Oil & Iran War Context Weekly (W10)

US-Israel-Iran war shocks oil market but prices, while sharply higher, are still far from reflecting the true damage already done, let alone the existential risk the market now faces.

There was one story and one story alone in the oil market this week; so, this weekly report is dedicated entirely to critical developments in the US-Israel-Iran war, including the stoppage of shipping flow through the Strait of Hormuz and the varied impacts on the global petroleum market so far.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

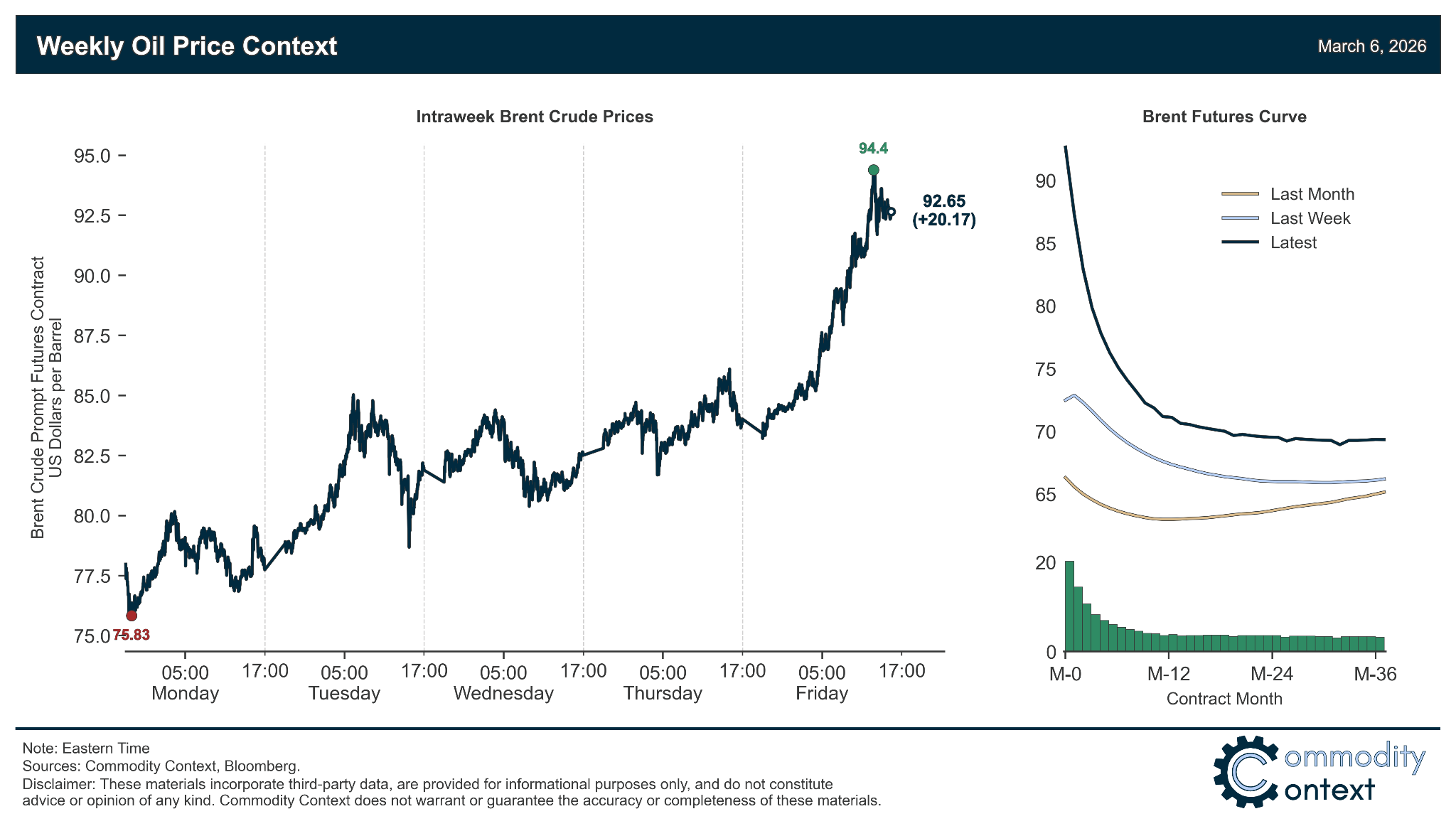

Flat Prices surged higher as the true extent of the US-Israel-Iran war sunk in for market participants; Brent was ~+$20/bbl to finish around $93/bbl, the highest close in more than two years and the largest weekly gain since March 2022 (i.e., Russia’s invasion of Ukraine).

Timespreads have exploded across all major benchmark grades; prompt spreads and Brent DFLs went from modestly backwardated—even sinking into outright contango last week—to astronomically backwardated, at $4–6/bbl as of trading today, as refineries scramble to secure every possible barrel.

Inventories data leaned incrementally bearish last week given modest builds across all major tracked hubs; but, data is as of the day immediately prior to the US and Israel launching their combined assault on Iran and traders aren’t currently pricing crude on where stocks stood last week—they’re pricing barrels on where things might be or, rather, where they might not be next week.

Refined Products were again dominated by gigantic moves in the relative price of middle distillates including diesel, gasoil, and jet fuel, especially in Asia; US diesel crack spreads rose by more than 50% on the week, while Singaporean jet fuel margins rose by 300% as Asian refineries preemptively

Market Positioning data revealed that speculative participants were only small net purchasers of crude contracts over the past week-through-Tuesday, though that statement masks large gross reductions in both long and short positions as speculators flee the volatile market; given the relatively modest net increase in spec positions (vs. price gains), we can imply that virtually all the week’s price action was driven by panicked refineries buying virtually every barrel not on the wrong side of Hormuz.

As Well As Oil prices remain well below where they should be given the current trajectory of effective closures in the Strait of Hormuz, Trump admin flailing on oil price spike, refined products impact will front-run crude as the relative value of middle distillates soars, Saudis tap emergency pipeline plan, and why Moscow is the greatest immediate beneficiary of the war against Iran.