Oil Context Weekly (W46)

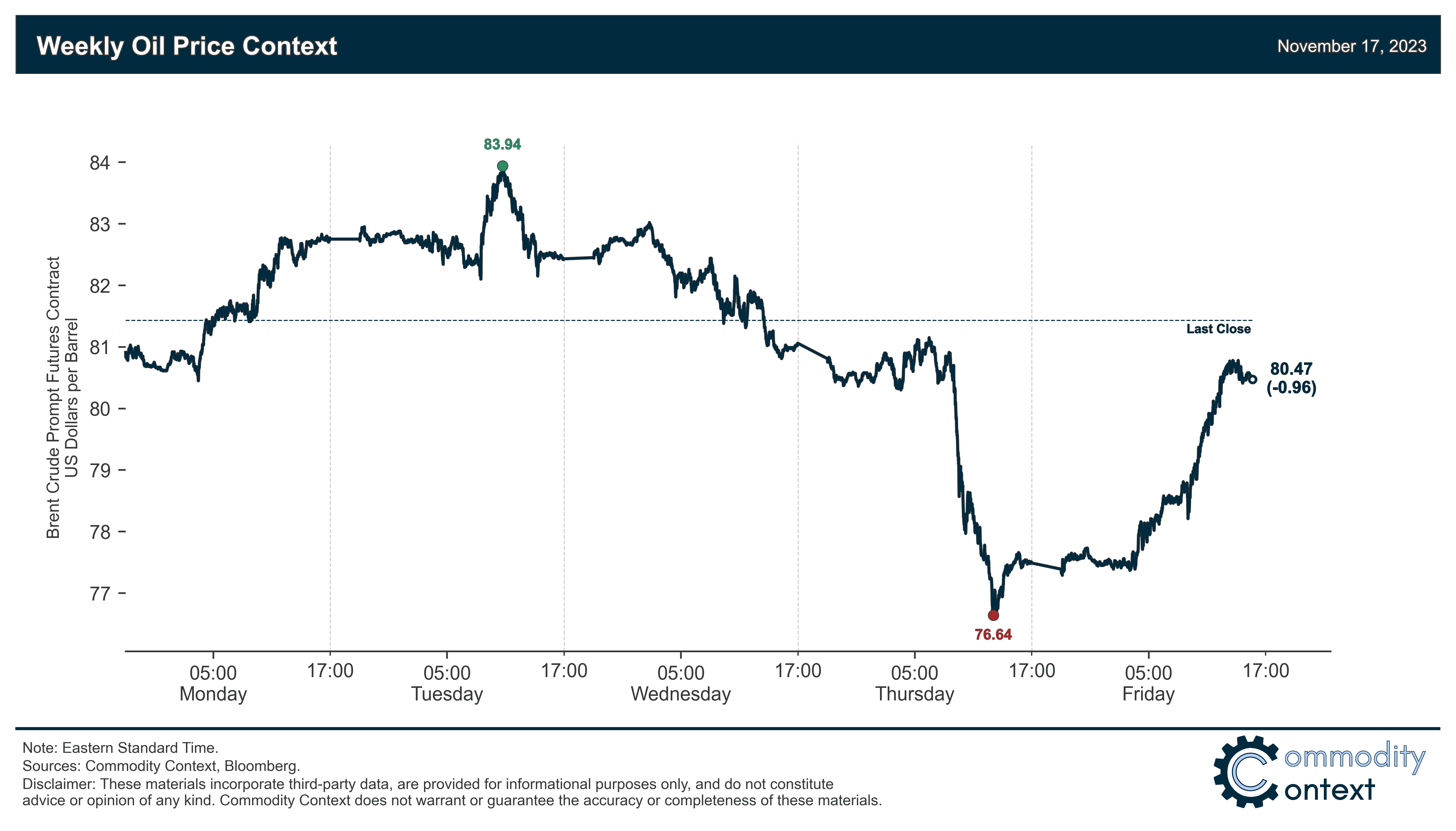

Crude prices crashed on further speculative liquidations before those very declines jump-started the pre-meeting OPEC rumor mill, ultimately pressing prices sharply higher again through a Friday rally

I had the opportunity to discuss recent oil market weakness earlier this week on BNN Bloomberg’s The Close—encourage you to check out that full interview here.

Happy Friday!

Every week, I summarize developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices experienced quite the rollercoaster, plunging into a technical bear market on Thursday before getting jolted back to life Friday on rumours of potential OPEC+ support later this month; Brent crude ended roughly $1/bbl lower on the week at ~$80/bbl.

Futures Curve generally confirmed the moves in flat prices, with calendar spreads slipping gradually lower through the early week, dropping suddenly on Thursday, and, ultimately, experiencing a combined recovery; Brent’s prompt spread briefly flipped into contango for the first time since June before finishing the week modestly backwardated.

Inventories data leaned bearish driven by small builds in Singapore and ARA Europe, while the double-week EIA data release confirmed substantial crude builds (~17.5 MMbbl over two weeks) were offset by nearly-equivalent refined product draws.

Refined Products were generally staid compared to the whiplash in crude, ending slightly higher on the week, supported by lower US refined product stocks; volatility is expected to remain concentrated in crude ahead of upcoming OPEC+ meetings.

Investor Positioning data confirmed that speculators were net sellers of crude over the past week through Tuesday, continuing the steepest selloff in speculative positions this year after reaching a high-water mark in mid-September; while still not the net-shortest we’ve been this year, investor positioning is undeniably bearish and puts positioning risk (i.e., the price pressure associated with inevitable sentiment normalization) squarely to the upside.

As Well As hopes of further OPEC market support as the pre-meeting rumor mill is kicked into high gear and what looks like yet another false start in the nearly year-long efforts to restart Iraqi Kurdish crude exports out of Turkey.