Oil Context Weekly (W27)

Crude prices were effectively flat this week amidst a comparatively-quiet stretch of summer headlines, with all eyes on the optimistic-but-lurching resumption of Middle Eastern shipping activity.

Happy Friday, Oil Watchers! And happy belated Canada Day and early Independence Day to our North American readers—hope you all enjoy a well-deserved opportunity to unplug.

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

For more oil market context, check out my conversations with and contributions to the MacroVoices podcast (audio), Politico (print), Reuters (print), and the Globe and Mail (print).

Member Exclusive: Context Call on Wednesday, July 8, 2026

Subscribe for details and registration link; paid subscribers will find link below paywall

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

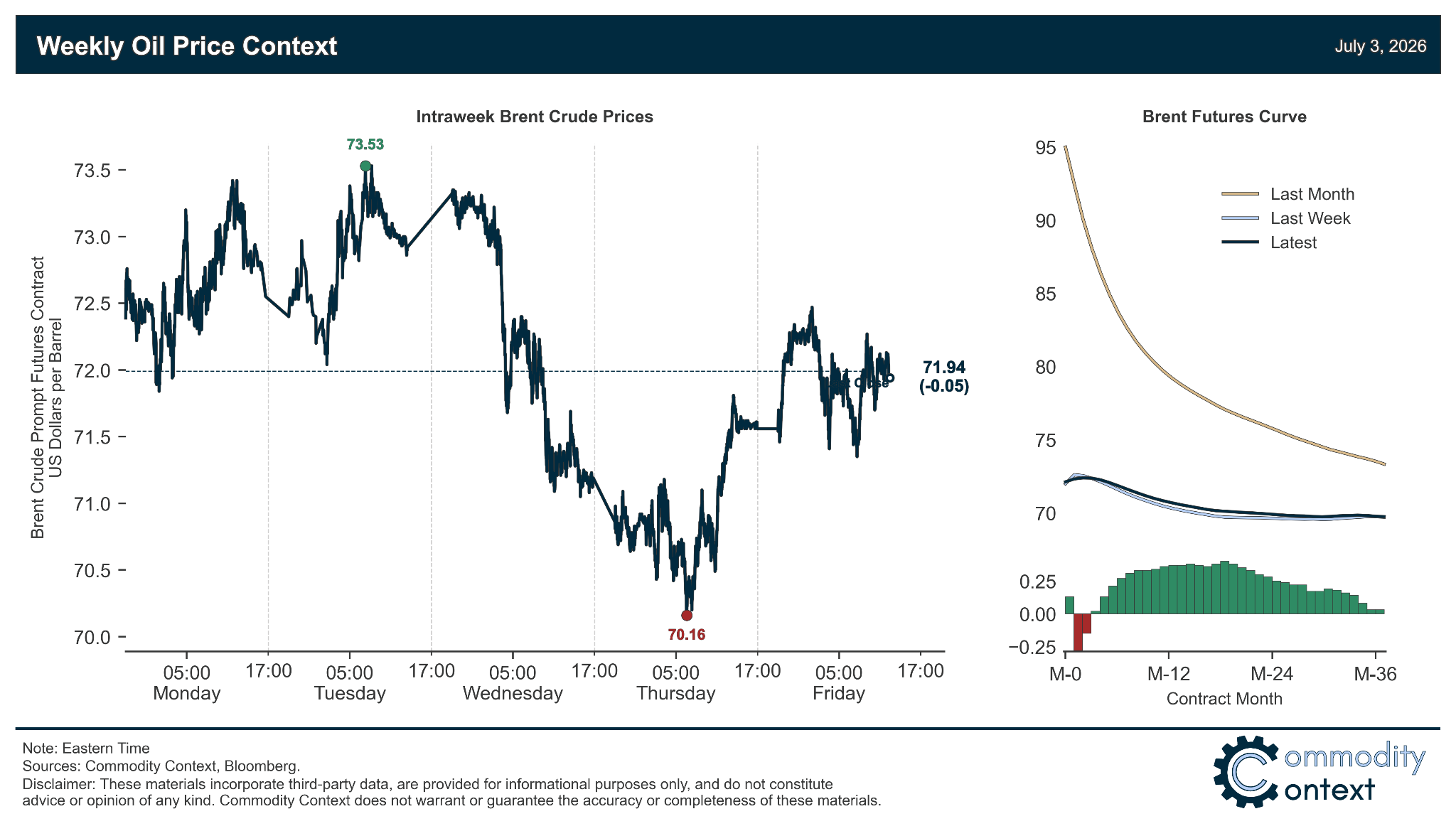

Flat Prices were effectively flat this week with Brent ending around $72/bbl; all eyes continue to track shipping activity developments through the Strait of Hormuz as well as evidence of production restarts across the Middle East, while sentiment remains dour and speculators continue to put downside pressure on prices.

Timespreads remained weak as all major crude benchmarks are either in or on the edge of prompt contango; the market is digesting our current “mini-glut” caused by a surge in exiting Hormuz barrels running up against Chinese-depressed import demand.

Inventories data flipped back to unanimously bullish thanks to draws in all three major trading zones; commercial stocks remain low and continue to draw counterseasonally across most regions and product groups, on top of the ongoing record drawdown in strategic reserves.

Refined Products continue to materially outperform crude: both US gasoline and diesel crack spreads are sitting at the highest seasonal levels on record—at >$50 and >$60 per barrel, respectively—and the highest-ever levels relative to the sinking crude price.

Market Positioning data revealed that speculators were once again notable net sellers of Brent crude futures and options contracts, while broader data published by the CFTC was delayed this week due to the US holiday and will be published on Monday.

As Well As Canadian oil goes further global with new westbound pipeline proposal, and Russia’s refinery crisis bolsters product cracks and further weighs on crude markets.