Oil & Iran War Context Weekly (W14)

War marches on and President Trump committed to weeks more fighting; Dated Brent crude prices hit their highest level since 2008 above $140/bbl and all crudes are experiencing record backwardation.

Happy Good Friday and Easter, Oil Watchers!

Hope you all enjoy some well-earned time off after an exhausting month in the oil market.

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re looking for some more Iran war/oil market implications coverage, check out my conversations on Breaking Point (Video); Milk Road (Podcast); CBC Power & Politics (Video); and Hidden Forces (Podcast) as well as read my latest contribution to The Dispatch (Print).

🎙️ Podcast Double Header:

On the latest episode of Oil Ground Up, I was joined by Karim Fawaz, Energy Advisory at S&P Global, to discuss the market’s irrational Iran War optimism given the unthinkability of a long-term Hormuz closure and what destroying 10+ MMbpd of demand could actually look like.

And earlier this week on Oil Ground Up, I spoke with Gregory Brew at Eurasia Group about Trump killing the Carter Doctrine and how to think about the political contours of the Iran War on all sides of the conflict and how they constrain our path forward.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

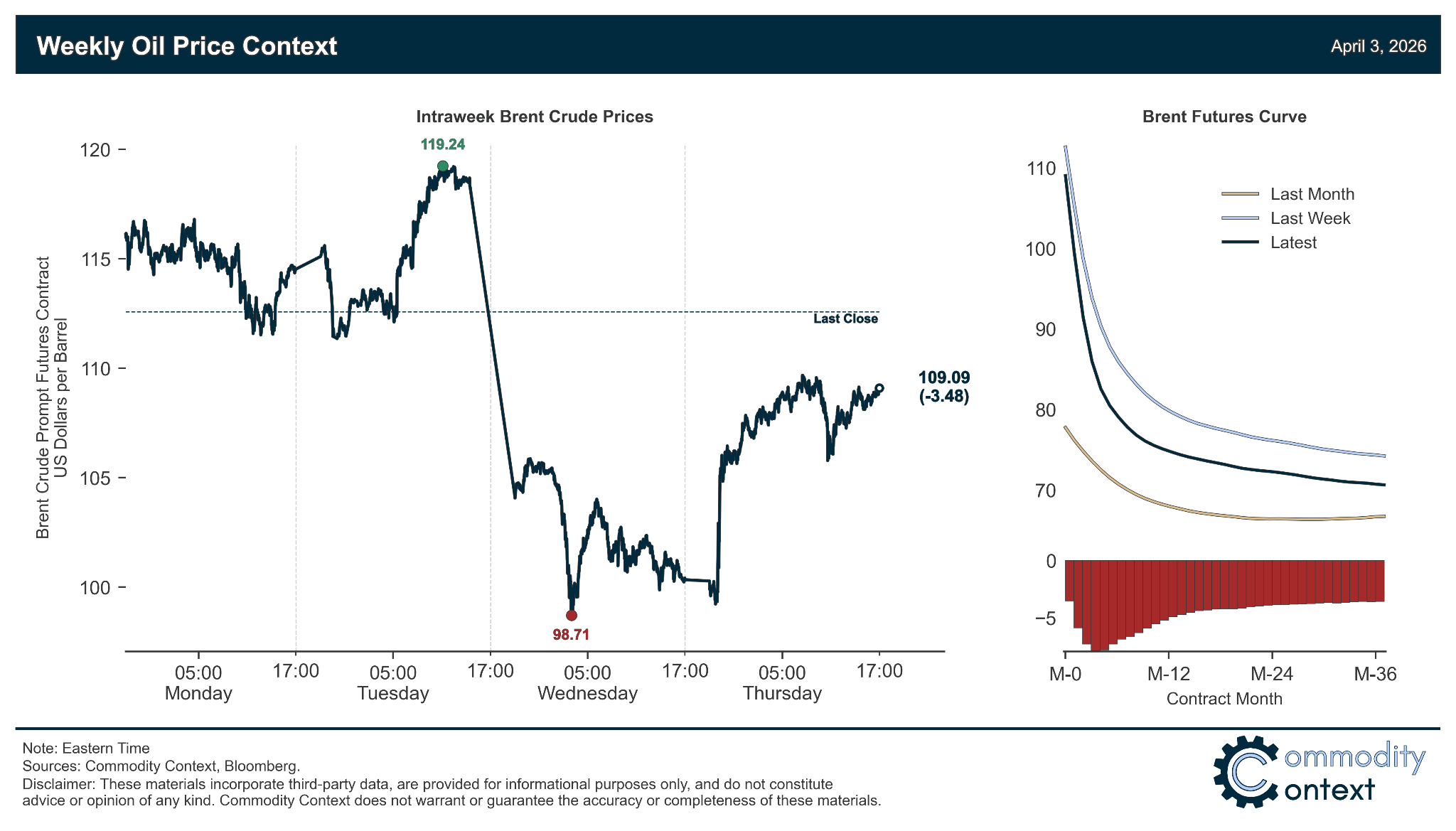

Flat Prices slipped on the basis of prompt Brent futures contracts, falling ~$3.50/bbl to $109; however, that decline was driven by the expiry of the steeply backwardated May contract and the June contract actually ended nearly $4/bbl above last Friday’s close. On Thursday, Dated Brent spot prices hit $141.37, the highest level since 2008.

Timespreads continue to explode and set fresh all-time highs, with the Iran War supply loss being experienced through term structure far more than flat pricing; prompt timespreads of all major crude futures contracts, which we normally discuss in cents, have hit $10–$17/bbl.

Inventories data was mixed between draws across the US and Singapore and a crude-driven build in Europe; however, we still have yet to see the Hormuz closure scarcity show clearly in the high frequency inventory data, with crude stocks in the US and Europe actually rising faster than usual for this time of year.

Refined Products continue to be dominated by squeezed middle distillates, with diesel crack spreads sitting at their highest-ever seasonal levels; but, we’re beginning to see the refining pain spread to gasoline as well, which is seeing refining margins roughly 50% higher than seasonal.

Market Positioning data showed that speculators were net sellers of WTI crude contracts over the past week, though we’ll need to wait until next week for Easter holiday-delayed ICE commitments of traders data to be more confident in our current positioning picture.

As Well As adjusting our view to a longer war following Trump’s speech, the billion barrel cost of that longer war, weakening prospects of a near-term diplomatic resolution, Tehran’s future plans for the Strait of Hormuz, and the timeline for the arrival of the Hormuz “air pocket”.