Oil Context Weekly (W19)

Crude prices fall $1/bbl alongside easing equities and a rallying US dollar; the macro vortex of doom remains well-entrenched, now fueled by the cacophony of US debt ceiling debates

Happy Friday,

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

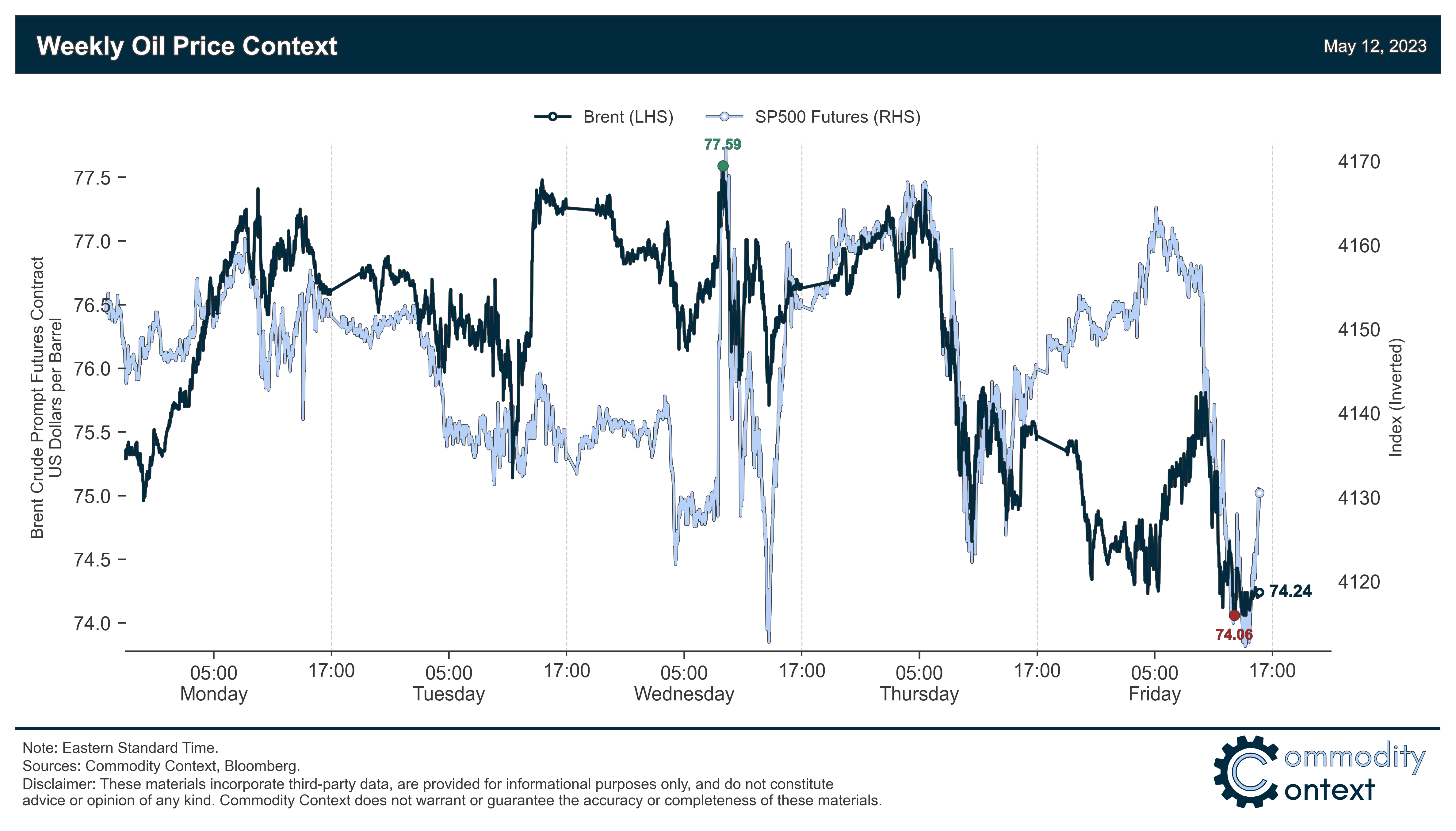

Summary

Flat Prices fell $1/bbl to $74/bbl (Brent basis) after a final Friday rout that saw crude chase equities lower alongside a strengthening US dollar; oil remains firmly trapped in the macro vortex of doom, trading more on debt ceiling headlines than any specific bullish or bearish oil-specific news.

Calendar Spreads were mixed between slightly wider prompt spreads—theoretically the most spot-market aware—in contrast to easing Dec23/Dec24 spreads, which narrowed in line with falling flat prices.

Inventories data were mixed but leaned generally bearish on a headline basis, while in the US crude builds were offset by a resumption of large draws in key refined product stocks.

Refined Products strengthened vs crude this week, with gasoline gains outpacing beleaguered diesel; rising crack spreads reflect both a sharp reduction in the US stocks of both fuels as well as the announcement of reduced Chinese export quotas.

Positioning data revealed that speculators were once again net sellers of crude futures and options contracts in the week-through-Tuesday on the back of further shorting; the net spec position as a share of total open interest is now decently below the trailing norm, tilting positioning risks—all else equal—to the upside, a tilt that likely grows more bullish when factoring for the selling in the second half of the week.