Oil Context Weekly (W17)

Crude prices ease ~$2/bbl on a combination of renewed macro concerns, technical factors, and speculative selling—or maybe it’s just the same 5-month-old cycle restarting anew.

Happy Friday,

Excited to be writing this week’s Oil Context Weekly from New York City ahead of the FinTwitIRL conference this weekend.

Every week, I summarize the developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data and then provide a taste of the themes I’m thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

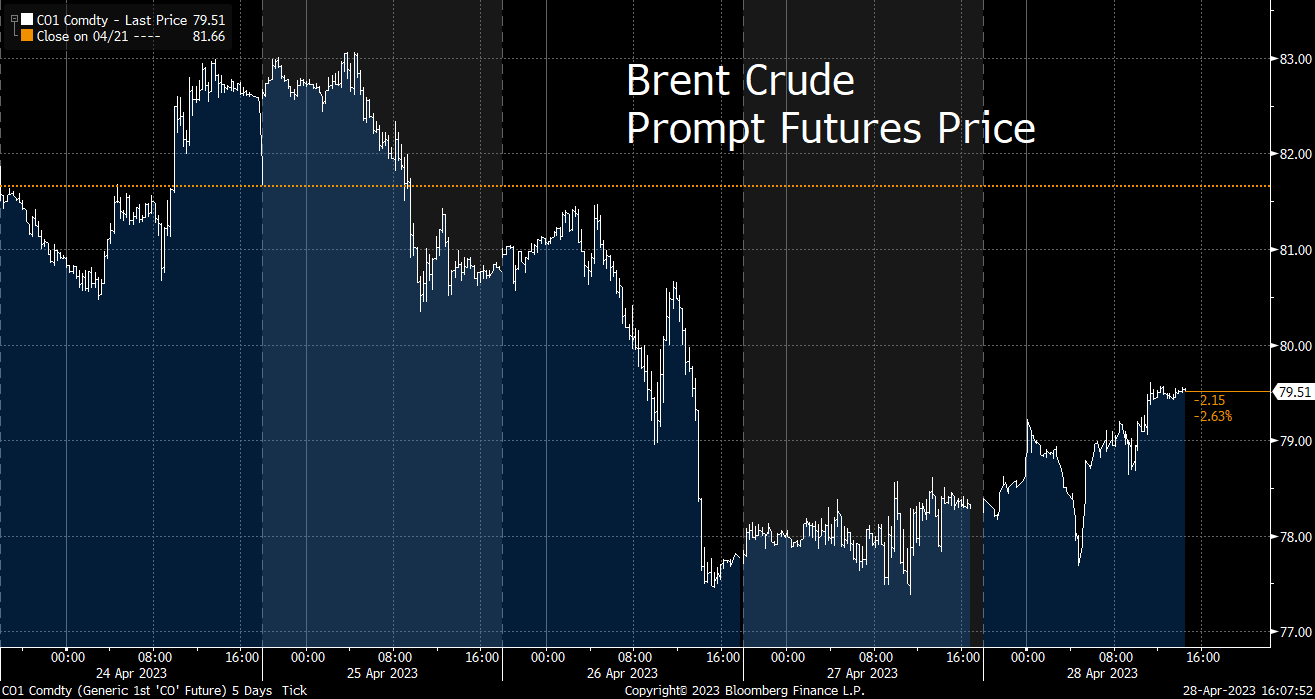

Flat Prices fell more than $2/bbl and Brent slipped back below $80 per barrel for the first time since OPEC+’s surprise production cut last month; however, that weakness appeared to be driven mostly by more broadly falling equity markets and renewed macro fears.

Calendar Spreads were comparatively uneventful and, if anything, stand as a positive sign juxtaposed against flat price weakness; that said, the prompt Brent spread did flip into mild contango earlier this week but it has a tendency to get wonky this close to expiry and the 2nd-3rd month spread remained far more resilient.

Inventories data were modestly bullish on a headline basis and looked more bullish below the surface—US crude stocks posted their second-largest draw of the year and gasoline stocks continued their downtrend after last week’s pause, only offset by substantial non-core other product builds.

Refined Products performance was mixed: diesel crack spreads continued their months-long decline to briefly fall below $20/bbl for the first time since late-2021, while gasoline cracks posted modest gains that further confirmed the increasingly dominant narrative that resilient consumer demand is offsetting increasingly muted industrial activity.

Positioning data revealed that money managers were net sellers of crude contracts to the tune of 54.3 MMbbl over the past week-through-Tuesday, driven by a 32.5 MMbbl reduction in longs and 21.8 MMbbl in fresh shorting; the (likely) further selling that we saw after Tuesday brings us to more-or-less neutral positioning levels, without any material pressure in either direction.

Russian Stats Blackout initiated this week completely killed upstream oil production data that was still being published by Russia’s main statistical agency, Rosstat; this move comes as uncertainty rises about the precise state of Russian oil flows, eliminating the opportunity to validate the Kremlin’s claims to exceptionally steep output declines in March. In a perverse way, this move actually endorses the accuracy of previously published official data—if the data was being fudged, why cut it now?