Oil Context Weekly (W52)

‘Twas the final week of the year for the oil market and not a creature, trader, or headline was stirring

Happy Friday and Merry belated Christmas, Oil Watchers!

This will be a slightly shorter Oil Context Weekly report given that it was a pretty slow week for oil-related news flow and for crude prices. Keep your eyes open for our year-end wrap-up, Oil in 2024, next week.

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

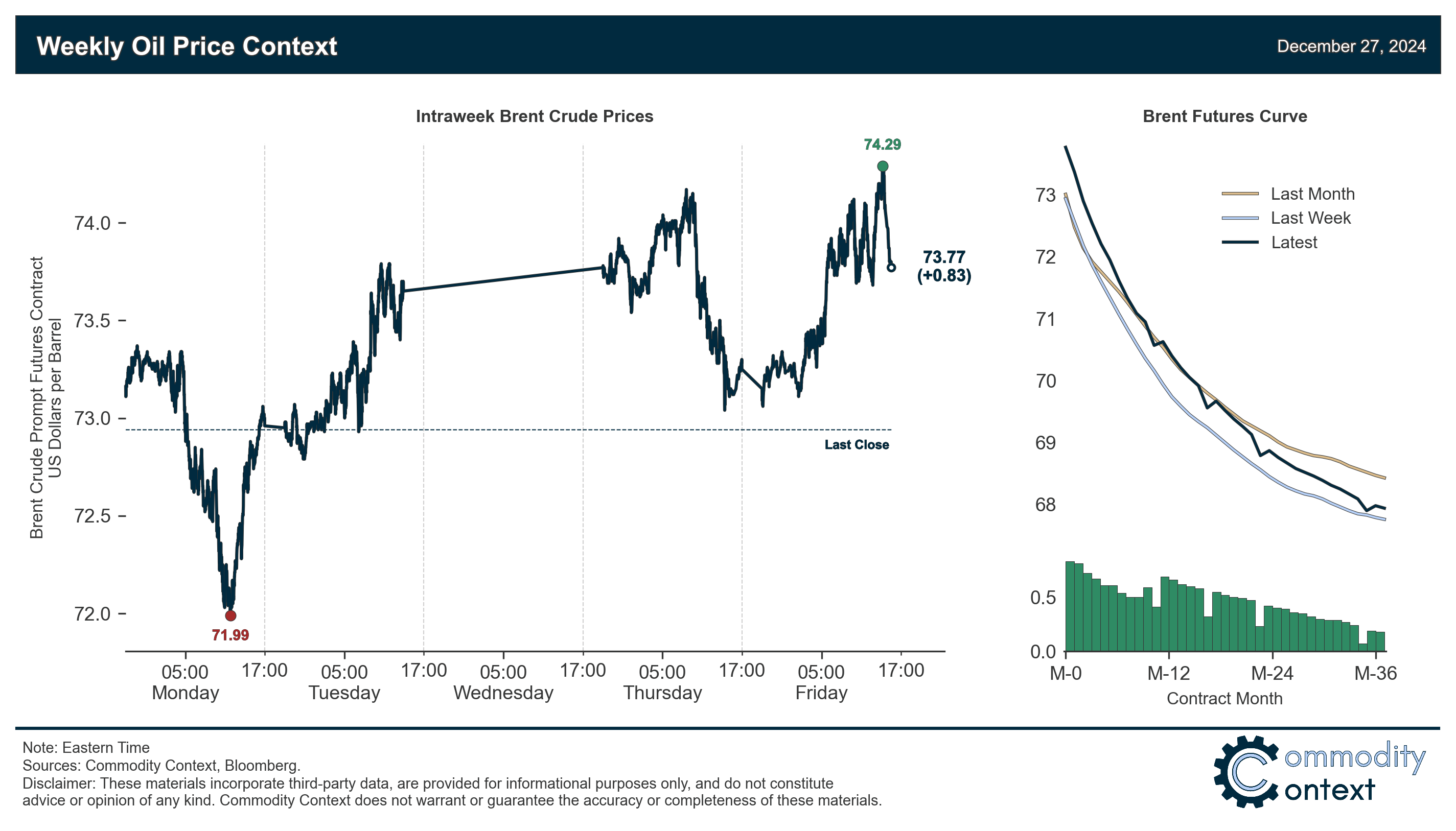

Flat Prices rose roughly $1/bbl over the Christmas week to end just below $74/bbl (Brent)—the upper end of its months-long range but still lacking anything close to durably directional momentum.

Timespreads were effectively flat amidst shallow trading and a lack of any real fundamental news flow, with a Friday rally in Brent CFDs the only real sign of life (but hard to get excited this close to the end of the month).

Inventories data leaned bullish thanks to large draws in the US and Singapore, though the Stateside draw tracks a long-held year-end pattern of crude inventory declines in December (thanks to tax treatment effects) and the Singaporean draw partially offset an even larger fuel-oil-driven build the prior week.

Refined Products weakened this week, with both gasoline and diesel margins sinking.

Positioning data typically published on Friday has been delayed by both ICE and the CFTC given the Christmas holiday and will be published on Monday December 30th.

As Well As Christmas Cracks Emerge in Trump Coalition, Beijing Announces Yet More Stimulus, and the First VLCC is Scheduled For Scrapping Since 2022.