Oil & Iran War Context Weekly (W24)

Crude prices sank to the lowest weekly close since February on the back of a whiplash shift from missiles flying across the Gulf to what most parties are now presenting as an imminent MOU-signing.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

Also a reminder that paid subscribers can access the latest weekly update of the detailed 40-page PDF Market Positioning Data Deck at the bottom of this report.

For even more context, check out my NYC video appearance with Paul Sankey (video, go Knicks!) as well as my comments to the Financial Times (print).

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

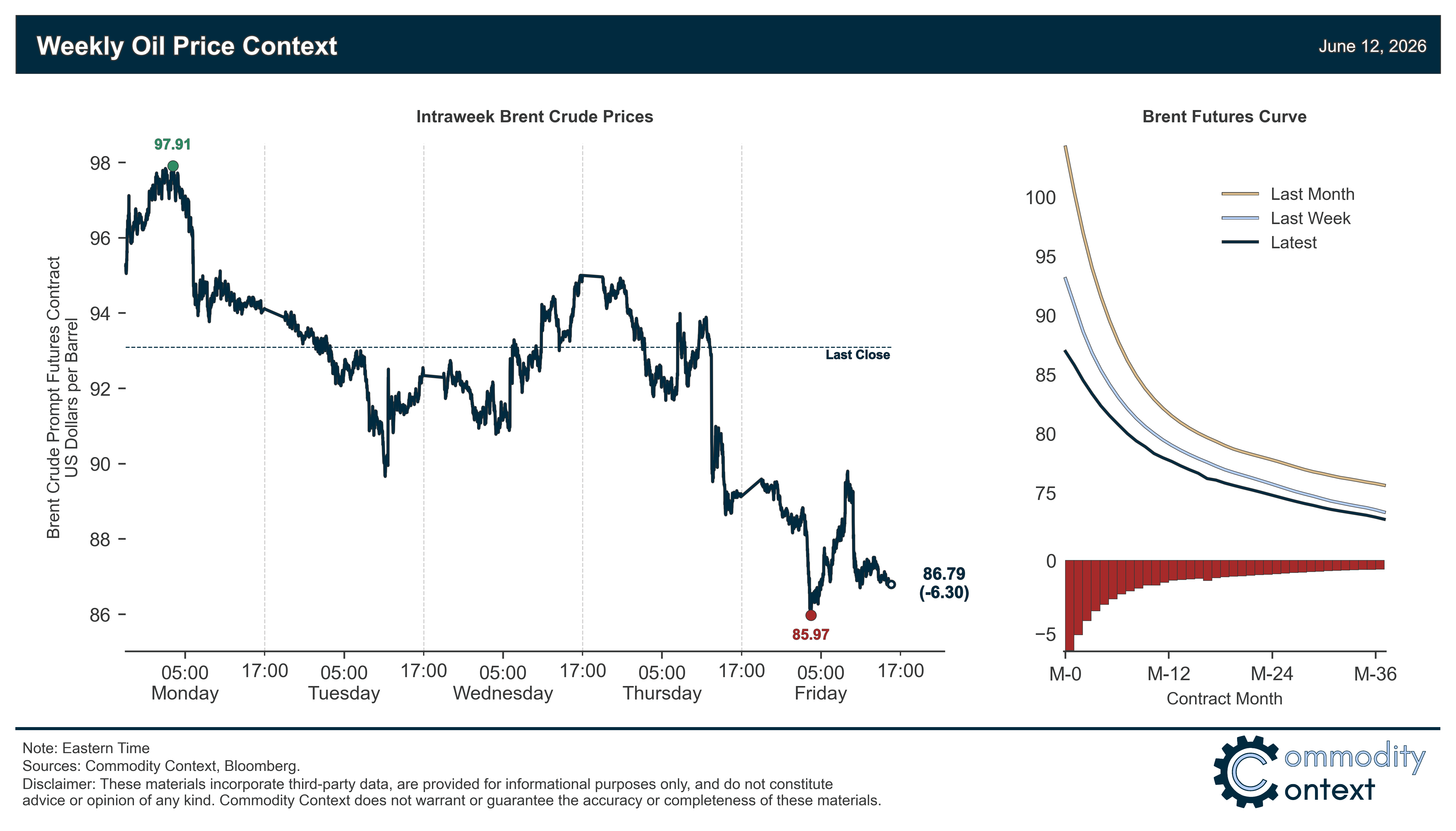

Summary

Flat Prices sank $6/bbl on the back of the most optimistic torrent of MOU-optimistic headlines since April and Brent crude finished at its weakest since the beginning of the Iran War (around $87/bbl); Brent traded as low as $85.80/bbl in earlier Friday trading, also the lowest intraday tick of the Hormuz Crisis and exceeding, even, the steep mid-April selloff.

Timespreads continued to weaken alongside flat prices, with prompt spreads of all major benchmarks slipping tightly from around $2–3/bbl to $1–1.50/bbl; despite plunging inventories, crude term structure remains the strongest counterargument to ongoing, acute supply tightness.

Inventories data leaned bullish given large stateside crude draws and a continued sharp rout in Singapore that furthered last week’s collapse and brought fuel stocks to their lowest level since 2013; these draws were blunted, only somewhat, by a crude-driven build in ARA European stocks.

Refined Products markets saw gasoline crack spreads rise amidst still-precariously low US stocks and diesel margins fade alongside crude on Iran MOU optimism.

Market Positioning data again confirmed broad selling of crude oil futures and options by speculative participants; the net speculative position as a share of total open interest across the six largest crude contracts fell to the lowest level since mid-February, when Brent crude prices were more than $20/bbl lower.

As Well As kinetic-to-diplomatic whiplash; do we actually have an MOU deal?; cash is king; measuring the Hormuz “leak”; and my NYC trip reflections on current sentiment.