Oil Context Weekly (W18)

Calamitous week for oil drags WTI prices down more than $10/bbl at their worst in yet another macro and banking panic driven speculative washout, though contracts regained lost ground on Friday

Happy Friday,

I had the opportunity to speak with the Financial Times this week about the bifurcated and polarized market between resilient gasoline-linked consumers and battered diesel-consuming businesses.

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

This one is admittedly a bit long because—and I can’t stress this enough—a LOT happened this week.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

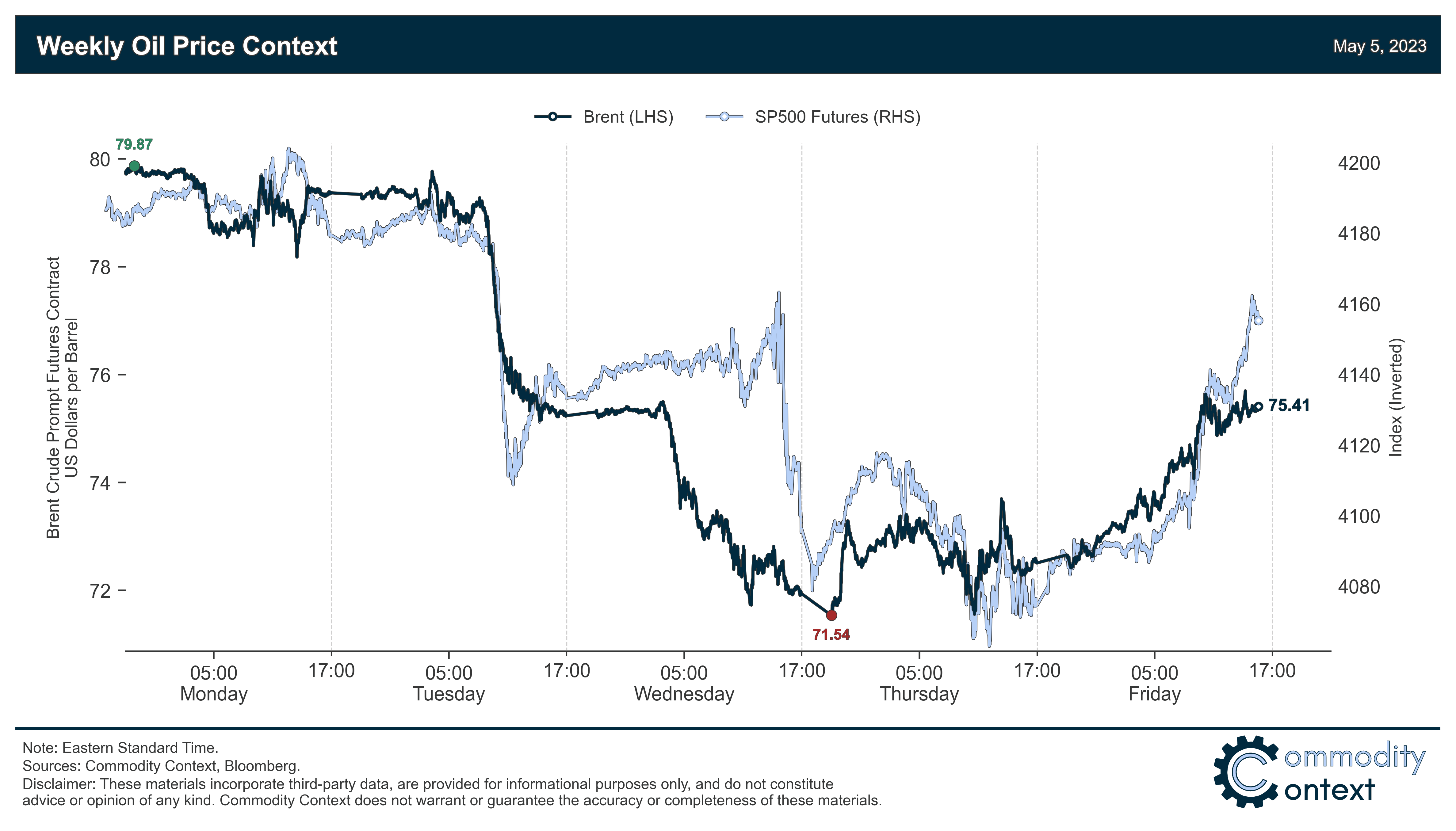

Flat Prices fell another $4/bbl, albeit a considerable improvement over the astounding more than $10/bbl shed by crude at the sharp bottom of the market this week; selling pressure was driven by speculative and flows-related pressures far more than any fundamental factors, with Brent closely tracking battered equity prices from their initial collapse to late-week recovery.

Calendar Spreads fell in tandem with the flat price rout but declines were comparatively muted and the Brent curve never even threatened a mild break into contango; even WTI, which has spent much of 2023 in prompt contango, only made it as far as flat vs. the 2nd month at the bottom of Wednesday evening’s (Thursday morning in Asia) collapse.

Inventories data were mixed across the unexpected flat-ish US stocks (+0.4 MMbbl) and then sizeable but almost entirely offsetting builds/draws for ARA Europe (+2.2 MMbbl) and Singapore (-2.27 MMbbl), respectively

Refined Products saw the relative fortunes of gasoline and diesel reverse their months-long trends, with the former easing off and the latter gaining in what could be an early crack in the strong consumer/weak business demand narrative

Positioning data revealed that speculators were—obviously—net sellers of crude futures and options contracts to the tune of 105.3 MMbbl over the past week-through-Tuesday; as a share of total open interest, the net spec position now sits at 5.7% vs. a March mini-banking crisis low 4.6%.