Oil Context Weekly (W47)

Another week of falling prices, volatile policy rumours, and concerning curve weakness; also confirmation that last week’s violent price rout was driven by the largest spec liquidation since March

Welcome to Oil Context Weekly, my less formal wrap-up of the market analysis, news flow, and data releases that matter.

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely—highlights now included in the free summary.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

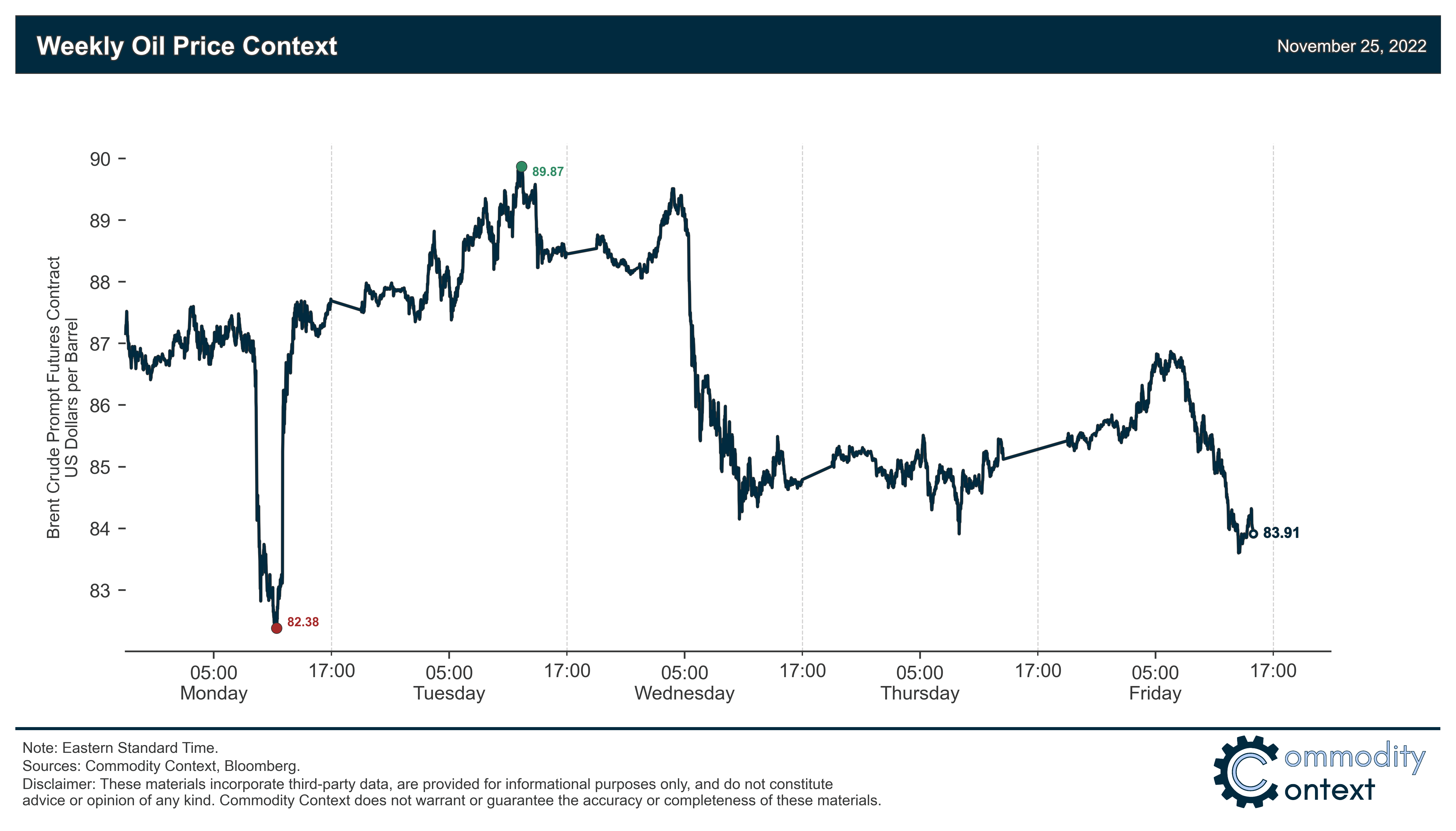

Summary

Flat Prices fell by $4/bbl this week to roughly $84/bbl (Brent basis), weighed down by easing concern regarding strict Russian price cap enforcement and a weaker spot market evidenced by intermittent contango across the front of both the Brent and WTI futures curves.

Calendar Spreads were once again a source of concern for crude market structure this week as Brent crude’s prompt spread followed WTI’s lead last week and flipped into contango multiple times over the past five days. While the front of WTI’s curve remains in contango even after the month-end settlement on Monday, the rest of the curve, beyond the front few months, remains in decently steep backwardation—but even that, too, has been easing off over the course of the week.

Inventories data was mixed, with builds in the US (+3.3 MMbbl) and Europe (+1.0 MMbbl) being partially offset by a draw in Singapore (-1.1 MMbbl). US crude inventories drew but were overwhelmed by product inflows, while commercial stocks of hyper-tight gasoil and diesel fuel rose across all major regions for the first time in 11 weeks.

Refined Products showed easing tightness for diesel crack spreads, which fell in New York Harbor from around $60/bbl at the beginning of the week to around $53/bbl at the time of writing, it’s lowest level since mid-September supported by across-the-board inflows of middle distillates inventories.

Positioning data for ICE Brent contracts (US data delayed due to Thanksgiving, released Monday) confirmed one of the largest speculative liquidations of the year; net managed money positions in Brent contracts fell by 70.5 MMbbl on the back of 52.7 MMbbl of long liquidations and the establishment of 17.8 MMbbl of fresh shorts, marking the largest weekly reduction in net length since early March when extreme volatility prompted a mass exodus; net spec positions as a share of open interest are now back down to 5.8%, which is their lowest level since early August.

Russia’s Price Cap was once again the source of negotiation breakdown this week as parties failed to converge around an acceptable price level for the cap; they’re cutting it especially close given only 9 days remain before the embargo against and shipping-related sanctions on Russian seaborne crude take effect (~800+ more words on this below).