Oil Context Weekly (W45)

A flat-ish week for crude prices really isn’t a sign of oil market strength when the US dollar falls by more than 4%.

Welcome to Oil Context Weekly, my less formal wrap-up of the market analysis, news flow, and data releases that matter.

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely—highlights now included in the free summary.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

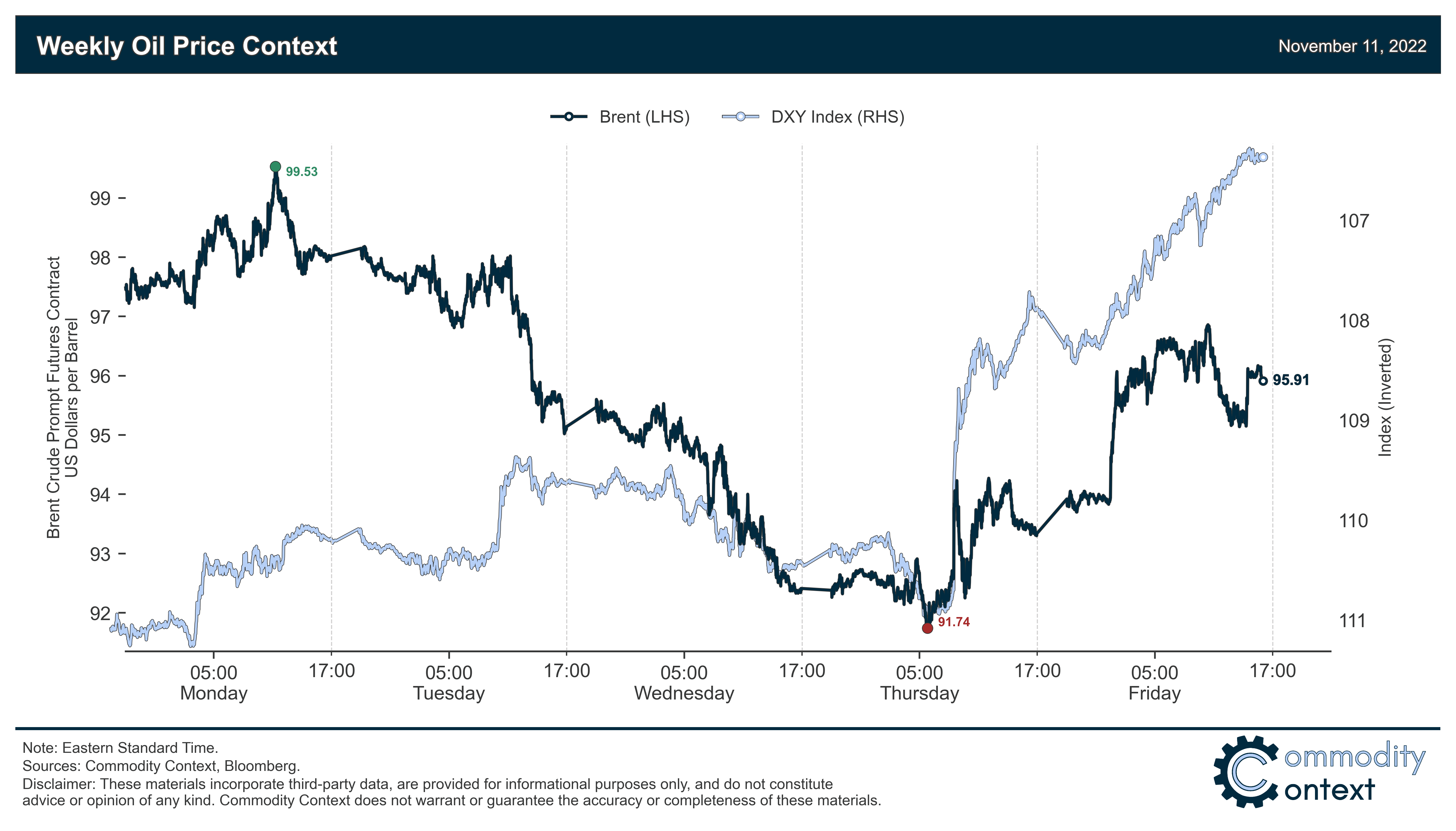

Summary

Flat Prices were flat-to-slightly-down on the week at $96/bbl (Brent) at the time of writing; we nearly breached $100/bbl on Monday but then fell back to sub-$92/bbl before the double-whammy of a super-bullish risk-on response to cooler-than-expected US inflation data released Thursday morning and another round of optimistic news on the China re-opening front on Friday brought us back to the mid-$90s. However, a flat-ish week for crude prices really isn’t great when the US dollar falls by more than 4%—that’s actually a pretty bad week.

Calendar spreads followed prompt prices on their merry-go-round of a week, ending very much where they began for both prompt and Jun23/Dec23 spreads—this is another way of saying that calendar spreads didn’t provide all that much more information than flat prices, beyond the market still being generally tight.

Inventories data was mixed this past week, with headline commercial petroleum stocks falling in the US (-0.8 MMbbl w/w) and ARA Europe (-0.3 MMbbl) and rising in Singapore (+1.9 MMbbl). The US headline decline masked a 3.9 MMbbl w/w crude build, which was overwhelmed by larger refined product draws.

Refined Products crack spreads (i.e., margin) fell back over the past week, with diesel cracks in New York Harbor falling $11/bbl to $61/bbl and gasoline cracks easing slightly to $21/bbl; French refinery strikes ended and a major Kuwaiti refinery entered commercial operation, but further European refinery strikes are possible over the coming month.

Positioning data in Brent futures and options contracts (there was no CFTC WTI contract data released today because of Veterans’ Day) revealed another week of speculative buying as net positions rose by 10.4 MMbbl on the back of a 13.5 MMbbl increase in long positions and a 3.1 MMbbl increase in shorts; the managed money net position as a share of open interest continues to climb.

World’s Largest Refinery Enters Service: Kuwait’s al-Zour refinery—the world’s largest by crude processing capacity—commenced commercial operation with the first phase of the project; the facility is expected to reach full capacity of 615 kbpd by early next year and specializes in processing heavy crude into middle distillates (like diesel!) and low-sulfur fuel oil.

China’s dynamic-zero dynamism: Global markets once again rallied on the latest bout of optimism toward China’s COVID-zero policy stance in the form of a list of concrete easing measures being taken by the government, made more promising still by the fact that it was released amidst China’s worst COVID outbreak since April; on the less-optimistic side, manufacturing powerhouse Guangzhou implemented another lockdown affecting some 5 million citizens.