Oil Context Weekly (W43)

Prices rebounded from last week’s rout but the barrel remains range bound as market awaits Israel’s retaliatory strike against Iran; Brent DFLs and diesel term structure also strengthening.

[Paid Advertisement]

In less than 2 weeks, join over 250 commodities leaders at the Financial Times Commodities Asia Summit in Singapore or online. You may be particularly interested in a keynote address with Bold Baatar, Chief Commercial Officer at Rio Tinto, as well as panel sessions focused on geopolitical impacts and navigating oil price volatility. Interested in who's already registered? Click here to see who's attending.

Both in-person and digital passes are available. As a valued reader, enjoy 10% off your in-person pass with code 2024CASCC10.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

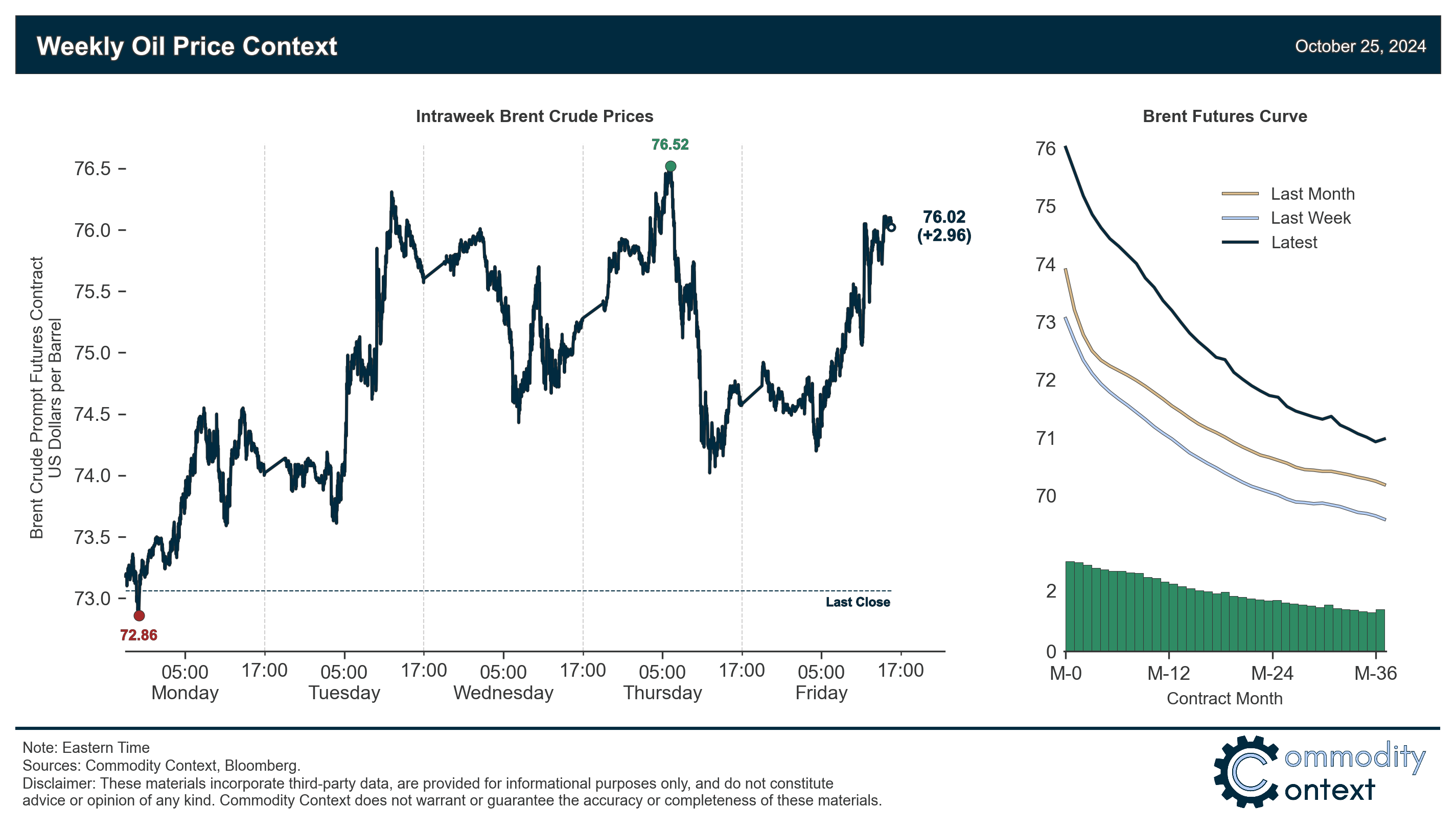

Flat Prices rose ~$3/bbl to end above $76/bbl, reversing roughly half of last week’s violent rout but failing to settle on any real direction as the market anxiously awaits the next chapter in sporadic hostilities between Israel and Iran.

Timespreads provided mixed signals but, overall, supported the move in flat prices: Brent DFLs rose to their highest backwardation in 3 weeks, confirming some underlying physical market strength, while prompt Brent spreads were effectively flat.

Inventories were mixed between builds in the US and Singapore and a draw in ARA Europe; stocks of major US fuels continue to follow their seasonal paths, albeit still at a level below the seasonal norm, while stocks of distillates are falling rapidly across all major hubs.

Refined Products margins for transportation fuels are relatively steady while diesel term structure is finally beginning to show durable signs of improvement; while lower-value feedstocks, like naphtha and fuel oil, are still sporting negative overall crack spreads, these have strengthened considerably through the year and, for fuel oil, especially over the past two months.

Positioning data confirmed that speculators were modest net sellers of crude over the past week-through-Tuesday, bringing us back into oversold net territory compared to the past two years; however, it is increasingly obvious that much of this reduction is being driven by a structural reduction in gross length rather than persistent shorting activity, which will reduce the cyclical upside for prices in the near term.

As Well As US tries to defuse Middle East tensions, US court rules Gulf of Mexico regulations set to expire in December can remain until May, crude options market gets frothier as open interest explodes higher, and domestic Chinese refining margins weaker further and depress operating activity.