Oil Context Weekly (W29)

Hormuz flows and Gulf loadings have definitively rolled over amidst mounting attacks while the oil complex rerated sharply higher across flat crude prices, term structure, and refined product cracks.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

🎙️ On the latest episode of Oil Ground Up podcast (spotify), I was joined by the one and only Jeff Currie for a wide ranging conversation about the theory and reality of crude price discovery running into the shock case study of the Hormuz Crisis. Another special aspect of this conversation with Jeff is that we’re evolving and this is the first time we’ve published the video of our conversation.

For more public oil market context, check out my comments to Bloomberg (print) and Al Jazeera (print), as well as my conversations with the Competent Investor podcast (video) and the Palisades Gold Radio podcast (video).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

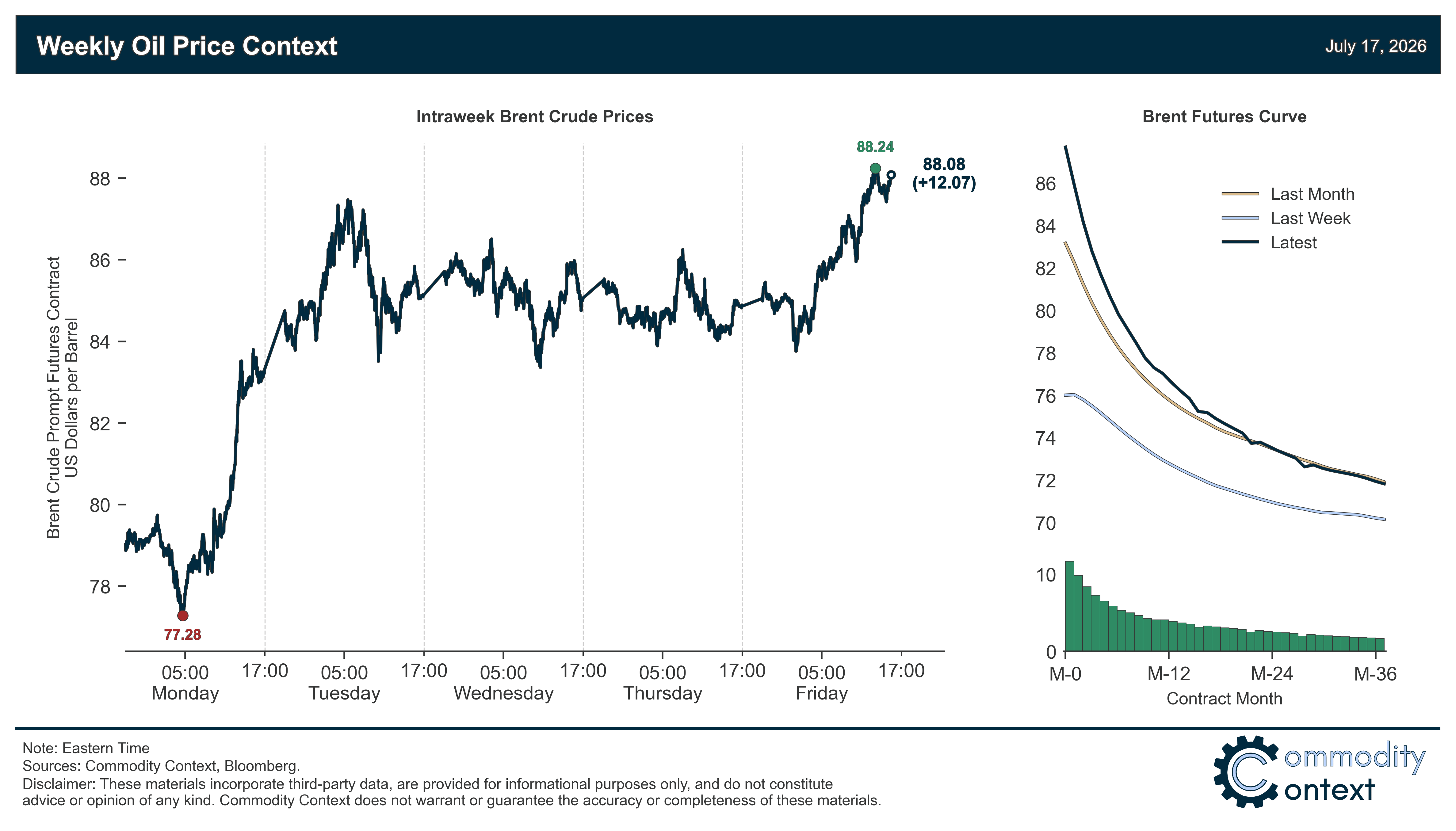

Flat Prices rose more than $12/bbl—the largest weekly gain since mid-April—as Brent settled around $88/bbl on the back of (1) sharply-elevated Middle Eastern supply risks, (2) the renewed collapse of Hormuz transits, and (3) the prospect of an even longer disruption to the world’s most prolific oil supply line; prices have now fully round-tripped the post-MOU selloff.

Timespreads ripped from minor prompt Brent crude contango last Friday to backwardation of nearly $2.50/bbl on Tuesday, ending the week around $1.80/bbl; other crude benchmarks joined the steepening (to a lesser extent), with WTI and Dubai prompt spreads sporting prompt backwardation of $0.50–0.75/bbl.

Inventories data came in particularly bearish, dominated by the largest headline build in US commercial stocks since last September—though the bulk of the US headline build was NGL inflows; ARA Europe also flipped to builds while Singapore saw draws moderate.

Refined Products felt the mounting supply concern, with diesel crack spreads hitting fresh crisis highs of more than $85/bbl and gasoline cracks rising back to retouch crisis highs above $55/bbl.

Market Positioning data revealed that speculators were massive net buyers but, even with this upswell, positioning risk still remains firmly to the upside between still extremely high short interest and only middling gross length.

As Well As a rundown of this week’s flurry of back-and-forth strikes in the Middle East, the impacts to Hormuz flows, the potential for escalation through the weekend, and a more-serious readying of a Houthi intervention in the Bab el Mandeb Strait.