Oil Context Weekly (W23)

Crude prices recovered to around their highest level since April as speculators returned to the barrel, while the rise and fall of Western Canadian wildfire concerns drove WTI term structure.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

New Podcast: In the latest episode of the Oil Ground Up podcast, I spoke with Tamas Varga—a 30+ year veteran and analyst at PVM, the world's largest oil market broker—to parse the contradictory signals in the current crude market.

I had the opportunity to join BNN Bloomberg early in the week to discuss the latest OPEC+ meeting, which you can watch in full here.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

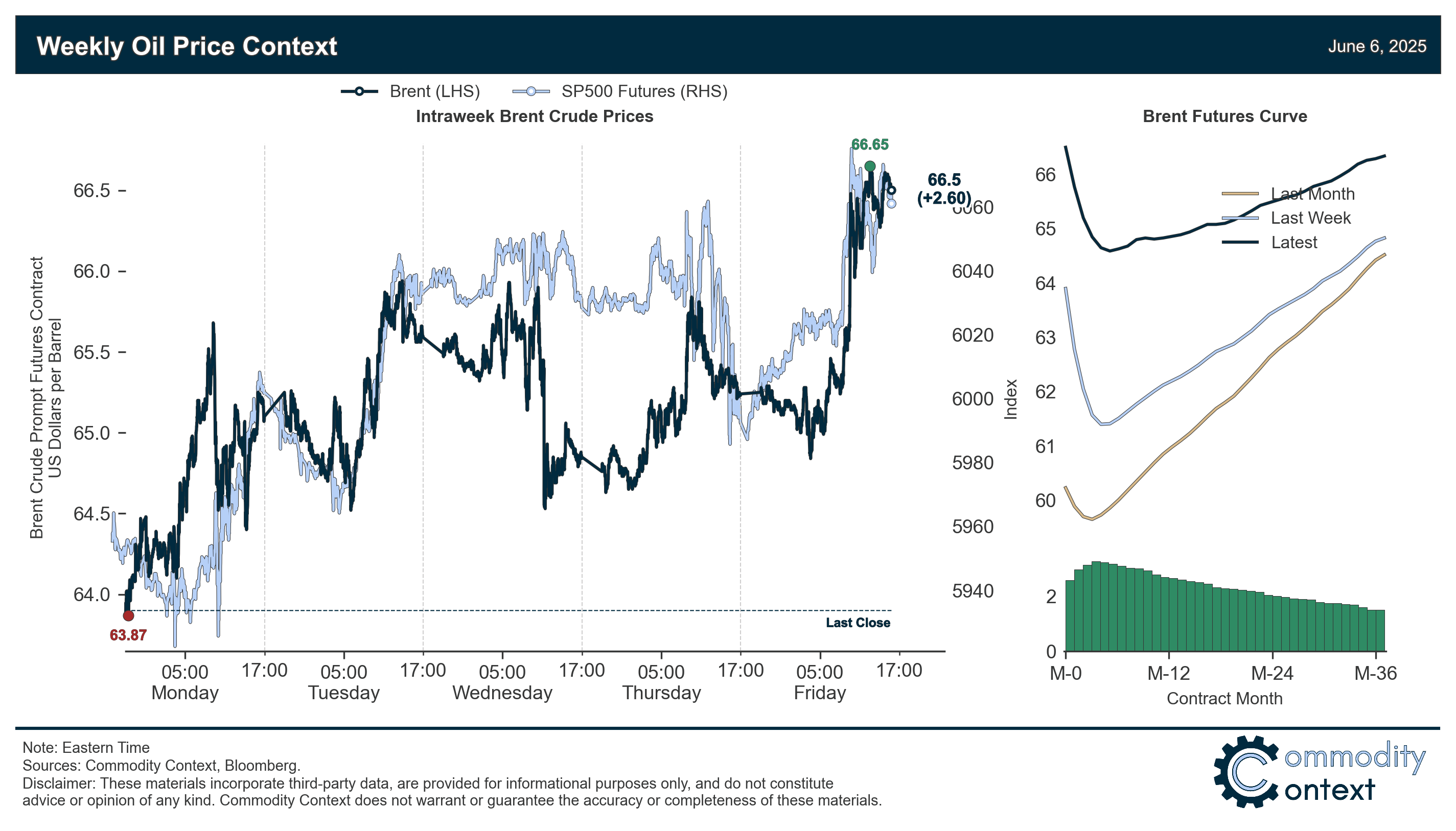

Summary

Flat Prices rose nearly $3/bbl to roughly $65.50/bbl, just shy of their highest level since April.

Timespreads broadly weakened following last week’s run-up but then rapidly recovered to effectively flat in a strong Friday rally; Dubai was the only major benchmark to see its prompt timespread steadily rally.

Inventories data was mixed but leaned bearish on the back of the largest US headline stock build in a year, but those builds are coming off deeply depressed levels and all major stock hubs are holding headline stocks below the seasonal norm.

Refined Products were split between diesel and gasoline, with the former strengthening and the latter continuing to weaken into what should be the season of strongest demand and richest refining margins.

Market Positioning data revealed that speculators are on again reaccumulating crude length, helping explain the rise in flat pricing despite a commensurate improvement in term structure; while there’s still more available upside than downside, we’ve also now reached a point where speculators hold enough gross length that prices could be vulnerable to a sharp liquidation-related selloff if hit with a bearish enough headline development.

As Well As OPEC+’s “accelerated” production hikes are by now the new normal, the US oil rig count continues to plummet, and the IEA expects global oil investment to decline this year for the first time since COVID-battered 2020.