Oil & Iran War Context Weekly (W25)

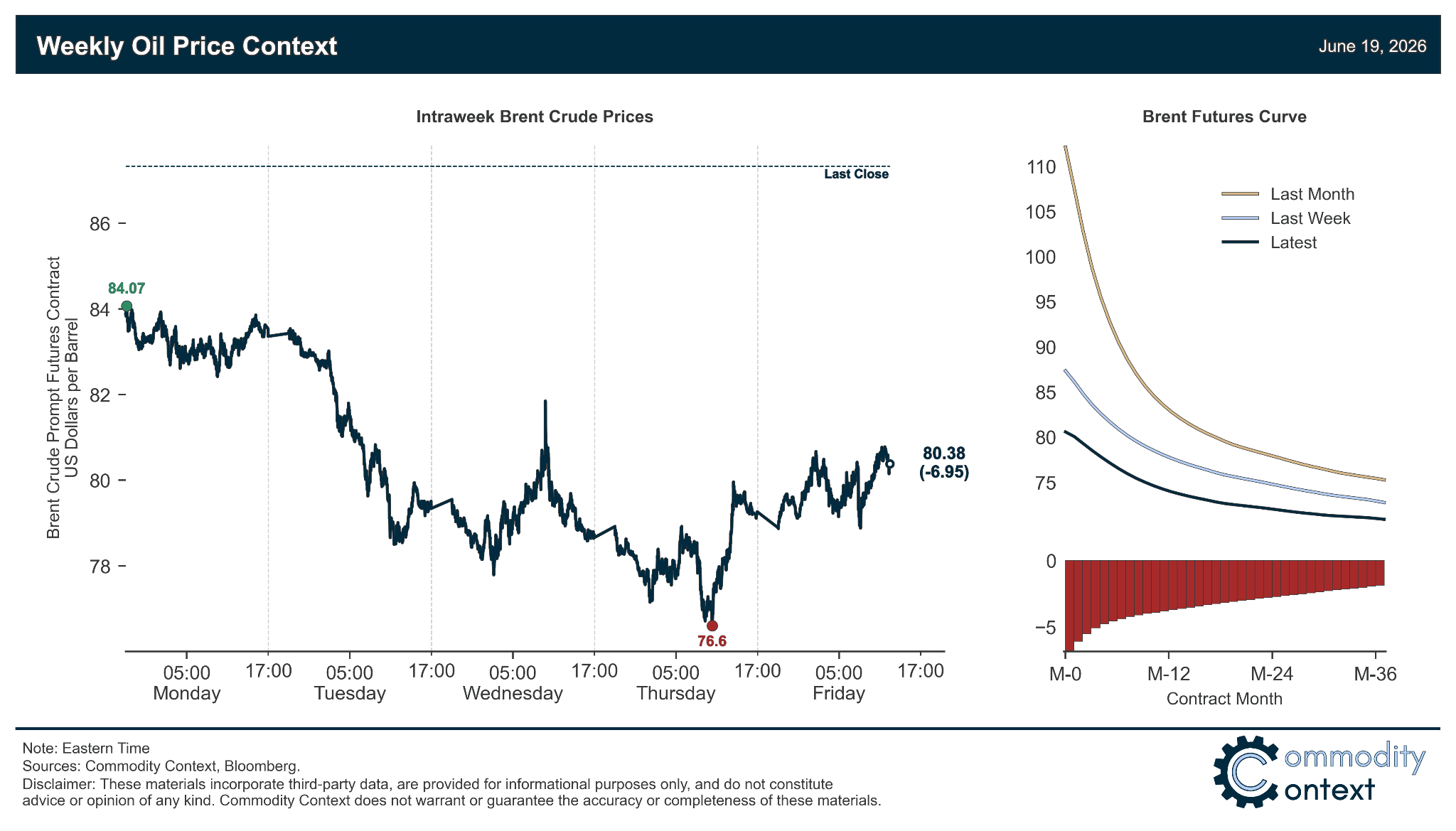

Crude plunged and curves flirted with prompt contango on the back of massive speculative short-selling following the announcement and signing of the US-Iran MOU to end the Iran War and reopen Hormuz.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

For additional complementary oil context, check out my appearances over the past week with the Money and Mine podcast (video), CBC’s Power and Politics (video), The Wall Street Journal (print), The Atlantic (print), NBC News (print), CBC News (print), and Vox (print).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices fell ~$7/bbl following the announcement and subsequent signing of the US-Iran MOU, driven by an enormous volume of speculative short-selling on the back of optimism that transits through the Strait of Hormuz will rapidly normalize and flip the oil market into renewed surplus.

Timespreads also sank under the weight of that same normalization optimism, with Dubai crude contracts plunging into outright prompt contango and both Brent and WTI on the edge of falling back into contango themselves for the first time since February.

Inventories continued to crater across the US and ARA Europe, only slightly offset by a modest build in Singapore off an extraordinarily low base.

Refined Products markets are seeing increased gasoline tightness as US gasoline crack spreads ripped higher, back to near crisis highs and on the edge of breaking above 2022’s all-time high seasonal refining margins.

Market Positioning data confirmed that speculators saw their largest weekly reduction in net Brent position (CFTC data delayed until Monday) through the Hormuz crisis, with the net position sitting at its lowest level of 2026 and gross short positions experiencing their steepest climb on record to within ~1 million barrels of the all-time high Brent short position recorded in December; covering this gargantuan short position will provide rocket fuel to any future crude rally.

As Well As the Memorandum of Versailles; US concessions; chaotic start to Hormuz reopening and renewed threat to stability of the MOU; reassessing Hormuz oil transit flows; tracking Gulf production restarts; and the implications of the IEA’s latest 2027 glut forecast.