Oil Context Weekly (W47)

Crude prices eased on broader market pullback and concerns that US-proposed Ukraine peace deal removes key remaining bullish market support; diesel margins hit eye-watering levels before rolling over

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

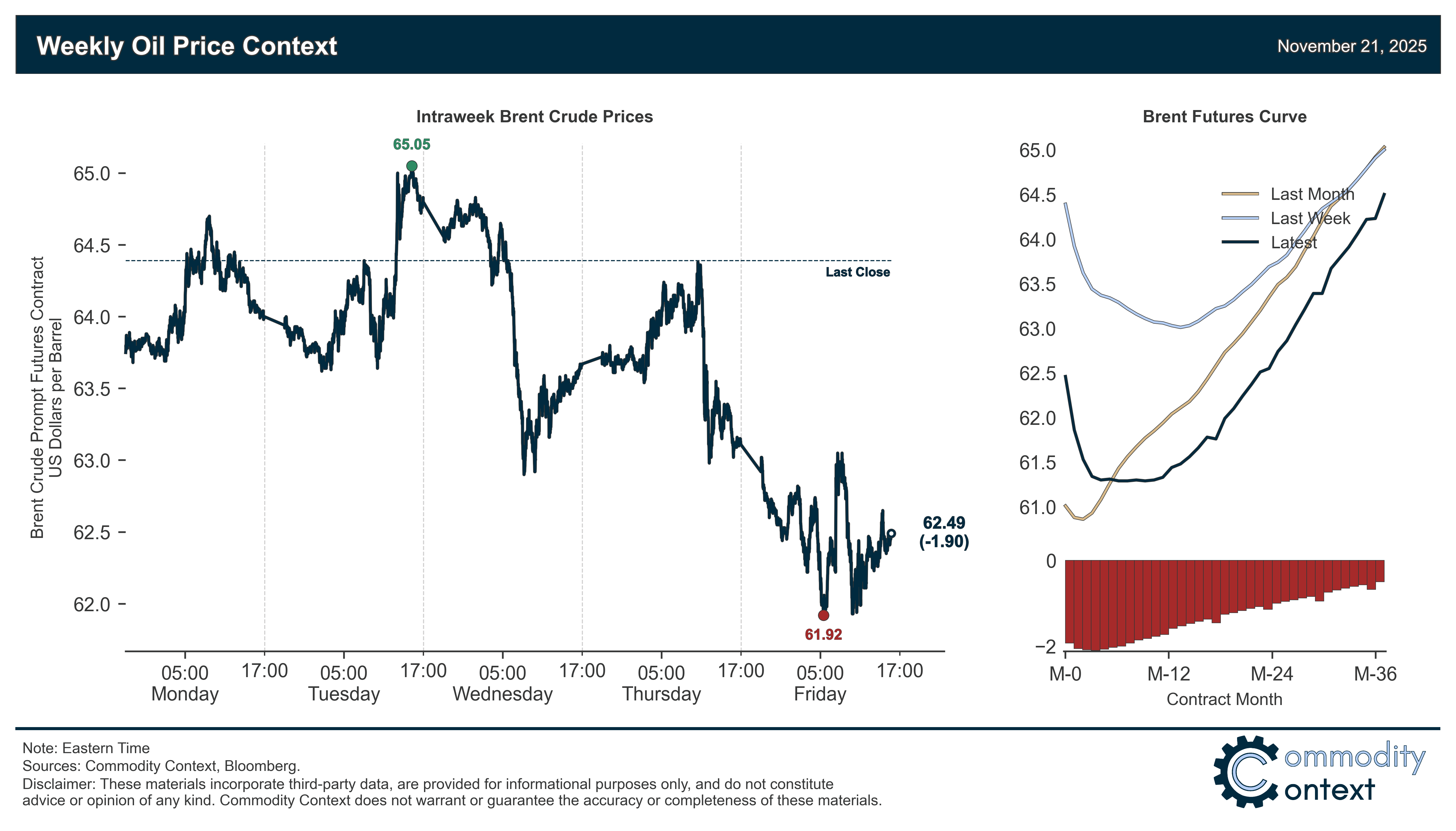

Summary

Flat Prices fell ~$2/bbl for Brent crude to finish just above $62/bbl, weighed down by a combination of broader AI-worry driven risk asset weakness and the oil-specific concerns over the US-proposed Russia-Ukraine peace deal, which would remove one of the last bullish market supports.

Timespreads strengthened further at the front of the curve, with Brent prompt spreads rising above 60c since late-October, and both WTI and Dubai prompt spreads rising to a lesser degree; however, the Brent crude futures curve remains almost exactly where it stood at this time last month, only with the front of the curve slightly more backwardated and the belly of the curve in steeper contango.

Inventories data were mixed between Stateside draws, a build in Singapore, and effectively flat stocks in ARA Europe; overall, US petroleum stocks remain notably low despite concerns of mounting surplus supplies, while inventories are generally higher across both Europe and Singapore.

Refined Products margins for key road fuels like diesel and gasoline have finally rolled over, down sharply from their truly astronomical levels reached earlier this week but still exceptionally rich as refined product markets remain tight.

Market Positioning data confirmed that speculators were net buyers of both Brent crude and ICE gasoil contracts, with Brent positioning risk more or less balanced and gasoil positioning risk reaching frothy levels; the end of the US federal government shutdown has allowed the CFTC to begin trickling out CoT data once again, but the releases won’t catch up to current market realities until the end of January 2026.

As Well As US-proposed Russia-Ukraine peace deal could remove one of last remaining bullish oil market supports, Novorossiysk back online much faster than feared, US sanctions on Rosneft and Lukoil enter force, and more details on the Trans Mountain Pipeline’s optimization.