Oil Context Weekly (W21)

Crude prices end the week lower as physical market signals darken and spec selling continues; on the brighter side, product markets appear to have found a near-term floor.

Every week, I summarize and analyze developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

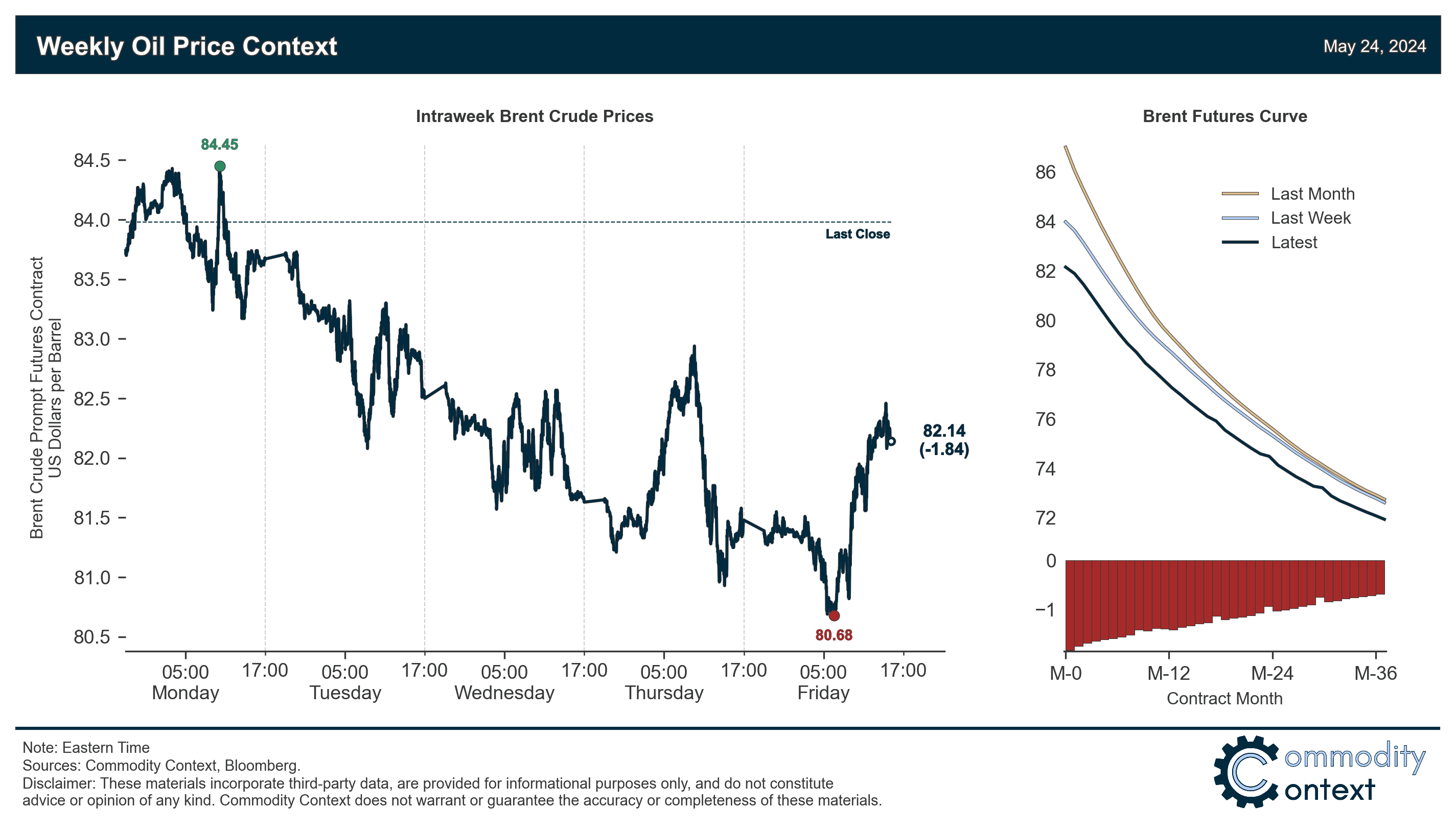

Flat Prices sank further to mark their lowest weekly close since early March amidst a slow news week as markets await next weekend’s OPEC+ decision; US-based WTI fared better than Brent, the spread between which is now sitting around its most narrow of the year.

Futures Curves weakened further for Brent crude, which saw prompt calendar spreads slacken while CFDs slipped into even deeper contango; WTI outperformed its globally dominant peer, seeing prompt spreads actually rise slightly over the course of the week.

Inventories data was mixed between draws in Singapore and then builds across the US and Europe; US stocks continue to follow a pretty typical seasonal pattern while European builds are running a bit hot and Singaporean inventories, driven by fuel oil, are drawing aggressively.

Refined Products have seemingly found a near-term floor as crack spreads and calendar spreads for both gasoline and diesel trade sideways after a month of mounting downside pressure.

Positioning data revealed that speculators were once again net-sellers of crude contracts and that their aggregate position had reached its most bearish since last December; however, while we still have yet more downside to reach the depths of early-December (3.5% of open interest vs 6.1% today), the balance of hot money flow risks are now tilted to the upside—or at the very least we’re closer to the end than the beginning of this latest spec selling cycle.

As Well As OPEC+ shifts its next weekend negotiations online, Saudi Arabia looks to sell more of Aramco, Brent weakening relative to WTI, and why the sale of the US Northeast Gasoline Supply Reserve isn’t another “SPR release”.