Oil [& OPEC] Context Weekly (W22)

Oil markets deteriorated ahead of OPEC+’s weekend meetings, which themselves grew chaotic amidst a flurry of last-minute headlines that some members would be traveling for in-person meetings in Riyadh

I joined BNN Bloomberg this afternoon to discuss the state of play heading into OPEC+ negotiations this weekend—check out that full video interview here.

The bulk of today’s write-up outlines how rumours around Sunday’s OPEC+ meetings have been developing. Pre-meeting chatter picked up on Thursday and then the barn doors blew open earlier today as a flurry of confusing reports regarding where, exactly, the negotiations would be taking place hit the wire and entirely muddied the waters heading into the meetings.

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

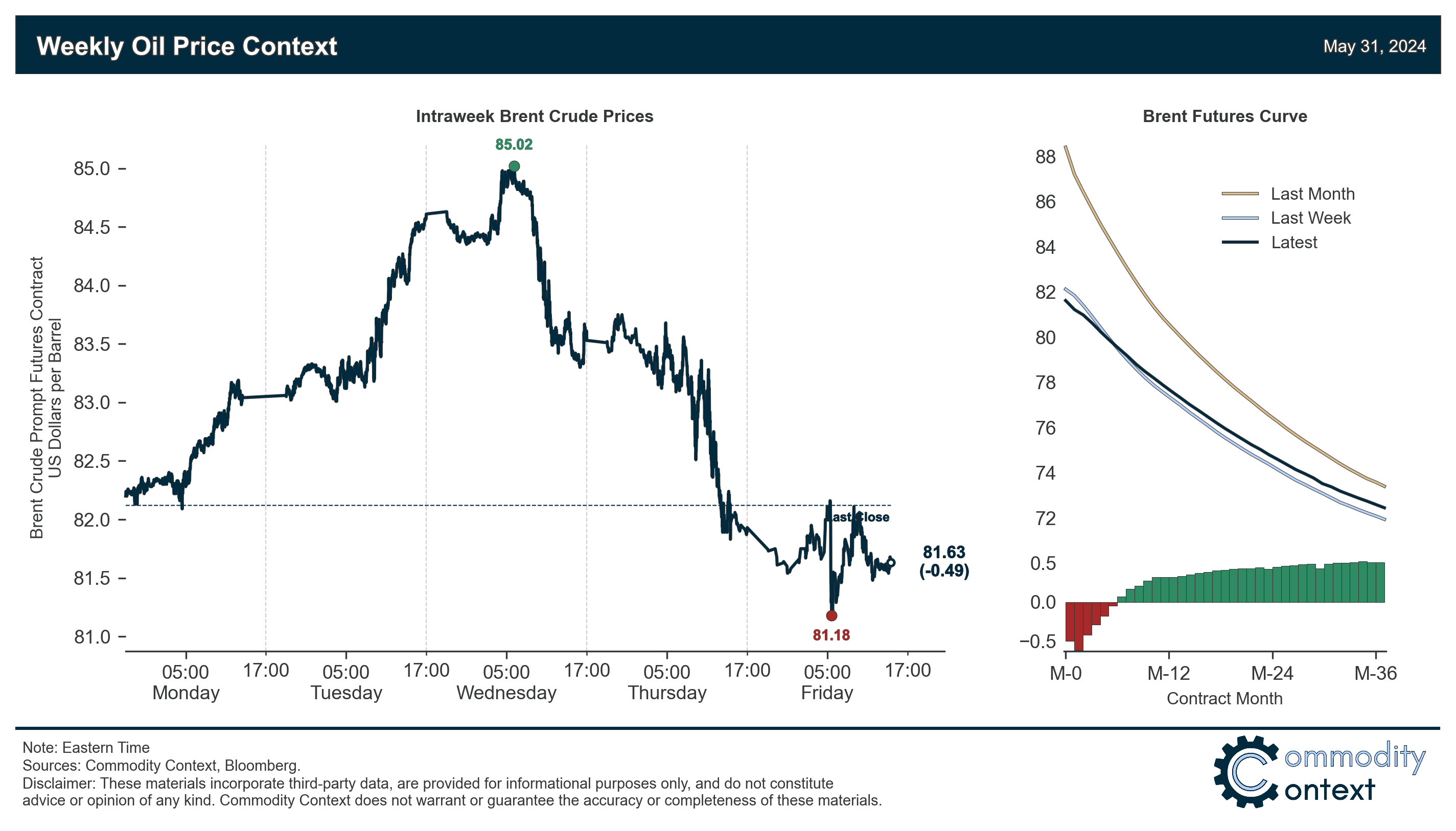

Flat Prices fell slightly to end the week just shy of $82/bbl (Brent), down from $85/bbl earlier in the week, though flat prices were generally more resilient than deterioration witnessed across term structures and related to refined products.

Futures Curves provided objective confirmation of OPEC+ delegate’s inventory-related concerns, with weakening prompt futures spreads and deepening outright contango in physical Brent markets; on the brighter side, longer-dated Brent contracts actually gained on the week.

Inventories data was mixed but leaned bearish on the back of a large product-driven inventory build in the US (12.7 MMbbl), a smaller build in Singapore (+1.2 MMbbl), and a small draw in ARA Europe (-0.5 MMbbl); US crude stocks drew ahead of seasonal schedule, but sizable builds of both gasoline and diesel added further cause for concern for weakening refined product markets.

Refined Products were a further source of concern as both calendar spreads and refining margins sank further.

Positioning data revealed that speculators were net buyers of crude contracts over the past week-through-Tuesday, a modest reversal of recent selling pressure; however, gross short positions remain high, which tend to irk OPEC leadership and were, last year, the explicit target of production cut surprises.

OPEC+ delegates are set to meet on Sunday, with pre-meeting rumours now tilting toward bigger decisions than the previously expected deal rollover; speculation is shifting into overdrive given last-minute confusion about where deliberations will even take place (OPEC has stressed that official meetings are still occurring online but some subset of member delegations will now be traveling to Saudi Arabia for Sunday).