Oil Context Weekly (W9)

Iran risk continues to stoke the paper market, but signs of physical barrel weakness are spreading and getting worse as contango returns to the Brent market.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

🎙️ On the latest episode of the Oil Ground Up podcast, I was joined again by Rachel Ziemba, my favourite person with whom to parse the everchanging details of the US sanctions regimes that are currently exerted outsized pressure on the global oil market.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

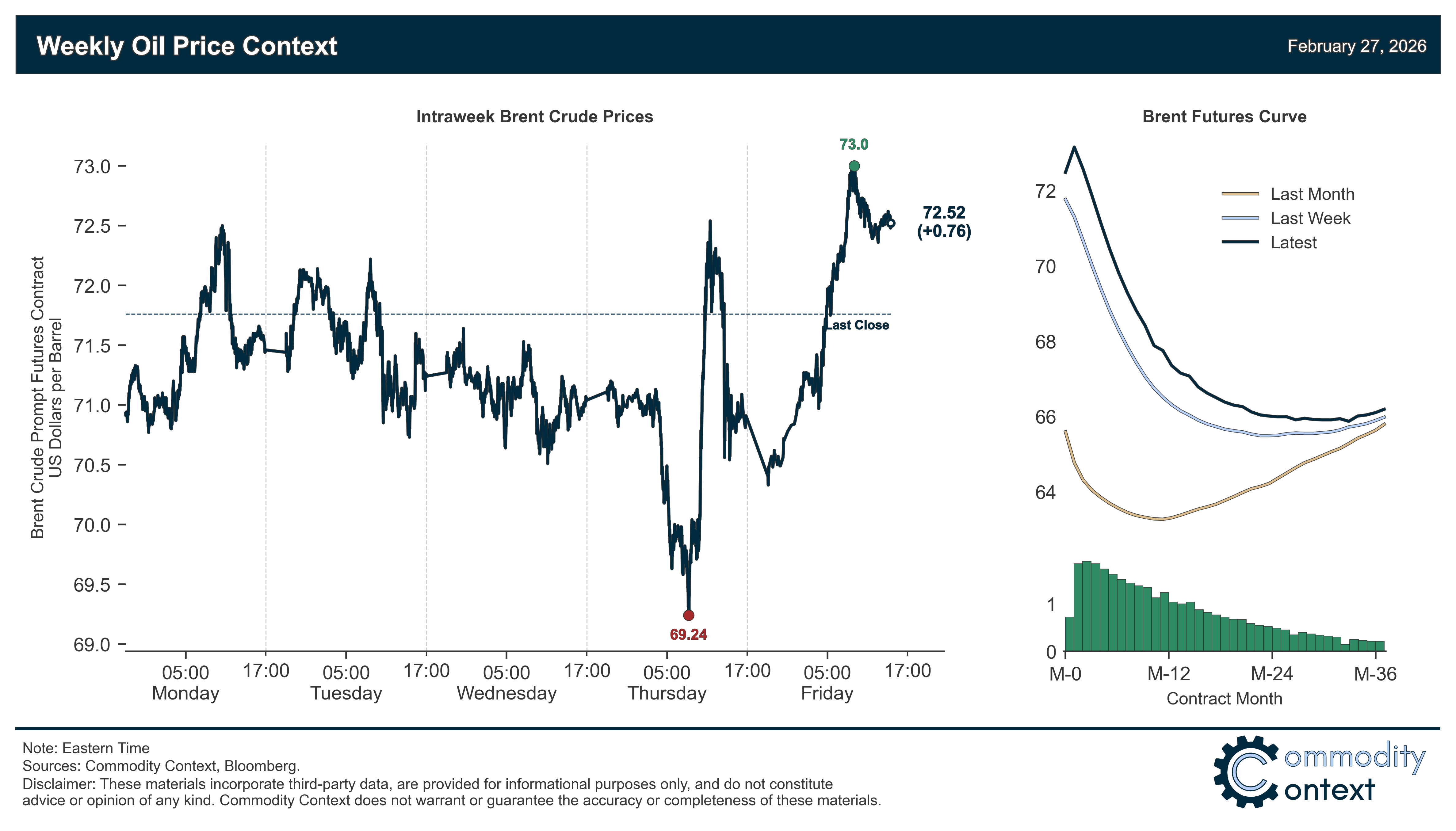

Flat Prices bounced between $69–73/bbl (Brent), reacting quickly and sharply to every Iran negotiation-related headline, but finished <$1/bbl up to end around $72.50/bbl (Brent).

Timespreads continued to weaken as both prompt Brent timespreads and Brent DFLs slip into outright contango; the collapse of DFL spreads into contango—for the first time since 2024—is an undeniable sign that Brent structure is both not confirming the Iran-torqued flat price rally and, likely, feeling spot market pressure from surging freight rates.

Inventories data was mixed given a notable bounceback in previously-plunging US stocks but sizable draws across ARA Europe and Singapore; the steep rise in US crude stocks put those inventories back on seasonal track while large draws across ARA Europe and Singapore pushed Northern European crude stocks to precariously low levels.

Refined Products rallied, with diesel, in particular, boosted even more by Iran concerns than seen in flat crude pricing; middle distillate markets remain exceptionally sensitive to the prospect of disruptions in the Middle East, which has become a crucial source of diesel supplies for Europe following EU bans on the import of historic mainstay Russian diesel.

Market Positioning data confirmed that speculators were once again large buyers of crude futures and options contracts, and that the net bias of these positions has risen to exceptionally high levels indicative of a roughly $5/bbl premium in flat pricing; however, given the propensity of the crude market to overreact on the downside during liquidations of these overbuild spec length cycles the downside price risk is likely now pushing $10/bbl if Iran risk is unwound.

As Well As US-Iran negotiations keeps the oil market on its toes and the Bridger Pipeline Expansion provides another opportunity for Western Canadian egress capacity growth.