Oil Context Weekly (W1)

Oil market trips out the gate in first week of 2023 as Brent sinks below $80/bbl to its lowest weekly close in a month and prompt calendar spreads flip back into contango.

Happy New Year! Welcome to Oil Context Weekly, my less formal wrap-up of the market analysis, news flow, and data releases that matter.

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

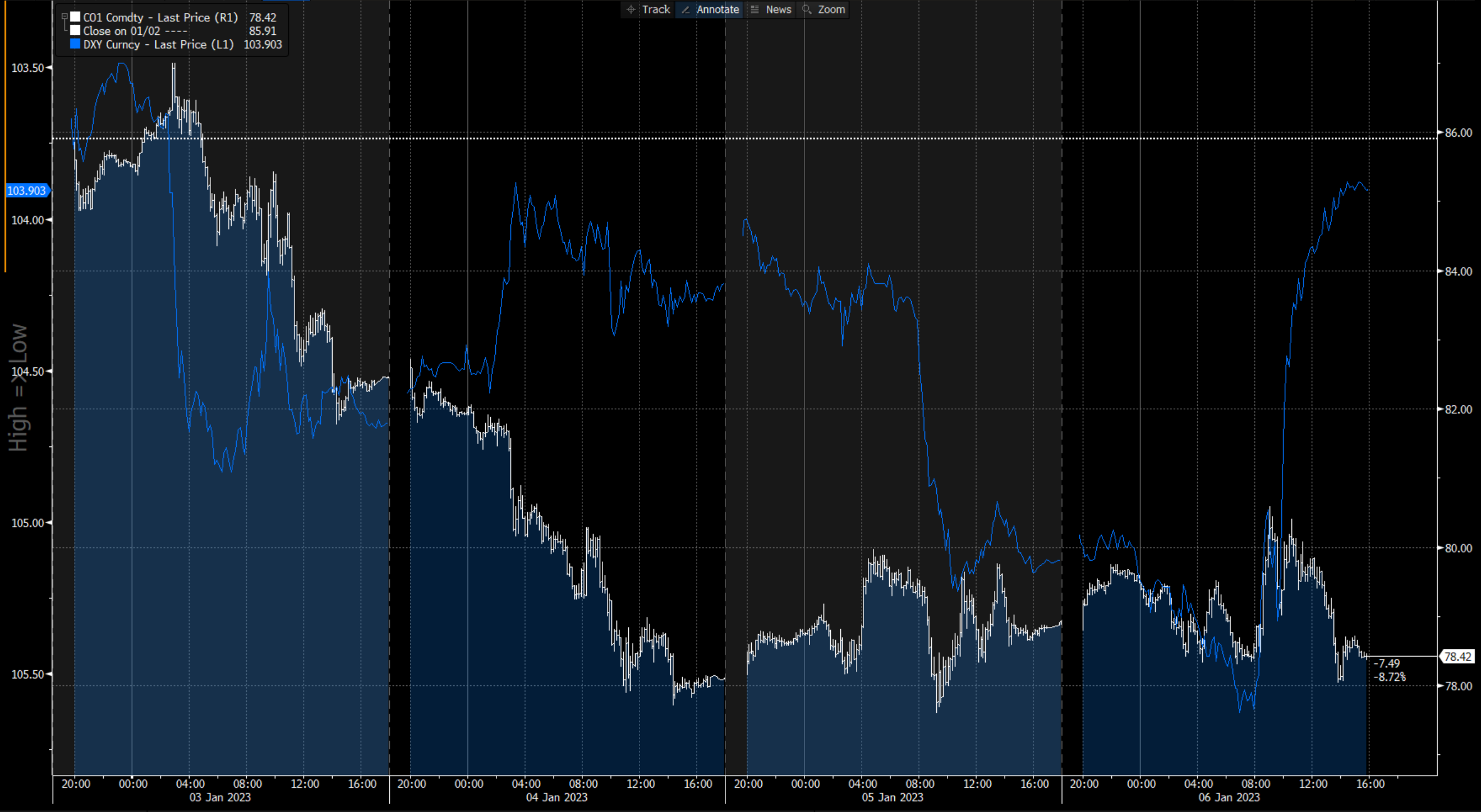

(Prompt Brent crude price = white; DXY US dollar index, inverted = blue; Source: Bloomberg Terminal)

Summary

Flat Prices gave up all their year-end gains and then some through the first week of 2023, falling ~$8/bbl in the first two trading days of the year to below $78/bbl (Brent) before stabilizing in the ~$78-$80/bbl range for the remainder of the week.

Calendar Spreads also weakened, with Brent flipping back into prompt contango after only just regaining its backwardation status in the final few days of 2023; the bellwether Jun/Dec spread also eased off materially, from a backwardation of >$3/bbl on Tuesday morning to <$2/bbl at the time of writing.

Inventories data covering the final week of 2022 were decidedly mixed, showing a modest commercial petroleum draw of 3.1 MMbpd in the US vs. builds across Singapore (+2.2 MMbbl) and ARA Europe (+0.8 MMbbl).

Refined Products margins eased off in New York Harbor over the past week as US refineries presumably continued to recover from December’s winter storm chaos; an [expected] short outage on the major Colonial failed to durably reverse that weakening trend.

Positioning data indicated that speculators were net sellers of crude futures and options contracts through the week ending Tuesday; the net speculative position fell by 12.2 MMbbl, the largest reduction in just more than a month; however, the as a share of total open interest in the relevant contracts, the net speculative position now represents 7.76%—a 0.29% w/w reduction but, excluding the prior week, still at the highest level since early November.

China announced further supports for the economy, adding to the momentum theoretically building as Beijing continues to shift away from its COVID-zero stance; latest announcements related to easing credit conditions for the all-important real estate sector, both backtracking on the government’s debt rationalization priorities for the sector as well as once again falling back on its old-faithful strategy of stimulating heavy legacy industries when running into economic growth challenges.