Oil Context Weekly (W28)

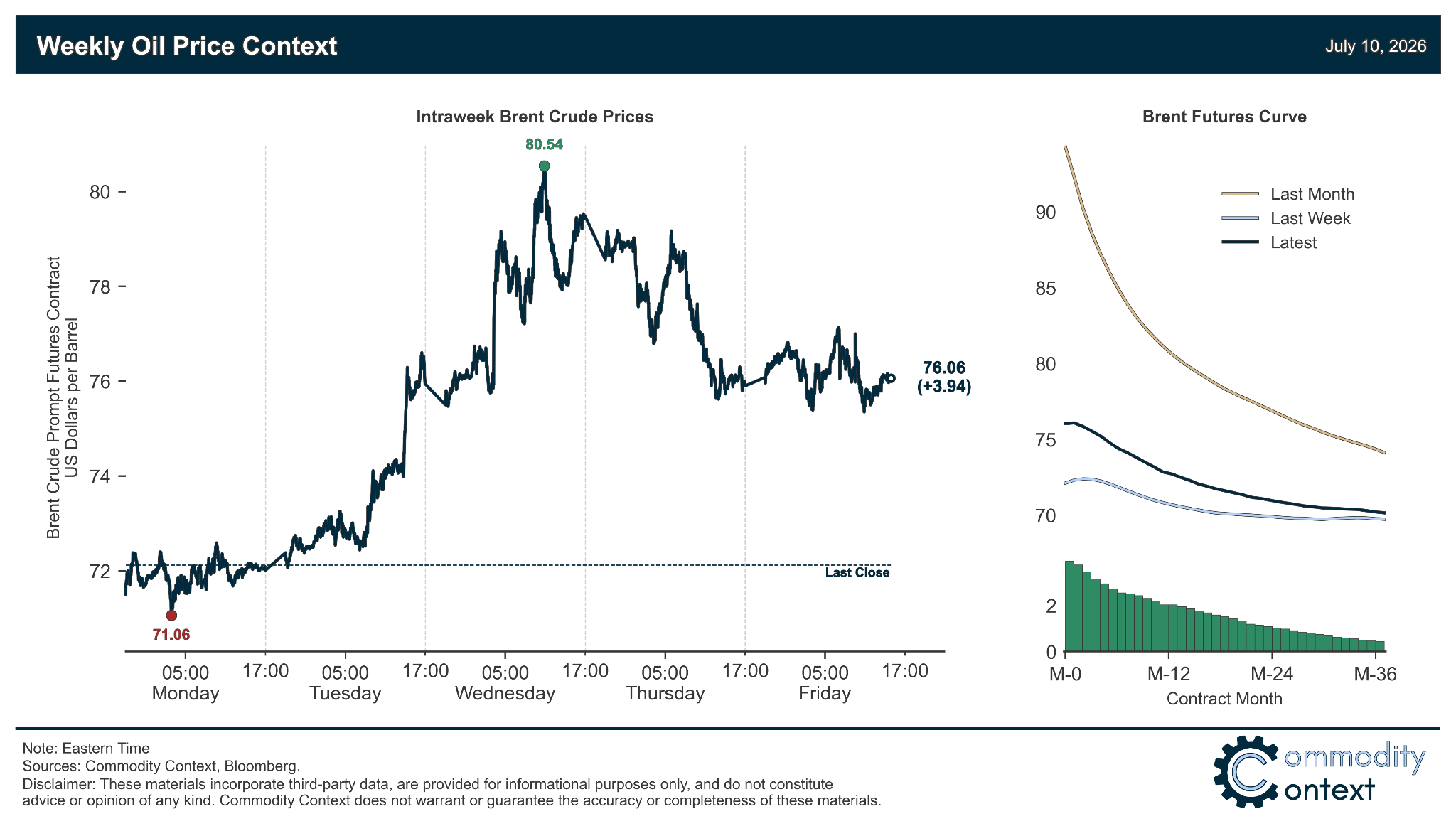

Crude prices jump, see largest weekly gain since mid-May as Iran’s attempt to control Hormuz shipping flows prompted another round of skirmishes that threatened a broader collapse of the MOU ceasefire

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

In the latest episode of the Oil Ground Up podcast, I was rejoined by Gregory Brew, Eurasia Group Sr. Analyst for Iran and Energy, to discuss the fragile peace in the Middle East and why the post-MOU order in the Strait of Hormuz remains fundamentally unstable. (Note: this conversation was recorded immediately before the mid-week escalation in strikes, but I believe Greg’s views still hold up well on what’s motivating the key actors and how far they’re likely willing to go.)

For more public oil market context, check out my conversations over the past week with CNN (video), DW News (video), Global News (video), The Commodities Show with Morgan Downey (video), Geopolitics & Empire (video), and Politico (print).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices registered the largest weekly gain since mid-May, up $4/bbl on the back of the greatest threats yet to the durability of the US-Iran MOU; both sides exchanged protracted fire as Tehran continued to attempt to force compliance with its control of Hormuz.

Timespreads recovered as Brent moved temporarily back into prompt backwardation from last week’s deepening contango; Brent ended the week stronger but still in very modest prompt contango after rolling over alongside flat prices from Wednesday’s high.

Inventories data registered across-the-board draws in the US, ARA Europe, and Singapore, with the pace of drawdowns re-accelerated stateside while slowing modestly in Singapore and ARA; the fact that the first US commercial crude build since mid-April was (1) swamped by SPR draws and (2) further swamped by refined product draws is an excellent summary of the current state of the oil market.

Refined Products markets remain far tighter than crude, caught between Russia’s diesel ban announcement (bullish) and Beijing loosening fuel export restrictions (bearish cracks, bullish crude); while I would have expected the Russian diesel ban to have been priced in ahead of time, the news was met with an aggressive $10/bbl intraday spike in US diesel margins.

Market Positioning data confirmed that speculators were actually once again net sellers of crude futures and options contracts despite the bounceback in prices between the weekly survey windows; this is a bullish print that indicates prices managed to bounce with no depletion of still-growing spec short covering impulse.

As Well As parsing the most violent week in the Strait of Hormuz since the signing of the MOU, which has understandably further stunted the already-slowing pace of shipping traffic in the region; and what do we know about the lower limit on the US SPR’s fill rate?