Oil Context Weekly (W26)

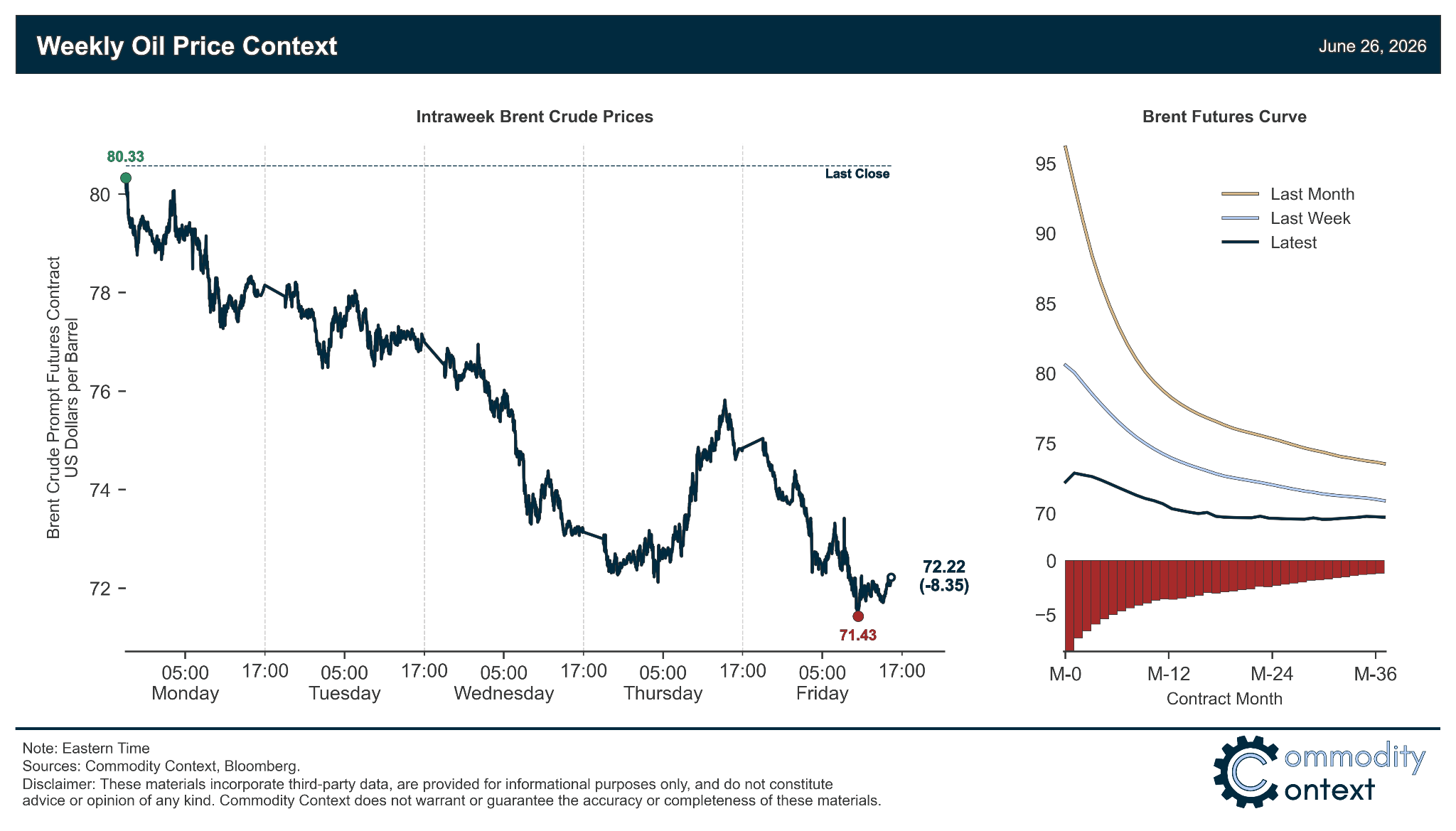

Crude fell another $8.50/bbl and Brent slipped into prompt contango for the first since February as the surge of exiting Hormuz barrels hit a still weak Asian import market with China on the sidelines

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

🎙️ I had the opportunity to rejoin the Odd Lots podcast (audio) this week to talk about how the world managed to avoid the extraordinarily high demand-destructive pricing that I initially thought would have been made necessary by a months-long closure of Hormuz. While there were many small things that added up, the 10,000 lb. gorilla in the room was China’s unprecedented 5 MMbpd cut to its crude oil imports. We still don’t completely know how—or most importantly why—Beijing managed to pull it off, a topic about which I discussed at even greater length on the Shift Key podcast (audio) earlier this week.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices continued to spiral lower, ending down ~$8.50/bbl with Brent in the low $70s, on the back of both (1) ongoing paper market selling and, more fundamentally, (2) the temporary mismatch between the surge of exiting Hormuz barrels and an Asian import market still defined by China’s ongoing buyer’s strike.

Timespreads collapsed on the temporary mini-glut, with Brent and Dubai flipping into outright prompt contango and WTI only managing to hold onto very thin backwardation; term structure is a far more reliable indicator of market condition than is flat prices, and it’s currently telling us that we’re oversupplied relative to demand.

Inventories data leaned bearish thanks to one of the largest weekly Singaporean product stock inflows on record as well as a pop in ARA European fuel oil stocks; US headline inventories fell at their lowest rate since early April despite the large ongoing decline in US crude stocks.

Refined Products went from hot to hotter as US gasoline cracks set a fresh all-time seasonal high—though, they’re starting to feel long in the tooth given the recent bottoming of US gasoline stocks and overstretched positioning—and diesel margins jumped $10/bbl on fears of a Russian export ban given the ongoing collapse of the Russian refining sector under Ukrainian drone attack.

Market Positioning data confirmed that speculators went shorter on crude this past week, driven entirely by a capitulation across gross length and gross spec shorts actually also fell; momentum could still certainly pull us lower—there’s some room to go to last year’s all-time low—but the balance of positioning risk is now largely to the upside and expected to fuel the pace of any rally should the status of Hormuz suddenly deteriorate.

As Well As the crude market is currently oversupplied(?!); a Hormuz jailbreak; and we know that Iran can take the Strait but can Iran HOLD the Strait?