Oil Context Weekly (W28)

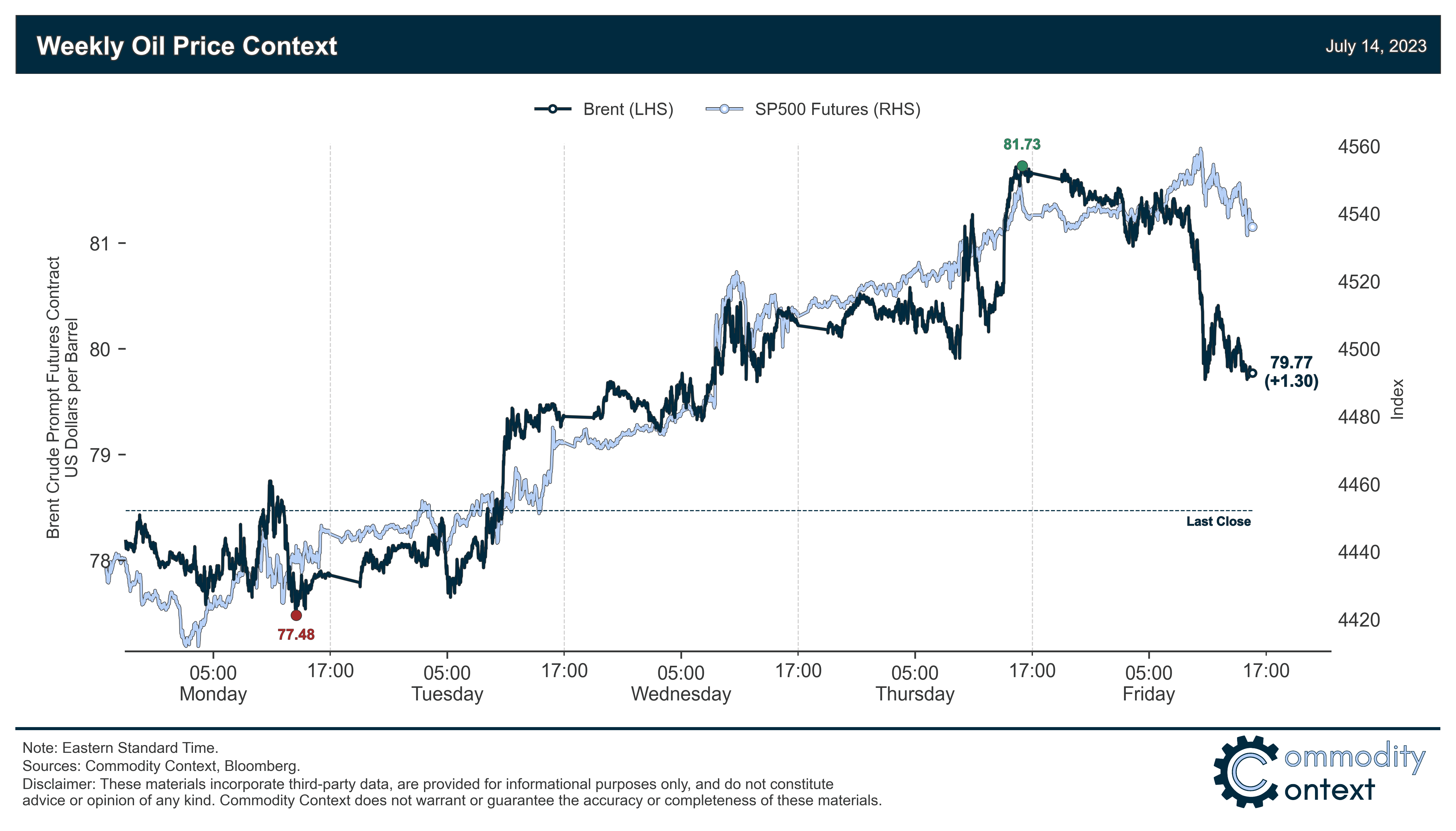

Crude prices rise again on ~600 kbpd in unexpected supply losses between Libya and Nigeria, but Brent failed to finish the week above $80/bbl.

Happy Friday!

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices rose ~$1.30/bbl to just shy of $80/bbl Brent, buoyed by rising broader markets and a suite of supply disruptions in Libya/Nigeria worth upwards of 600 kbpd, seemingly unphased by large US inventory builds.

Calendar Spreads were little moved, with prompt spreads tightening by ~$0.10/bbl and Dec23/Dec24 spreads widening by about the same measure.

Inventories data was mixed but overall bearish thanks to the largest US commercial petroleum build since early February; meanwhile, inventories outside the US continued to fall, reaching exceptionally low levels in Singapore, specifically.

Refined Products also had a reasonably quiet week, with gasoline cracks gaining ~$1/bbl while distillate cracks were effectively flat.

Positioning data revealed that speculators were net buyers of crude futures and options contracts to the tune of 81 MMbbl last week-through-Tuesday, driven by a 46.8 MMbbl increase in long positions and a 34.2 MMbbl reduction in shorts; these net purchases no doubt helps boost crude gains, but we’ve also moved from super bearish positioning to pretty middle-ground levels, shifting the positioning risk from unambiguously to only modestly bullish.