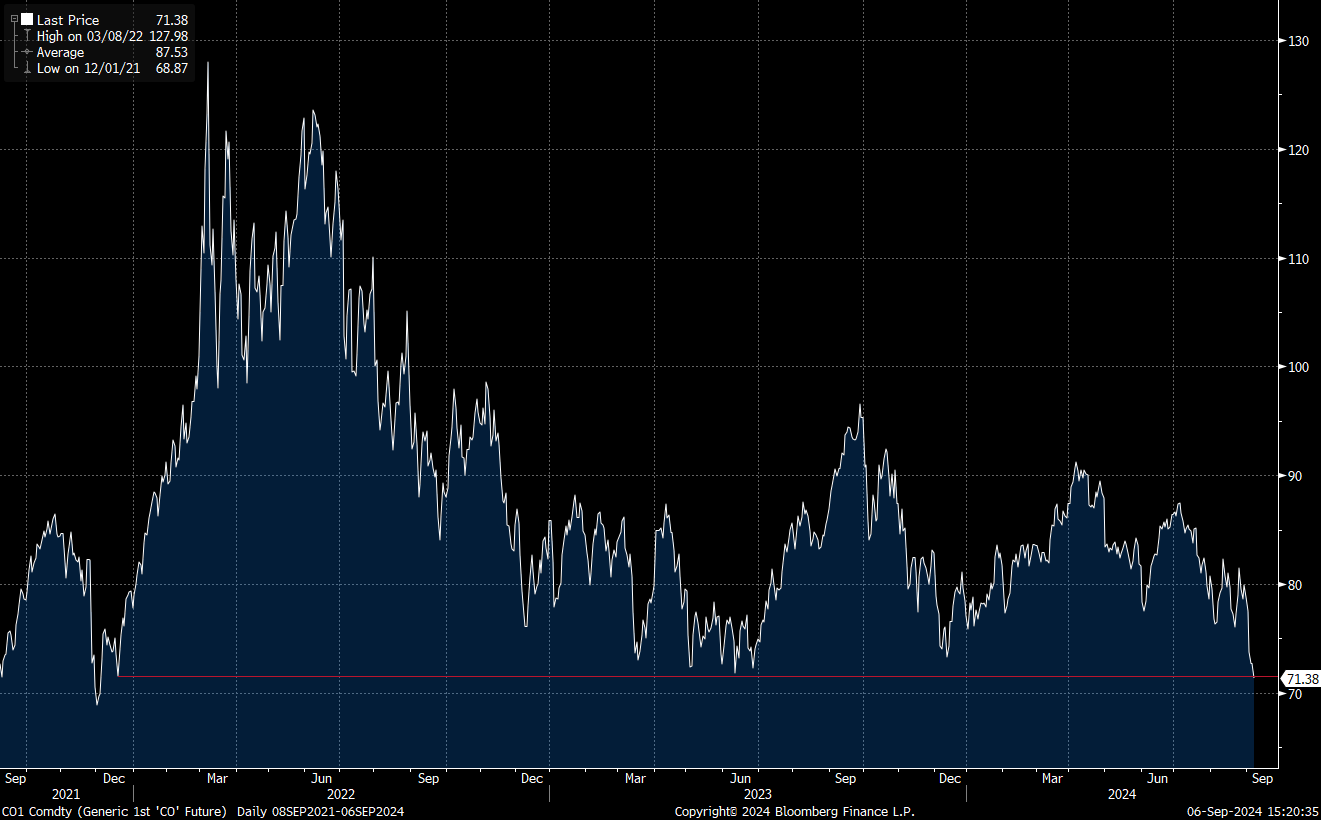

Flat Prices collapsed, falling more than $7/bbl for the worst weekly performance in 9 months and closing at the lowest level since December 2021, before the Russian invasion of Ukraine and the start of the COVID-era bull market in crude oil.

Timespreads eased off this week but remained far firmer than battered flat prices; prompt futures spreads are still modestly backwardated, and while DFLs have fallen to near-contango levels they’re still stronger than the outright contango realized in May and year-end 2023, moments at which flat crude prices remained $5+ higher than they stand today.

Inventories data was mixed but leaned bullish, with a large US crude draw—now drawing faster than the seasonal norm—overwhelming a modest headline products build in Singapore.

Refined Products continue to show weakness, with both gasoline and crack spreads falling another $1.50-2.00/bbl this week, adding further weight to the macroeconomic storm clouds darkening the entire oil complex; however, rising supplies from new refineries are driving at least some of that weakness.

Positioning data revealed that speculators were once again massive sellers of crude contracts to the tune of 100 MMbbl (net), bringing their net position to excruciatingly low levels—below both December 2023 and June 2024, and the lowest net position since the early days of the COVID shock in 2020; it remains extremely unlikely that positioning normalizes here and indeed is still expected to turn to acute buying pressure as these shorts are inevitably covered and spec length is rebuilt.

As Well As OPEC+ delays scheduled production increases by two months, the overfitting of current price weakness to months-old Chinese demand weakness, and the ongoing loss of Libyan supplies.

What Happened This Week