Oil Context Weekly (W4)

Crude prices rallied on a cornucopia of both realized and feared hits to global supplies: from further losses of already-wounded Kazakh supply to an unexpected winter storm to renewed Iran risk.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

🎙️ I had the pleasure of rejoining the Macro Hive podcast (YouTube link) to talk about how to parse the numerous conflicting data points and narratives in the oil market, including the importance of distinguishing between supply vs. production, demand vs. consumption, and the character and location of inventories.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

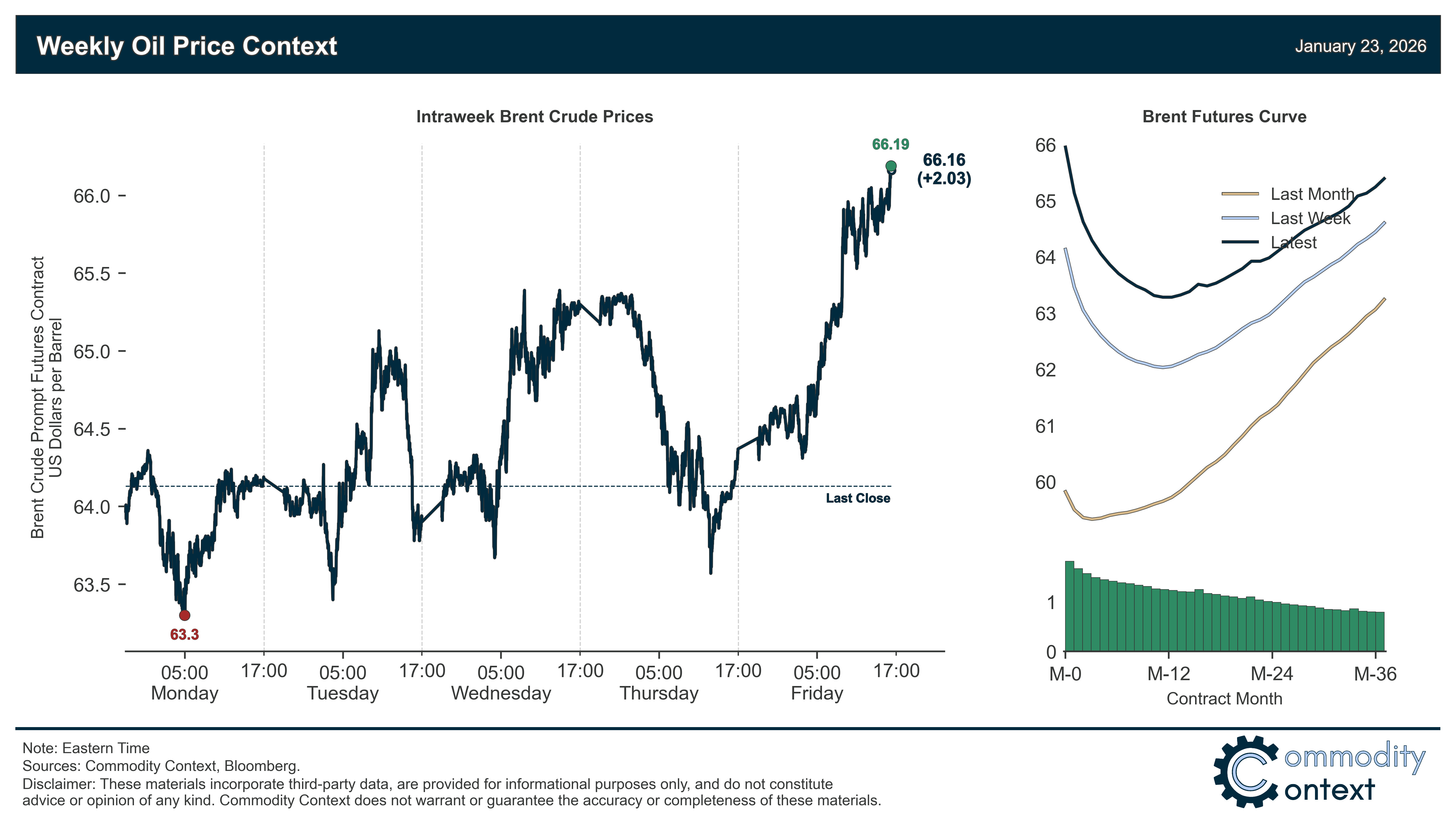

Flat Prices rallied $2/bbl to finish above $66/bbl Brent, supported by fundamental stressors like the ongoing loss of Kazakh crude supplies, the winter storm bearing down on North America, as well as the lingering and spiky Iran-risk amidst an “armada” of US warships steaming toward Iran.

Timespreads were split: Brent is still exceptionally bid on both Iran risk hedging and realized Kazakh production losses while other crude grades saw prompt time spread flat to lower.

Inventories data were also split given big builds in the US and draws across both ARA Europe and Singapore; across all three hubs, stocks of crude and middle distillates remain low—albeit rising counterseasonally—but gasoline stocks are high and generally rising at a faster-than-usual pace; consecutive builds through the beginning of the 2026 have put US stocks on a firmly bearish trajectory to kick off the New Year.

Refined Products were dominated by a massive 20+% rally in diesel crack spreads on the back of the massive winter storm bearing down on North America; while boosting heating demand (diesel rallied in lockstep with natural gas, which shot 70% higher in two days), the storm is also expected to weigh on supply given cold weather complications in refinery operation.

Market Positioning data confirmed little change in speculative crude positioning in aggregate over the past week-through-Tuesday but there were material divergences between major crude benchmarks: Brent and WTI experienced net buying while Dubai saw nearly half its net speculative length cut on the week, helping explain the Middle Eastern medium sour benchmark crude’s comparative underperformance.

As Well As CPC Terminal struggling to get back on its feet—and, now, a fire at Kazakhstan’s largest oilfield, Iran remains in focus and risk premia spike ahead of weekend amidst renewed sabre rattling, first end-buyer sales made by new US-led Venezuelan crude marketing push, Trump administration backtracks on security guarantees for oil operators in Venezuela, and Winter storm spikes heating demand and sparks concerns of supply losses.