Oil & Iran War Context Weekly (W23)

Crude prices rose through Wednesday before pulling back to end the week only modestly higher; all’s quiet on the US-Iran negotiation front, and all eyes on China’s plunging crude imports.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

I had the opportunity to rejoin Erik Townsend on the MacroVoices podcast for another update on how I’m thinking about the Iran War and the Hormuz oil shock—and why prices aren’t higher! (audio, 46:30-forward). I also joined Agelica Oung on the Taipology podcast to talk about China’s role in the crisis response so far (and lots more on that in this week’s writeup below). I spoke with the Financial Post to talk about the 1.5 billion Middle Eastern barrels we can already count as lost so far in the crisis.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

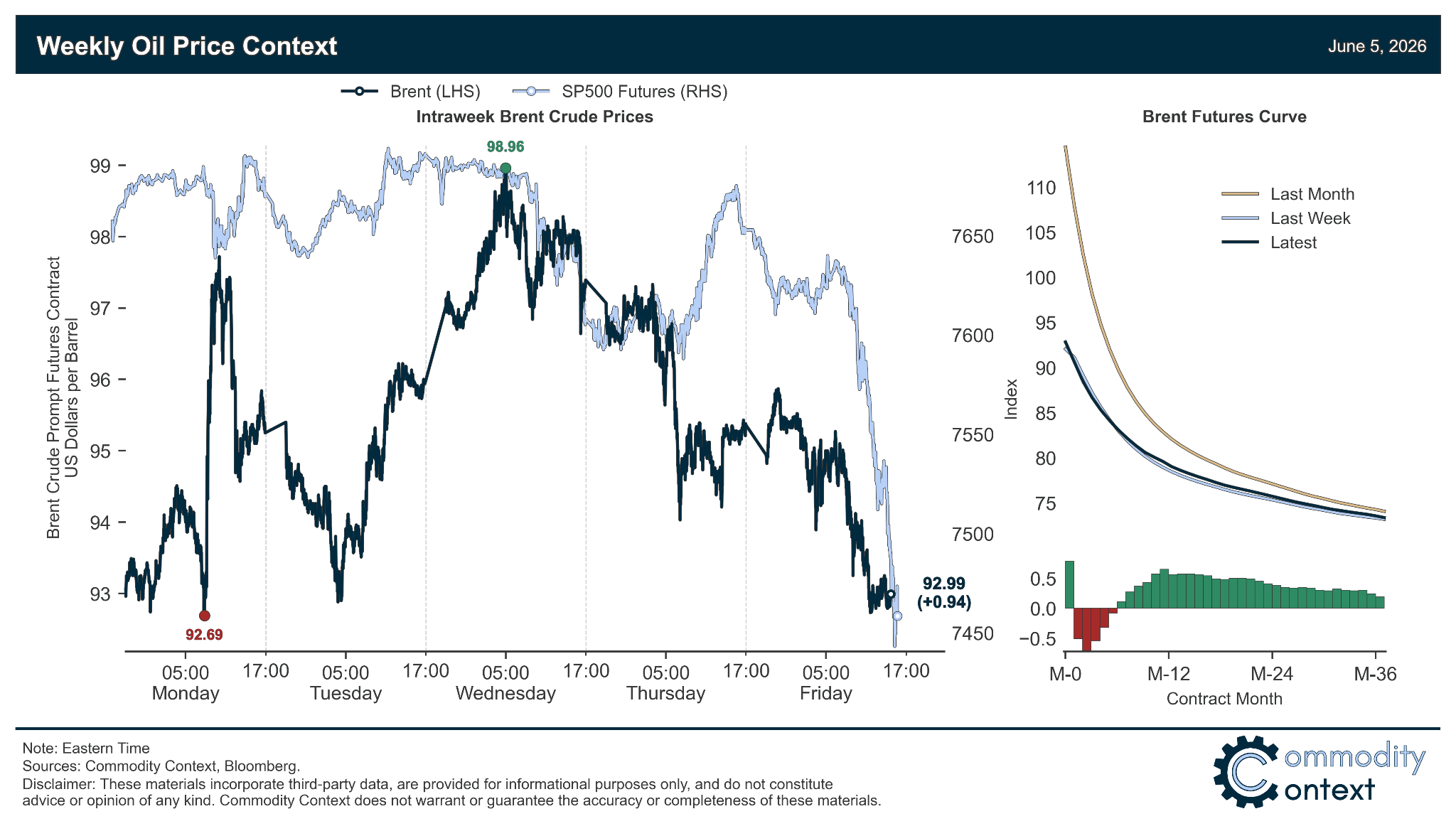

Summary

Flat Prices rose through Wednesday before easing back, ending ~$1/bbl higher as the market remains in a perilous limbo, awaiting any sign of progress in negotiations between Washington and Tehran.

Timespreads restrengthened from last week’s end-of-month swoon as all major crude benchmarks are holding $2-3/bbl in prompt backwardation; that’s substantially weaker backwardation than we saw at the heights of late-March/early-April but still represents extreme tightness.

Inventories data mixed but, again, leaned bullish on the back of a collapse in Singaporean inventories; US total crude inventory draws hit a whopping -18 MMbbl, split equally between commercial and strategic stocks, and the mild bounceback in US gasoline stocks capped the largest (and tied for longest) stretch of consecutive gasoline draws on record.

Refined Products markets remain tight and choppy; both gasoline and diesel crack spreads were roughly flat ($35/bbl and $60/bbl, respectively), though gasoline, in particular, finally caught some breathing room

Market Positioning data confirmed that speculators were once again net sellers of crude futures and options contracts over the past week-through-Tuesday, driven largely by a continued buildup in gross short positions. The leaking of this speculative length is gradually removing a key downside risk for crude prices while at the same time beginning to build up the dry powder that will provide explosive upside to the next rally should inventories continue to drain and fundamentals retighten anew.

As Well As China China China (all I can think about is China), Iran wants its pallets of cash, Trump envoys begin technical nuclear consultations with US national lab, and yet another new UAE pipeline plan.