Oil Context Weekly (W48)

Crude prices gained slightly on the week but ended the month lower, and Ottawa and Alberta finally signed the “Grand Bargain” MOU on which the Canadian oil and gas industry has been waiting.

🦃 Happy Thanksgiving to our American subscribers and happy Friday to all oil watchers,

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

This week’s OCW report includes a lengthy overview of my initial impressions of the Canada-Alberta MOU, which conditionally approved a major (1+ MMbpd) oil pipeline to Canada’s west coast.

Source: The Hub

🎙️ I also shared some of my immediate thoughts on this MOU alongside former Alberta Deputy Energy Minister Grant Sprague last night on The Hub’s Alberta Edge podcast (and the YouTube video), which I encourage you to check out. Come for the frenetic hand-talking, stay for the nuanced insights on yesterday’s Canada-Alberta MOU and what it really means for the future of Western Canada oil pipeline capacity.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

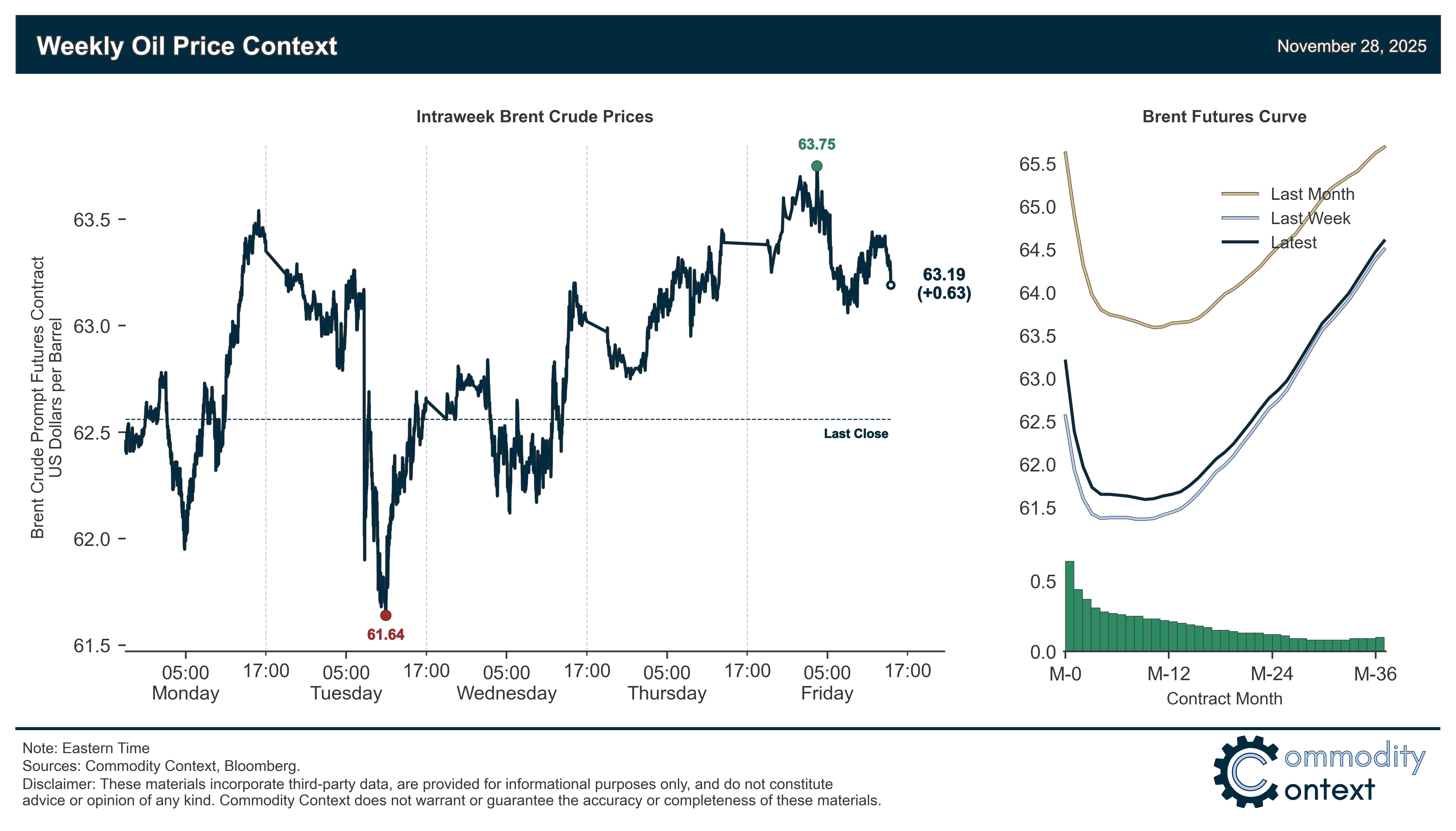

Flat Prices rose just more than 50c/bbl for Brent to finish the week a hair above $63/bbl, down ~$2/bbl from the start of the month. Reports earlier this week that Ukraine was poised to accept the US-proposed peace plan precipitated a ~$2/bbl crude price rout on Tuesday, though contracts spent the rest of the week clawing back those losses to end the week back in the green as hopes of a near-term resolution again faded.

Timespreads remained largely unchanged, save a bit of a pre-expiration crunch through the Brent complex; prompt WTI and Dubai (as well as Brent’s 2nd-3rd month spread) each traded sideways, bouncing around a ~10c/bbl rangebound channel.

Inventories data were mixed between notable draws in Singapore and ARA Europe and a seasonally abnormal headline build in the US; overall, middle distillate stocks remain under clear pressure, even after the rollover of the acute market tightness seen earlier this month.

Refined Products continued to fall back to earth from the exceptionally high levels reached over the past few weeks; but, while well below recent highs, both diesel and gasoline cracks are sitting 50% or more above seasonal levels.

Market Positioning data confirmed that speculators were large net sellers of Brent crude contracts, bringing Brent specific positioning back into oversold territory and, thus, tilting price risk to the upside; indeed, the large w/w decline in Brent spec positioning only prompted a ~$2/bbl decline in pricing, which is relatively modest and can be read as a signal of crude’s current underlying market health.

As Well As OPEC+ expected to hold output steady and potentially agree to new capacity estimation mechanism, two Russian dark fleet tankers struck in Black Sea, and Ottawa and Alberta signed a pipeline and regulatory MOU (longer read).