Oil Context Weekly (W40)

Crude prices exploded higher as an Iranian missile attack on Israel and potential retaliation against Iranian oil infrastructure sparked mass spec position covering.

This week, I joined the International Energy Forum (IEF) Oil Markets Analysis Webinar [replay available] to break down the differences between the latest fundamental forecasts published by the IEA, EIA, and OPEC—which seems closest to reality and where we see divergence.

Then I had the chance to join BNN Bloomberg on Wednesday [video linked] to discuss the Iranian strikes on Israel and how the price response was overwhelmingly driven by the markets exaggerated short positioning, in stark contrast to the April 2024 attacks.

Happy Friday, Oil Watchers!

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

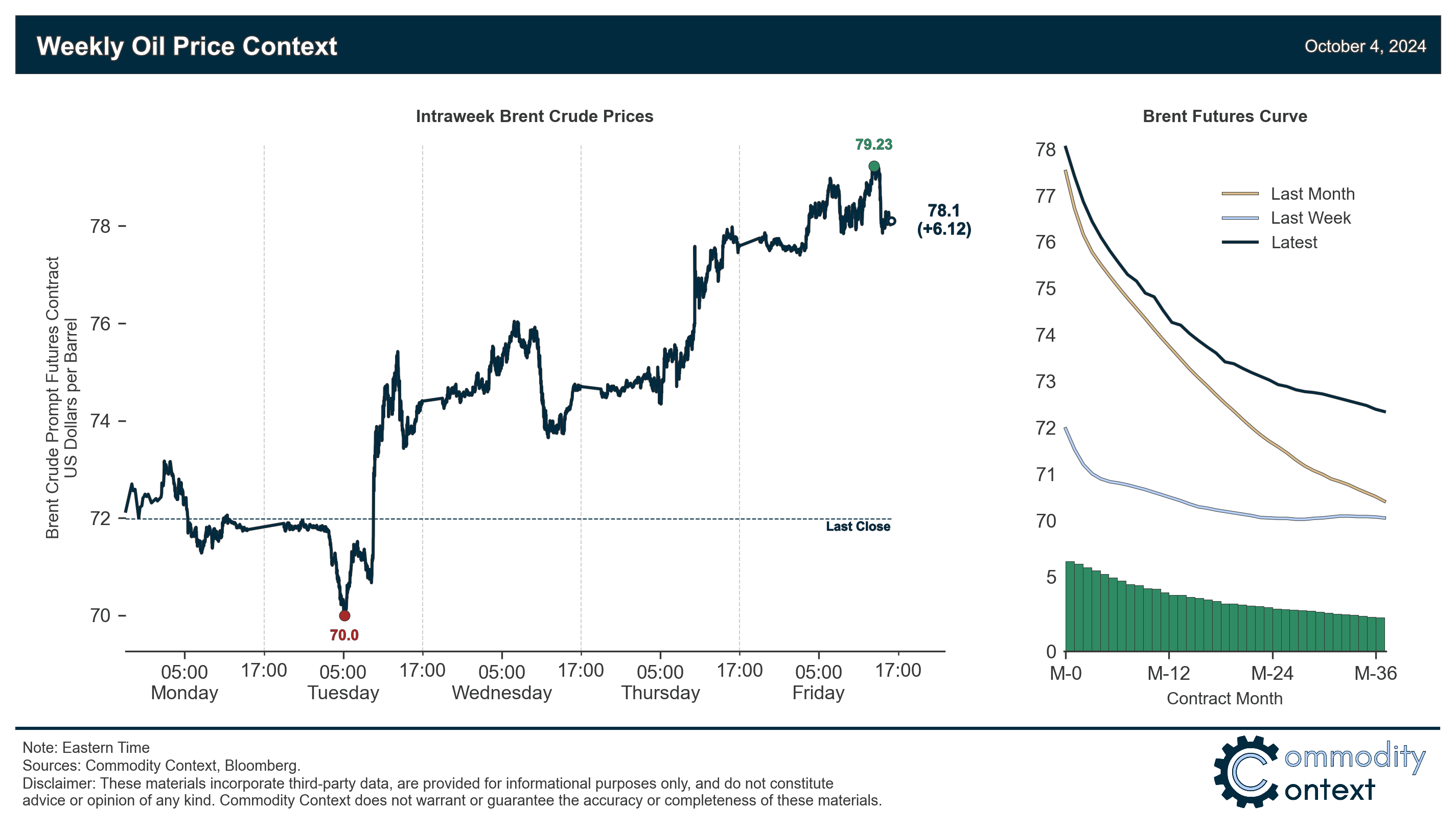

Flat prices roared higher, jumping more than $6/bbl on the week as Iranian missile strikes against Israel and subsequent concerns that retaliatory strikes could target Iranian oil infrastructure lit the powder keg of near-record overstretched short speculative positioning in crude contracts.

Timespreads rallied alongside flat price gains, though prompt spread steepening was relatively muted as gains were spread more broadly across the curve, which itself lifted into pronounced, curve-wide backwardation from last week’s far flattered structure.

Inventories were mixed between builds in Singapore and smaller draws in the US and ARA Europe.

Refined Products were uneventful compared to crude’s precipitous rally, though flat—and, even, modestly positive—crack spread performance amidst a steep speculative run-up in crude prices is a promising sign for current underlying market strength.

Positioning data confirmed that speculators were very small net sellers of crude contracts over the past week-through-Tuesday; even factoring for the bounce we likely saw in the latter half of the week, positioning remains low by virtually any historical standard and represents an ongoing tailwind for crude prices over the coming month, blunting downside corrections and amplifying upside surprises as we saw this week.

As Well As Iranian missile strikes on Israel and mounting concerns about potentially-US-supported retaliatory strikes against Iranian oil infrastructure, how OPEC+ is positioned to respond to possible Iranian supply losses, another round of Saudi/OPEC+ rumours (this time vehemently and officially denied), and the return of disrupted Libyan oil production following the end of the export blockade.